Showing 120 of 120on this page. Filters & sort apply to loaded results; URL updates for sharing.120 of 120 on this page

GARCH vs. GJR-GARCH Models in Python for Volatility Forecasting

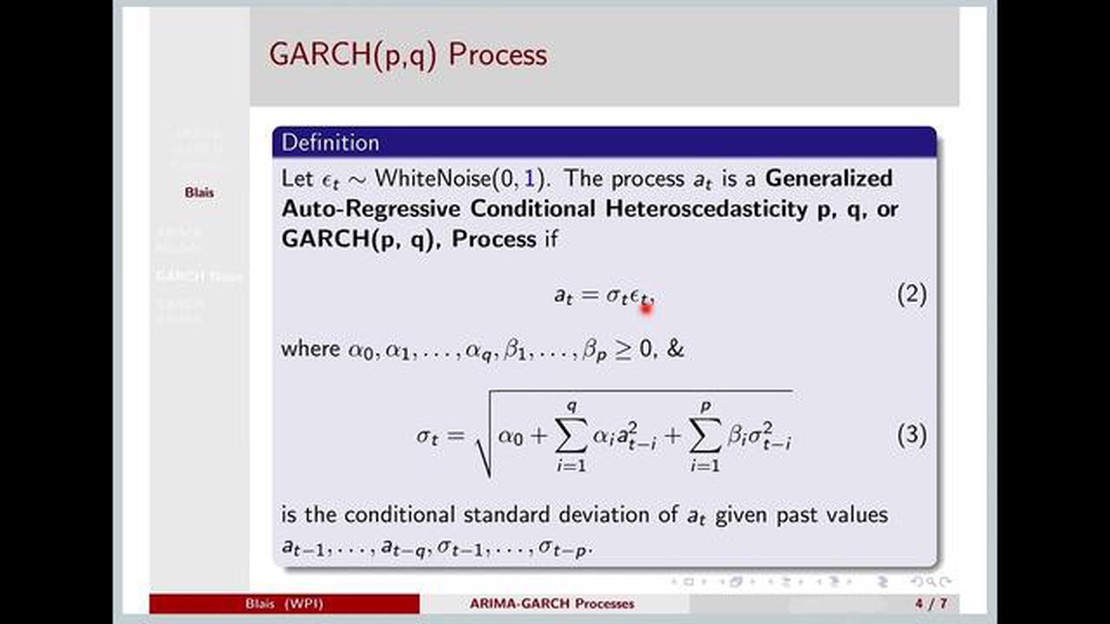

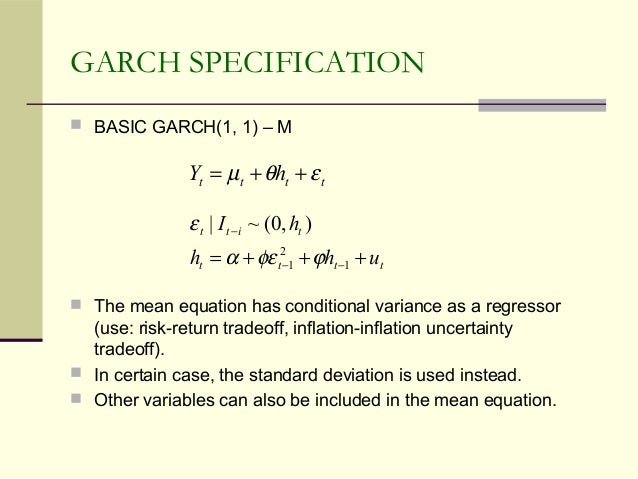

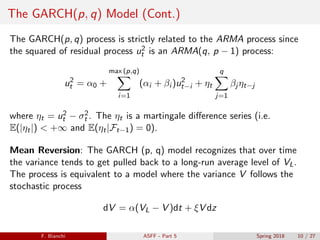

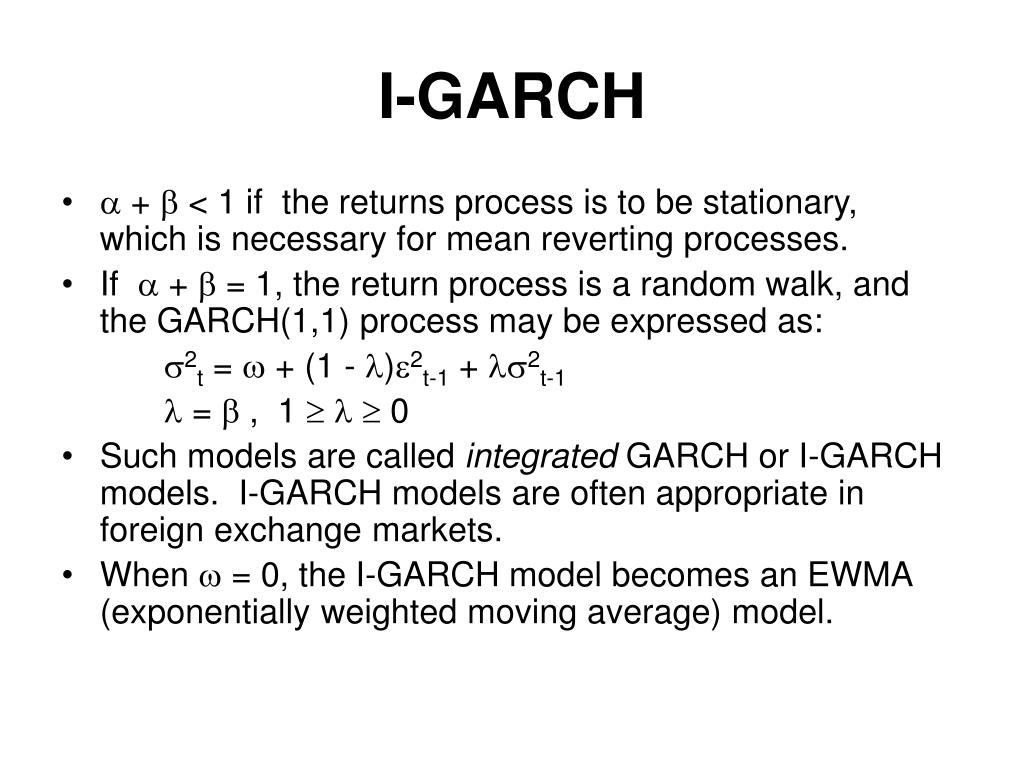

What Is the GARCH Process? How It's Used in Different Forms

GitHub - Allisterh/Different_GARCH_models: Weekly homework about GARCH ...

Understanding GARCH Models: Volatility Prediction in Finance

Christina Kay & Katie Garch - WAPT : r/newswomen_hd

(PDF) ANN-Time Varying GARCH Model for Processes with Fixed and Random ...

GARCH models with R programming : a practical example with TESLA stock

Arch & Garch Processes | PDF

PPT - GARCH Models and Asymmetric GARCH models PowerPoint Presentation ...

V-Lab: Prevas AB Zero Slope Spline-GARCH Volatility Analysis

Conditional standard deviation for AB and GB cases computed using the ...

(PDF) Comparison of GARCH and SVRGARCH models: Example of gold return

Amazon.com: GARCH Models: Structure, Statistical Inference and ...

Garch Vs Edward Elric (Dbmlore Vs Fullmetal Alchemis) "Spirit Alchemist ...

Figure 2 from A Comparison of GARCH Option Pricing Models Using ...

Advanced Garch Variants Overview PPT Example ST AI SS PPT Template

(PDF) Testing for GARCH effects: a one-sided approach - DOKUMEN.TIPS

Understanding Asymmetric GARCH Models in Financial Econometrics ...

Understanding ARCH and GARCH Models for Financial Volatility | Course Hero

GARCH Analysis on Volatility Patterns | EODHD APIs Academy

Figure 1 from An interval-valued GARCH model for range-measured return ...

Full article: Bayesian Nonparametric Panel Markov-Switching GARCH Models

PPT - Module 3 GARCH Models PowerPoint Presentation, free download - ID ...

The Garch household has a visitor! : r/Dbmlore

(PDF) Hisse Senedi Piyasalarındaki Oynaklığın GARCH Modelleri ile ...

Makalah Model Arch Dan Garch Kelompok 10 | PDF

Figure 1 from A comparative analysis of multivariate GARCH and CNN ...

Introduction to ARCH & GARCH models / introduction-to-arch-amp-garch ...

为什么 GARCH 优于 ARIMA:对比分析

Financial econometrics xiii garch

Snails vs Garch “Motherly Might” TM by 2r0n and NOT 1r0n : r/Dbmlore

(PDF) GARCH Models - unipveconomia.unipv.it/pagp/pagine_personali ...

Sarveshwar Inani's Blog: GARCH Modelling

Model ARCH dan GARCH dalam Volatilitas | PDF

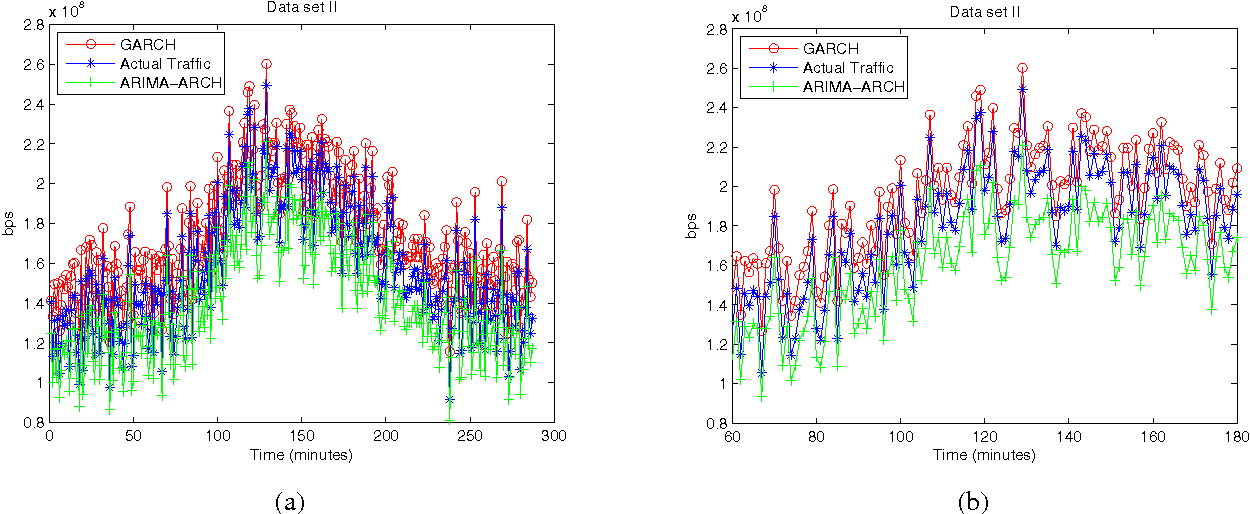

Figure 4 from GARCH — non-linear time series model for traffic modeling ...

(PDF) Garch (1,1) comparision - DOKUMEN.TIPS

Figure 3 from GARCH — non-linear time series model for traffic modeling ...

(PDF) Financial Econometrics Lecture 3: ARCH & GARCH models

GARCH Model - Nixtla

GARCH Models for Volatility Forecasting: A Python-Based Guide | by The ...

ARCH vs GARCH (The Background) #garch #arch #clustering #volatility # ...

Garch - 3D model by Mr.MaroonMoon (@MaroonTune) [240f6ee] - Sketchfab

What Is GARCH Model In Python? - AskPython

Comparison of suggested GARCH models. | Download Scientific Diagram

Table 1 from Bayesian Estimation of GARCH Model by Hybrid Monte Carlo ...

The pricing of options on WIG20 using GARCH models Kaminski, Szymon ...

Lecture 8 Stephen G Hall ARCH and GARCH

GARCH Update for next week (N)OPEX : r/PickleFinancial

Table 1 from Gumbel GARCH model with stock application | Semantic Scholar

Differences between ARCH and GARCH models. | Download Scientific Diagram

Volatility capturing using simple GARCH and DCC-GARCH model. Note ...

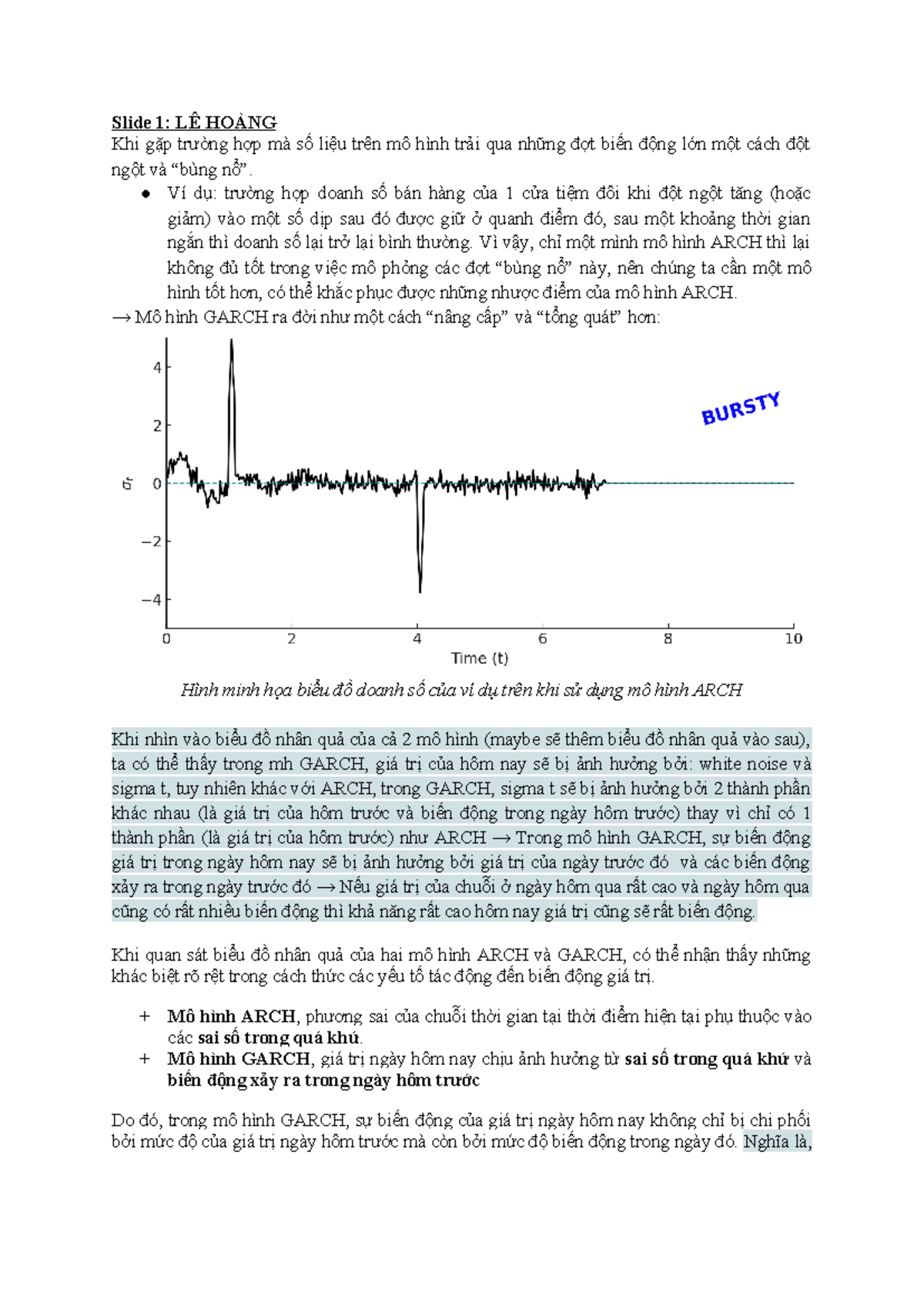

Script Garch - Slide 1: LÊ HOÀNG Khi gặp trường hợp mà số liệu trên mô ...

GARCH Update : r/PickleFinancial

Modèles ARCH-GARCH et Asymétrie des Chocs | PDF | Loi normale | Asymétrie

Garch模型Stata实例-CSDN博客

GitHub - J-02/Arch-and-Garch-models: Application of ARCH, GARCH, and ...

4 -A GARCH(1, 1) process with 2 breaks (K * = 3) following the scenario ...

GitHub - atmajitg/garch_arch_model: The project is trying to develop an ...

金融时间序列分析:Python基于garch模型预测上证指数波动率、计算var和var穿透率、双尾检验_garch var-CSDN博客

GitHub - JustinRuelland/Garch_Model_Assets: Projet de modélisation des ...

Table 3.1 from Comparison of option pricing between ARMA-GARCH and ...

Network Graph · yolowinnn/Code-for-fitting-the-GARCH-family-model-to ...

R语言学习:如何构建DCC-GARCH模型? - 知乎

Forecasting Stock Price Volatility New Evidence From The GARCH-MIDAS ...

PPT - ARCH/GARCH Models PowerPoint Presentation, free download - ID:8824700

Time Series Analysis - 6 Generalized Autoregressive Conditional ...

Figure 2 from Forecasting Stock Market Volatility with Regime-Switching ...

(PDF) Properties and estimation of GARCH(1,1) model

Hedge ratio for the AB-GB and the AB-GBS cases computed using the ...

Modelling time-varying volatility using GARCH... | F1000Research

ARIMA和ARIMA-GARCH模型预测股票价格-R语言 - 知乎

第三章 ARCH和GARCH模型(2014FALL)_word文档在线阅读与下载_无忧文档

R语言多元(多变量)GARCH :GO-GARCH、BEKK、DCC-GARCH和CCC-GARCH模型和可视化|附代码数据-腾讯云开发者社区-腾讯云

Figure 1 from GARCH-Informed Neural Networks for Volatility Prediction ...

SVR_GARCH_KDE/Benchmark_Methods/GARCH/Apply_GARCH_Models_V2.R at master ...

多变量GARCH模型R代码实现_garch能研究两个变量嘛-CSDN博客

Volatility forecasting (GARCH & ARCH) - Nixtla

Python使用GARCH,EGARCH,GJR-GARCH模型和蒙特卡洛模拟进行股价预测-腾讯云开发者社区-腾讯云

求助 ARIMA和GARCH模型一起怎么用? - 知乎

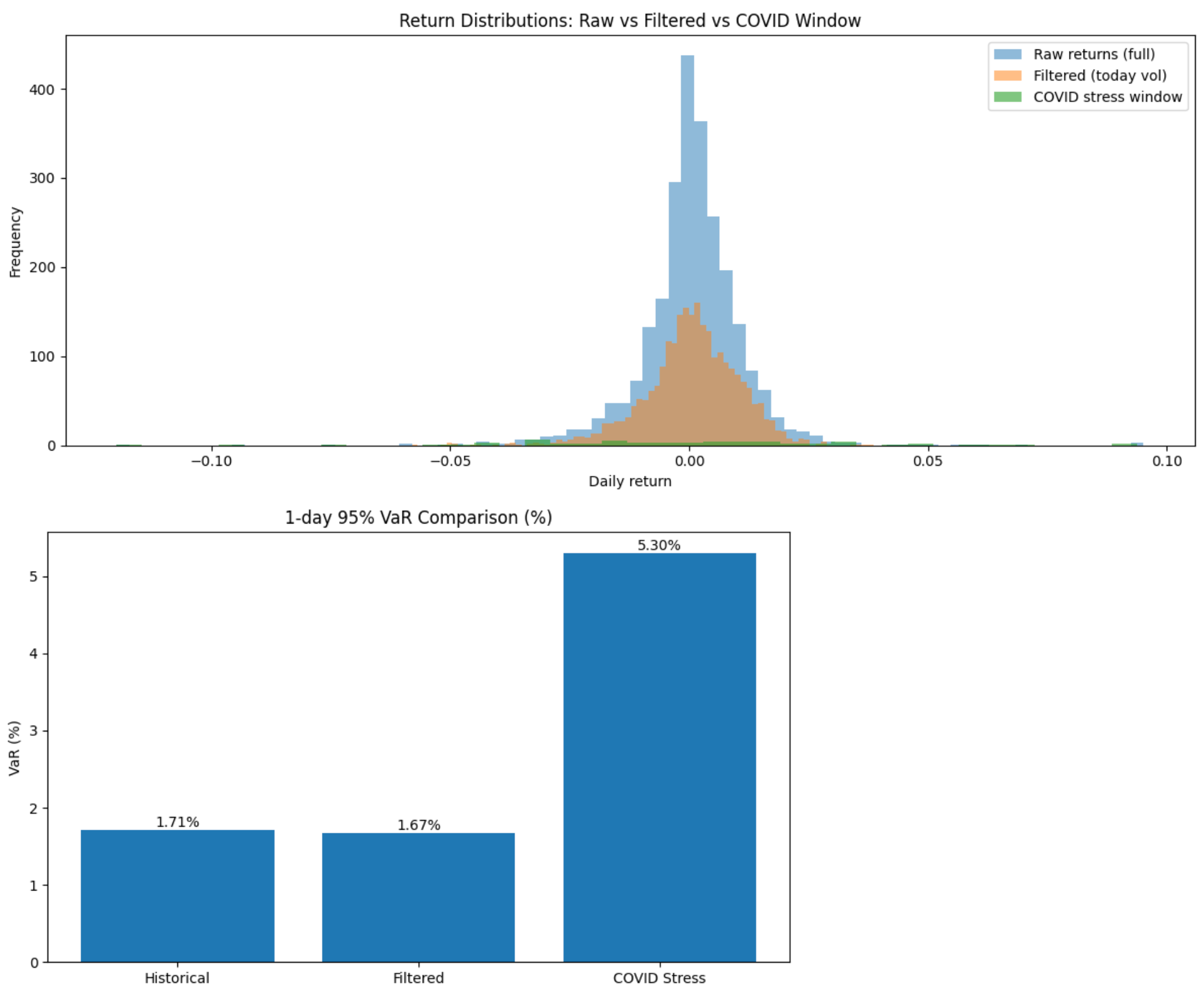

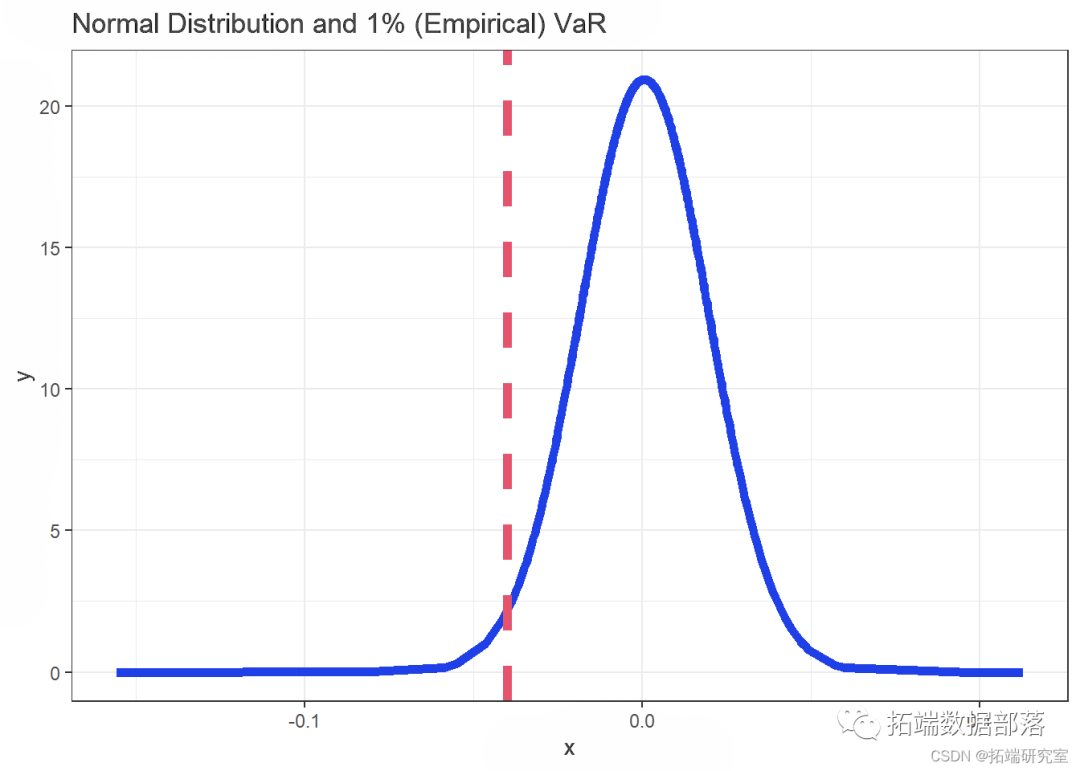

Value-at-Risk Models (Using The S&P 500): Non-Parametric, GARCH, and ...

Full article: Neural networks and ARMA-GARCH models for foreign ...

GitHub - disserth/VaR_DCC_GARCH

(PDF) Estimating m-regimes STAR-GARCH model using QMLE with parameter ...

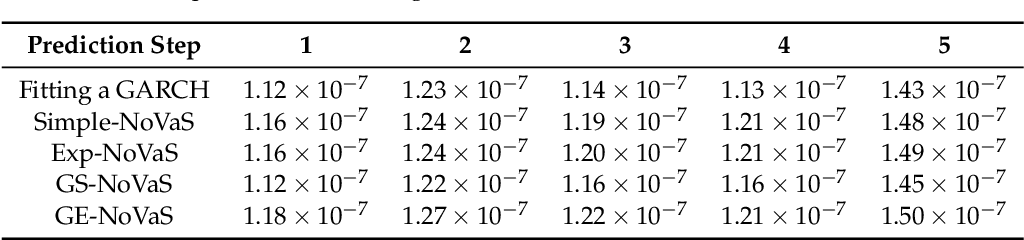

Table 1 from Optimal Multi-Step-Ahead Prediction of ARCH/GARCH Models ...

(PDF) The Pricing of CSI 300 ETF Options with GJR-GARCH Model

R语言用GARCH模型波动率建模和预测、回测风险价值 (VaR)分析股市收益率时间序列|附代码数据 - 知乎

GARCH指导的神经网络在金融市场波动性预测中的应用 - 知乎

nifty-option-volatility-model/VolatilityEWMA_ARCH_GARCH.ipynb at main ...

Modelling Volatility Cycles: The MF2‐GARCH Model - Conrad - Journal of ...

The likelihood values of (a) GARCH, EGARCH, and GJR-GARCH models; (b ...

Schematic diagram of hybrid NN-GARCH model | Download Scientific Diagram

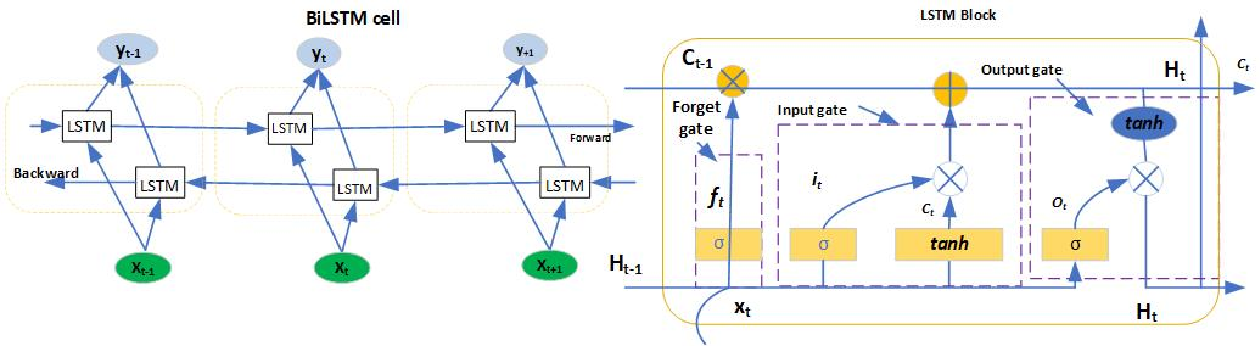

ANN-GARCH and LSTM-GARCH architectures. | Download Scientific Diagram

R语言DCC-GARCH模型对上证指数、印花税收入时间序列数据联动性预测可视化-CSDN博客

EGARCH与GARCH的区别? - 知乎

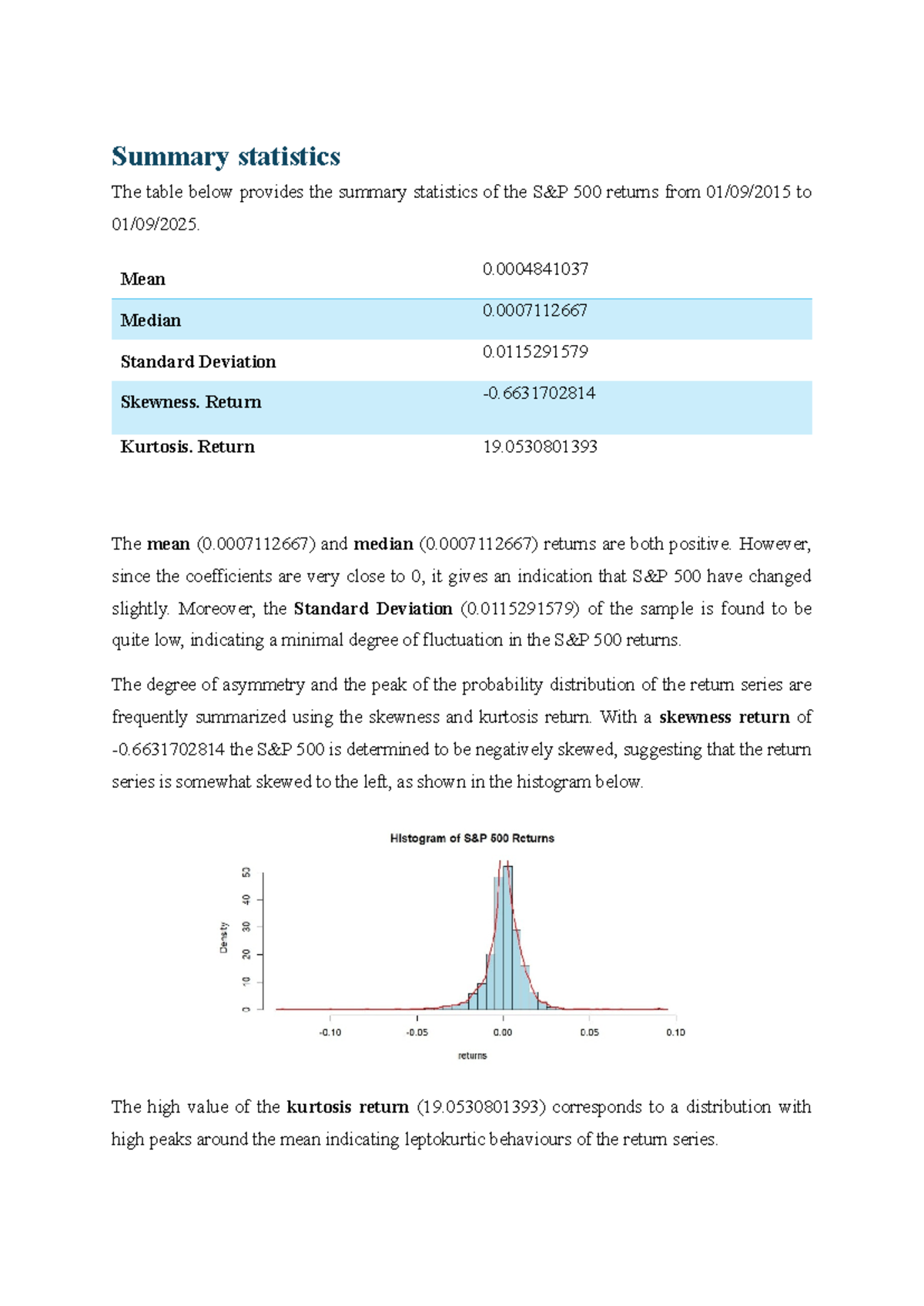

Summary Statistics of 500 Returns: GARCH(1,1) Analysis - Studocu

(PDF) Revisiting the cryptocurrencies role in stock markets: ADCC-GARCH ...

PPT - Correlation Measures PowerPoint Presentation, free download - ID ...

基于Copula—GARCH模型的上证地产股与金融股的相关性研究_word文档在线阅读与下载_无忧文档

R语言多元(多变量)GARCH :GO-GARCH、BEKK、DCC-GARCH和CCC-GARCH模型和可视化-CSDN博客

I'm gonna make all the Tier List from every single dbmlore characters ...

GitHub - KinH8/Realized-GARCH: Incorporating a realized measure of ...

基于LSTM-GARCH模型的投资组合波动预测研究【主要目的是比较传统计量经济学模型与深度学习技术在预测金融市场波动方面的性能】(Python ...

(PDF) Volatility, correlation and risk spillover effect between freight ...

如何利用ARMA-GARCH模型进行预测? - 知乎

时间序列--GARCH模型 - 知乎

Garch-M model - International Review of Financial Analysis 91 (2024 ...

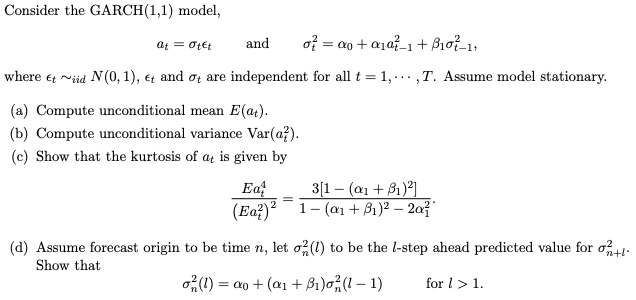

Consider the GARCH(1,1) model, at = 04€ and oź = «p + | Chegg.com

3 Empirical Modeling of High Income and Emerging Stock and Forex Market ...

Time Series Economertics Semester-3 Modelling Stock Return Volatility ...

FuturesAnalysis-ARMA-GARCH-MonteCarlo/ARMA-GARCH及蒙特卡洛模拟.ipynb at main ...

:max_bytes(150000):strip_icc():format(webp)/GARCH-9d737ade97834e6a92ebeae3b5543f22.png)

:max_bytes(150000):strip_icc()/GettyImages-2044493481-148ab08717b941efa4c6d4621233dc64.jpg)