Showing 120 of 120on this page. Filters & sort apply to loaded results; URL updates for sharing.120 of 120 on this page

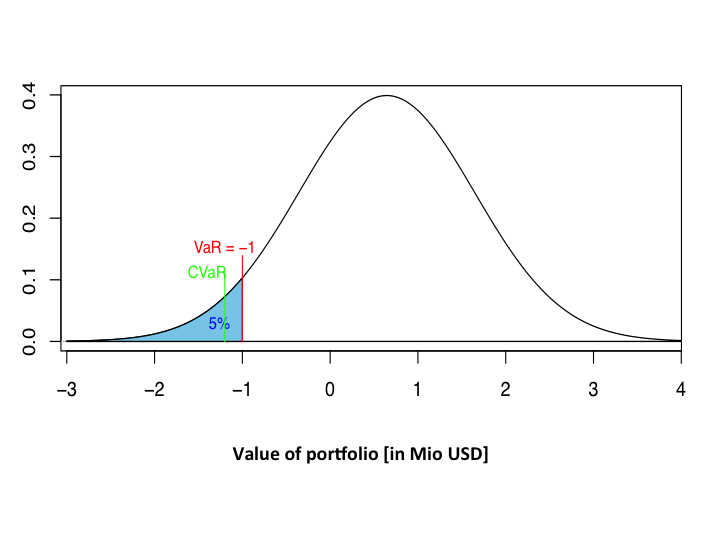

VaR and CVaR in case of normal distribution Source: the authors' own ...

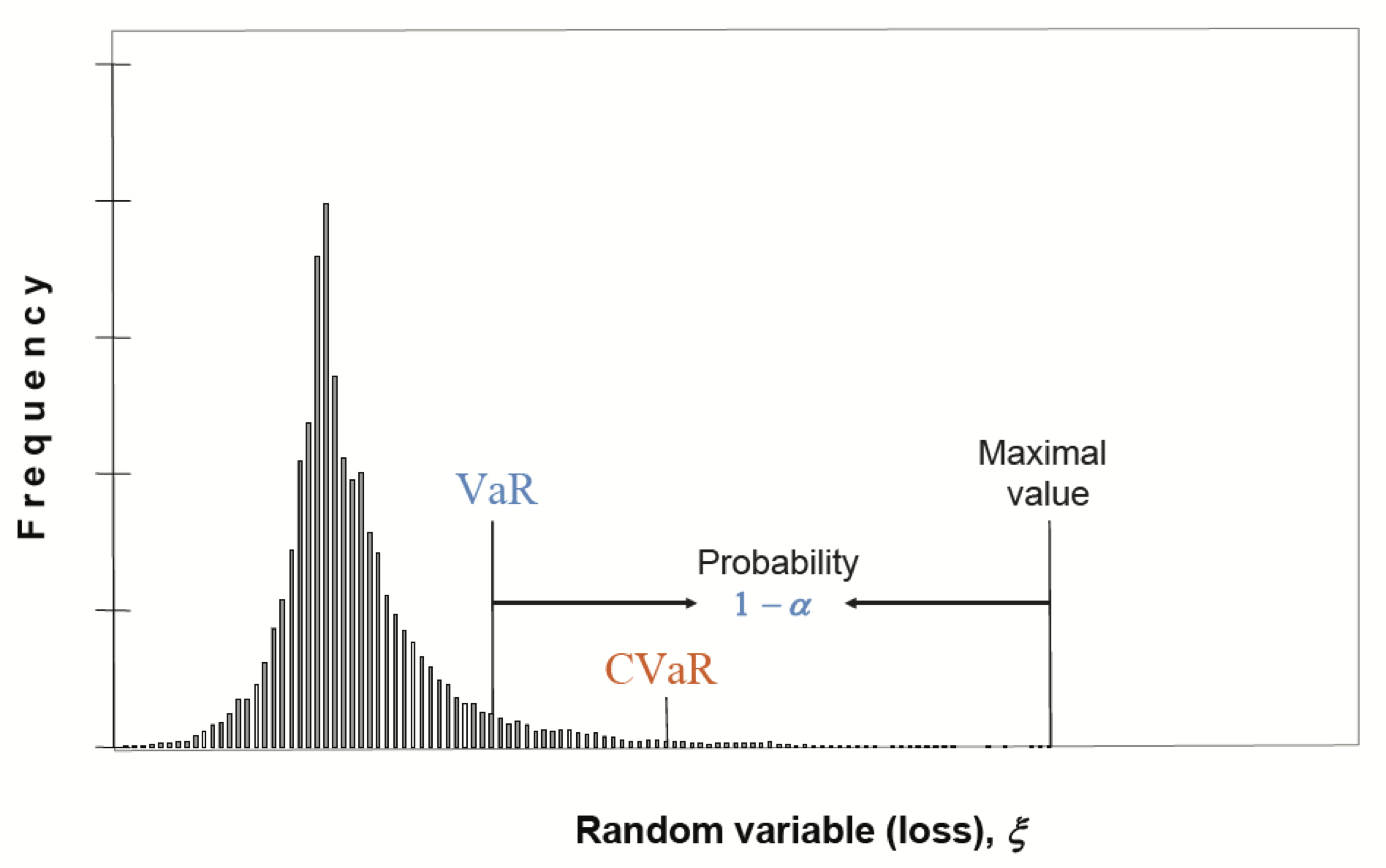

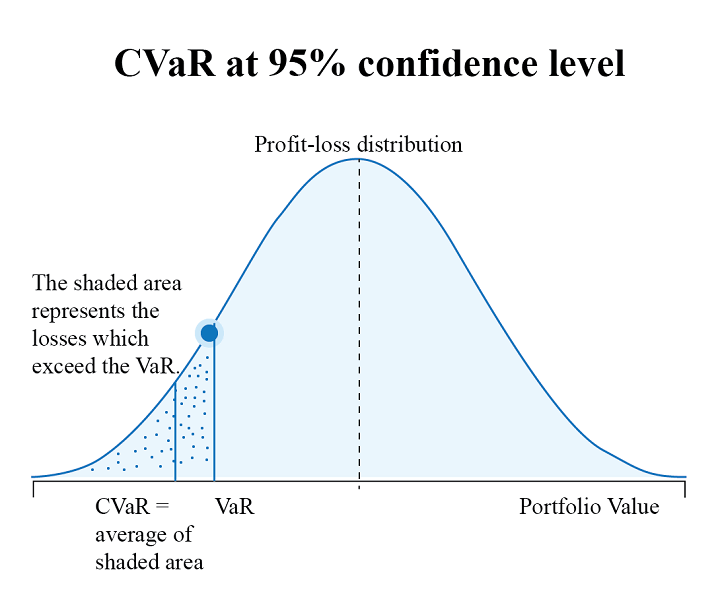

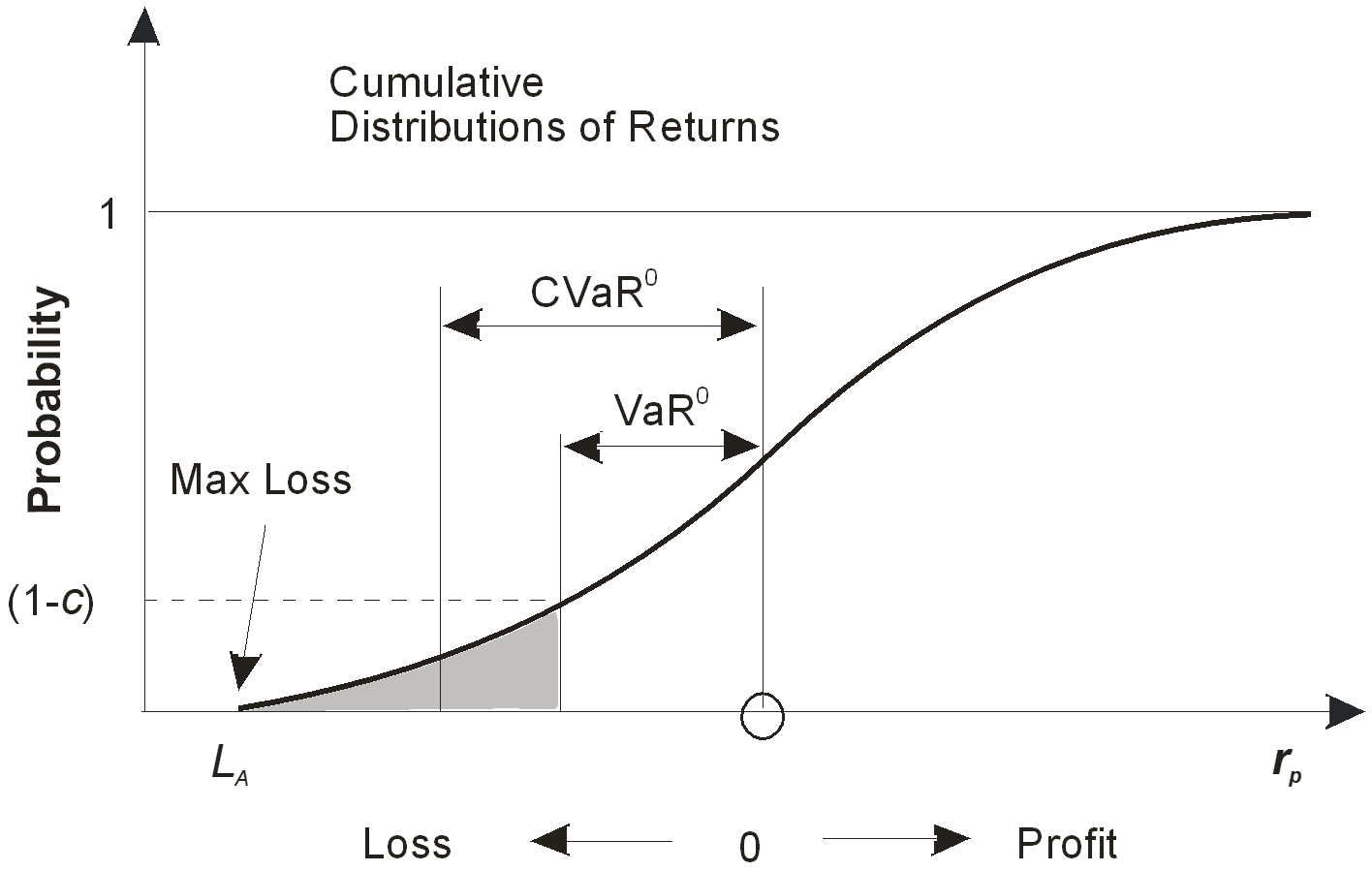

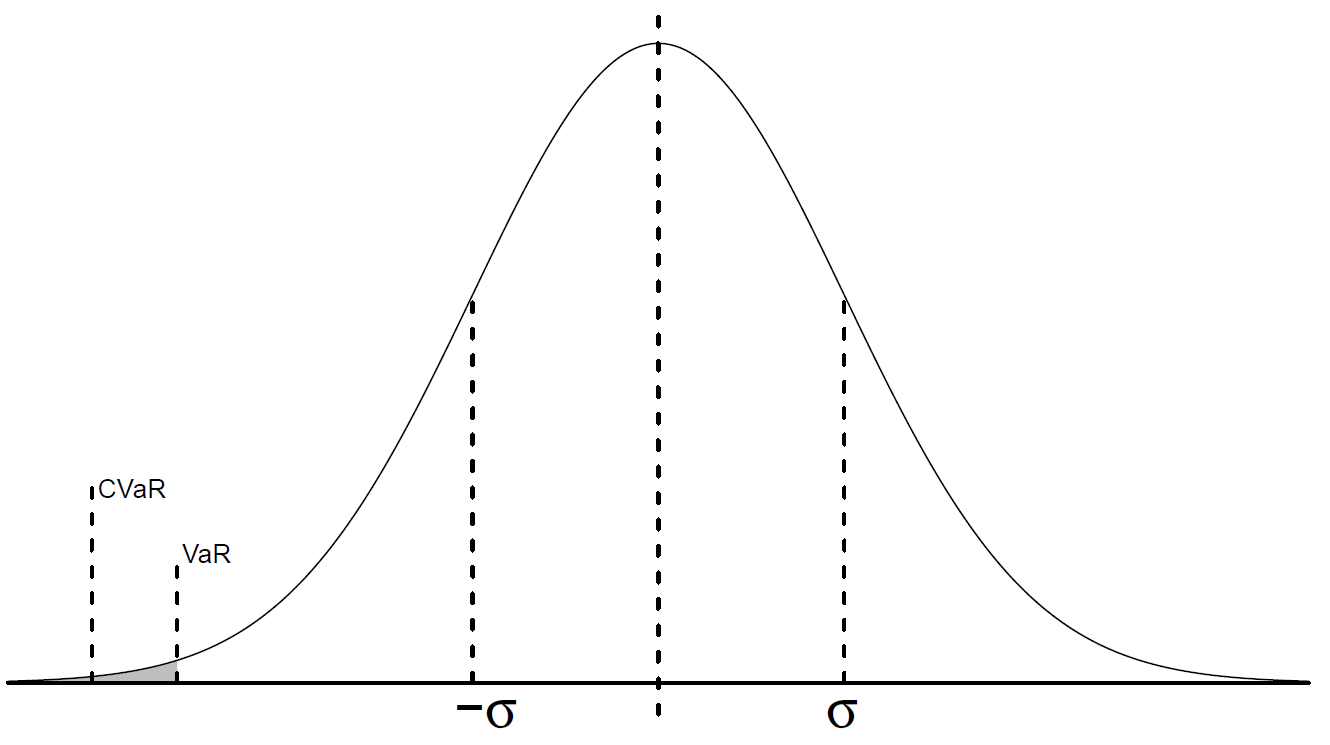

Representation of the Rmin, VaR and CVaR in a normal distribution ...

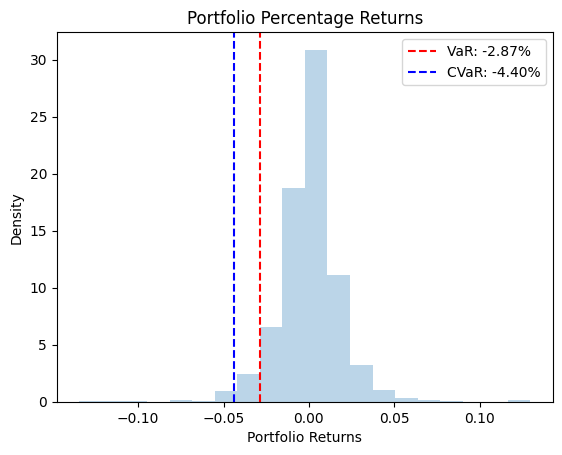

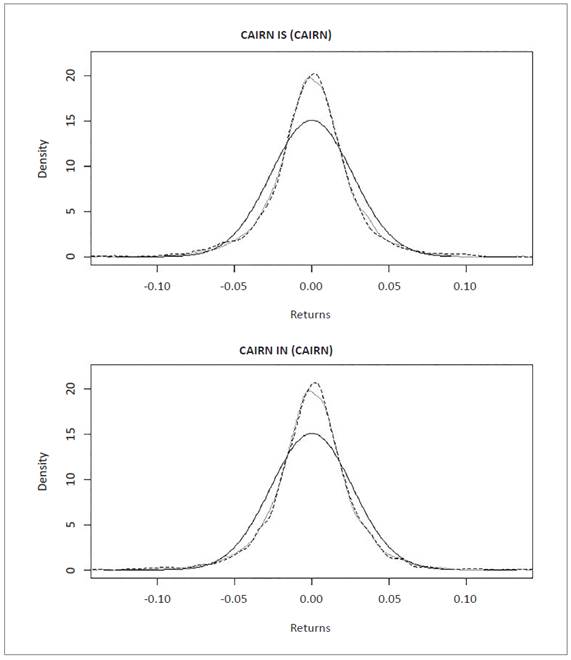

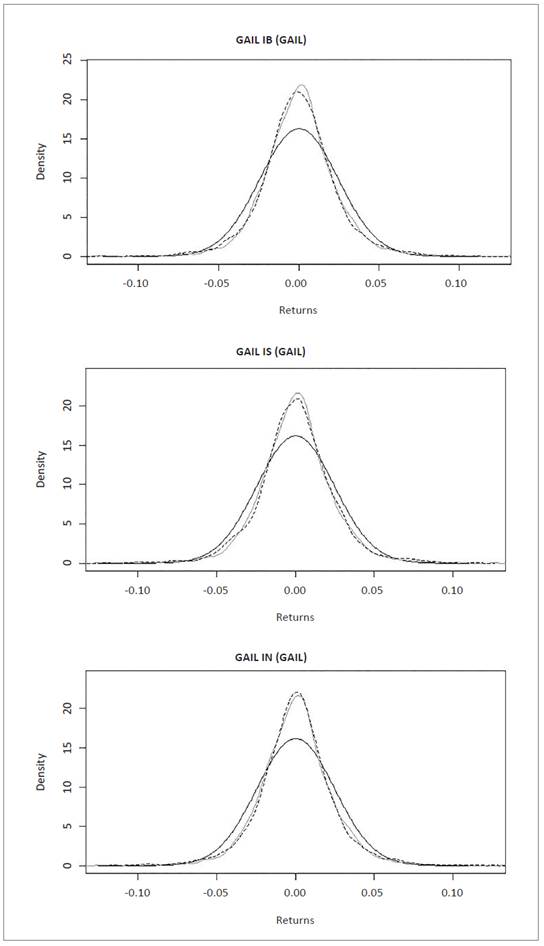

Comparison of VaR and CVaR series based on Normal Distribution of GARCH ...

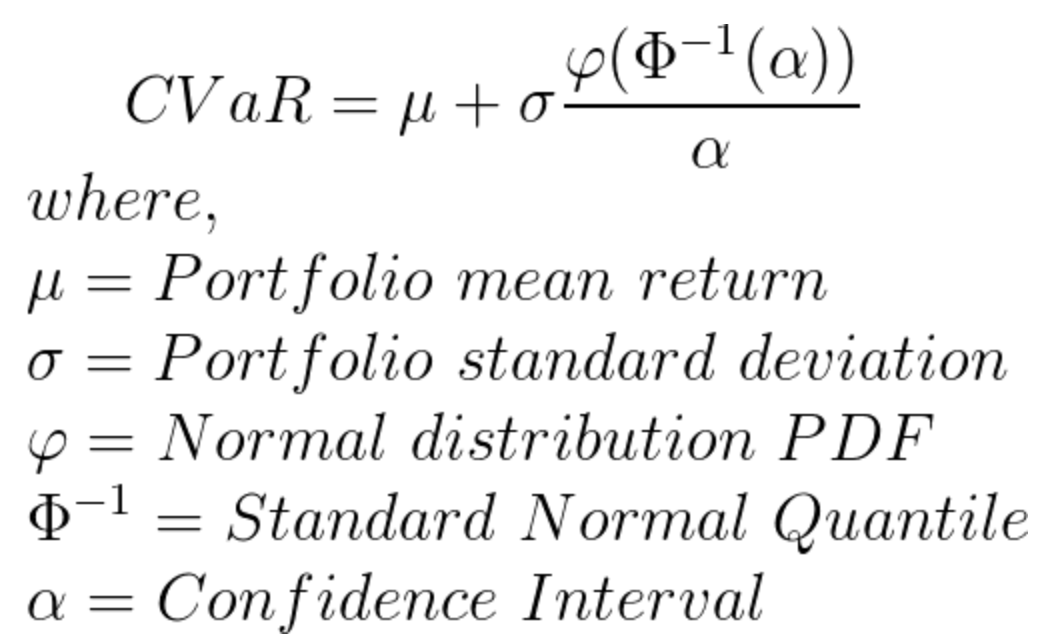

α-VaR and α-CVaR for a normal random variable, where the distribution ...

Illustration of mean and CVaR with α = 0.95 for an example distribution ...

SPY : Conditonal Value-at-Risk (CVaR) Normal and Student t distribution ...

Effectiveness analysis between a normal distribution and Student's ...

Comparison of VaR and CVaR under normal and extreme value distributions ...

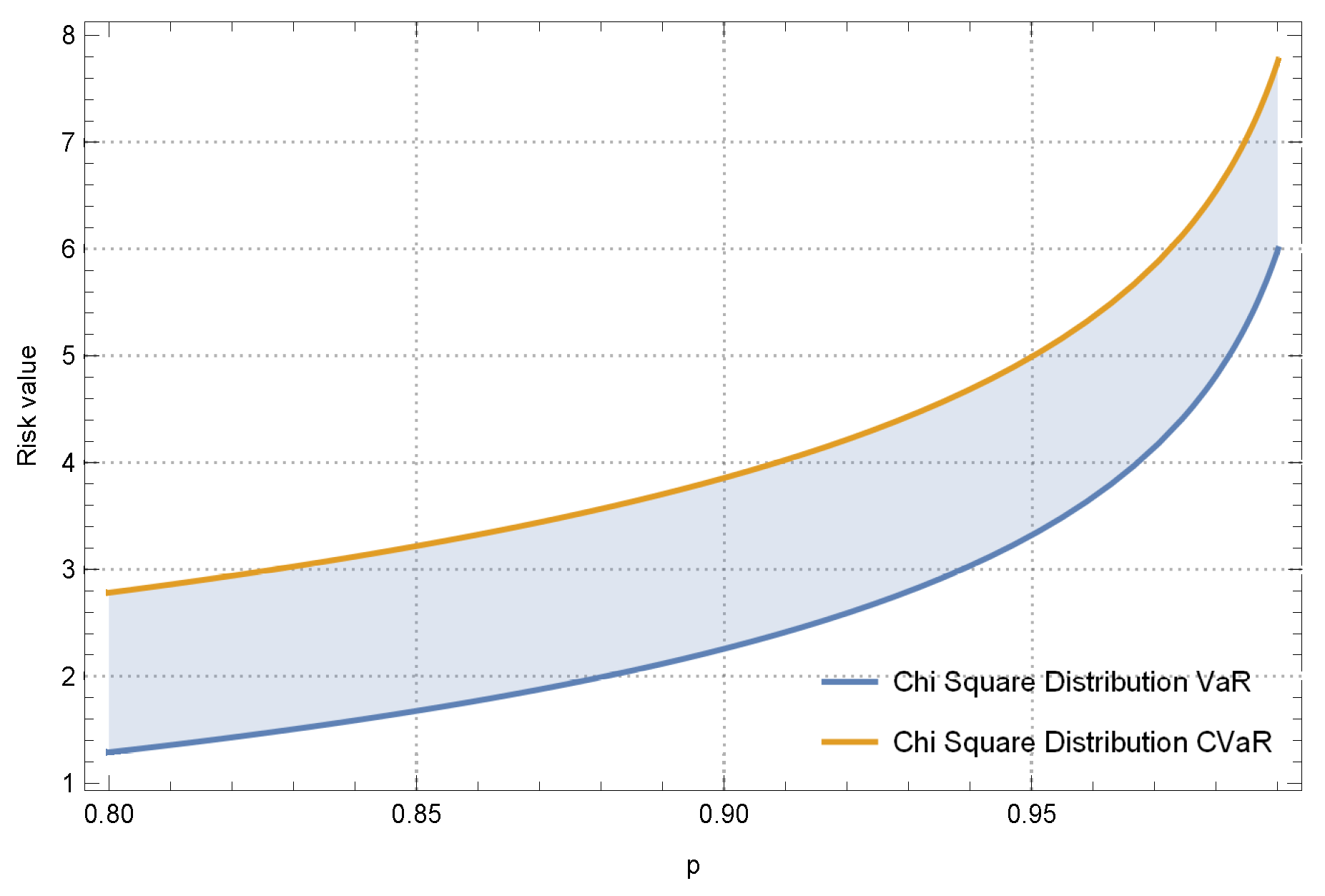

Managing the Risk via the Chi-Squared Distribution in VaR and CVaR with ...

Volatility, VaR and CVaR in a (a) loss and (b) revenue distribution ...

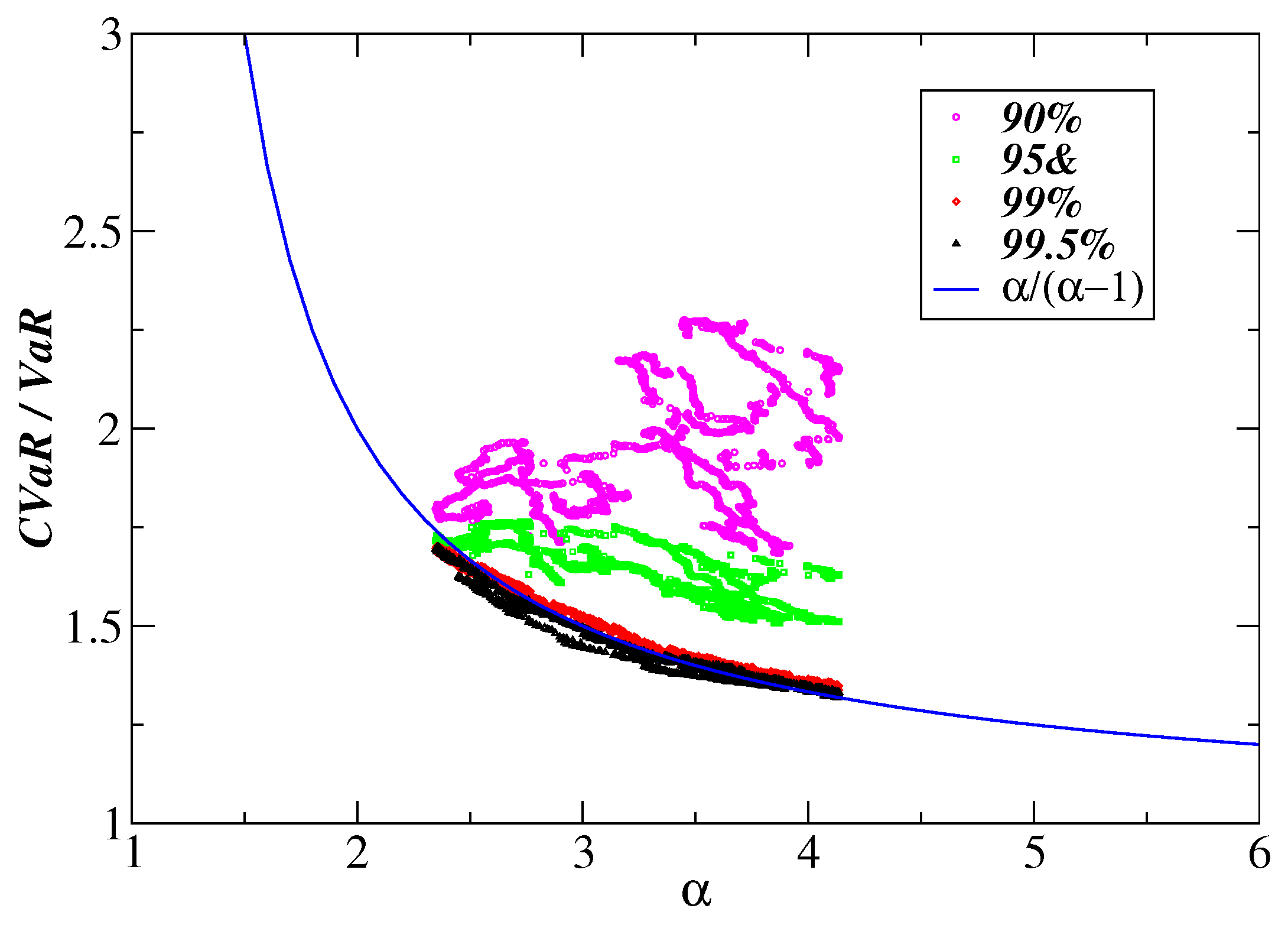

1. CVaR bounds and normal approximation as percentages of µ S ...

Distributions of VaR and CVaR for Normal and Student-t distributions ...

Learned value distribution at distance B = 100 m. The CVaR parameter is ...

VaR and CVaR Estimates in BRIC’s Oil Sector: A Normal Inverse Gaussian ...

Distribution of losses in Case C with minimum CVaR and maximum expected ...

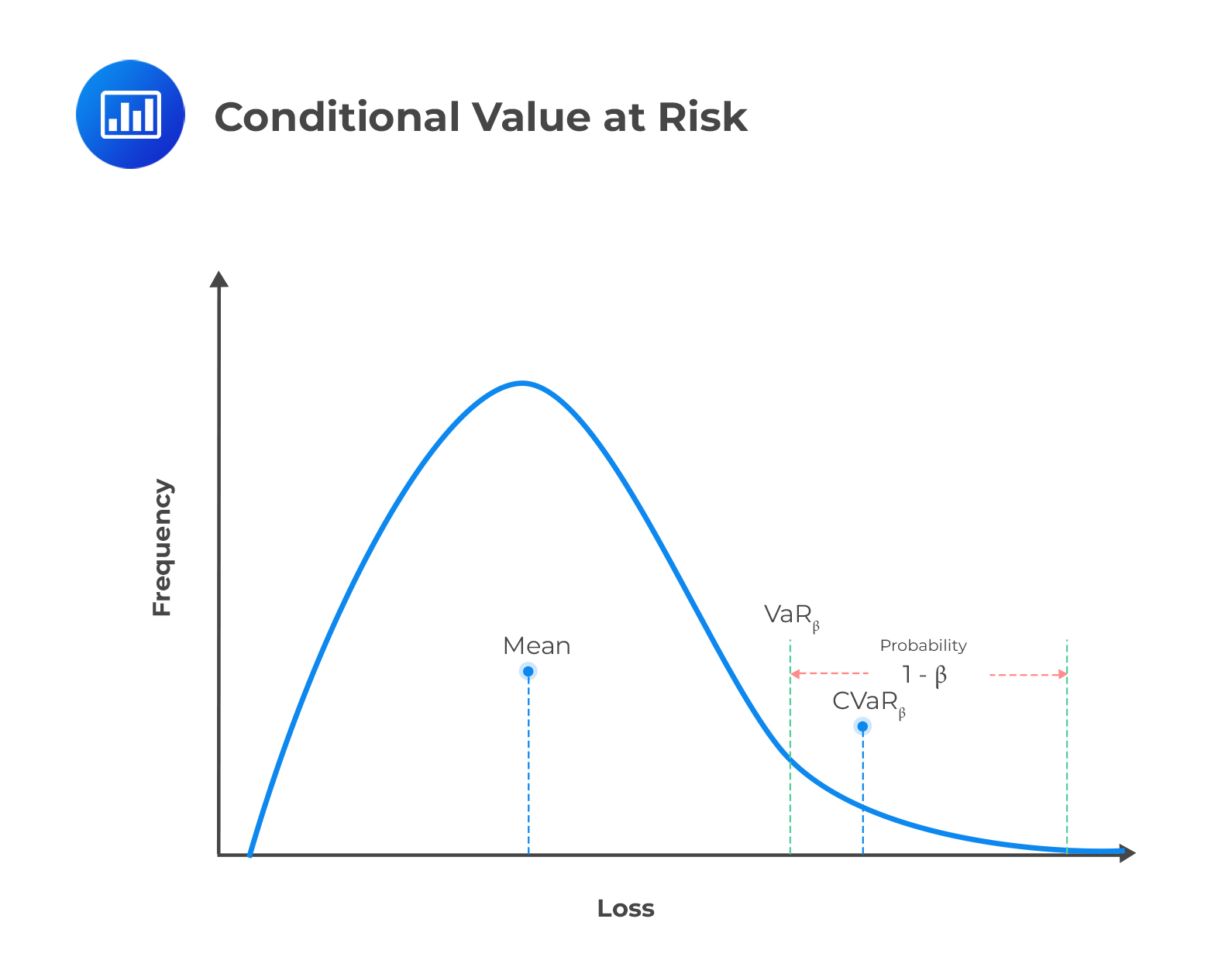

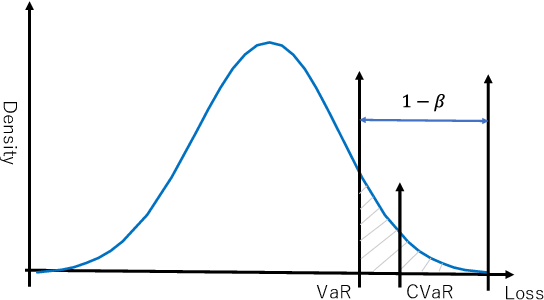

The CVaR description in a probability distribution function (PDF ...

Example of a final time distribution with VaR 1−α and CVaR 1−α marked ...

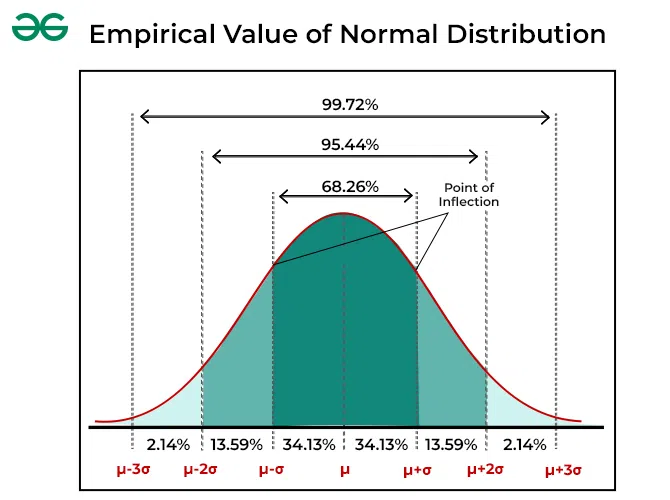

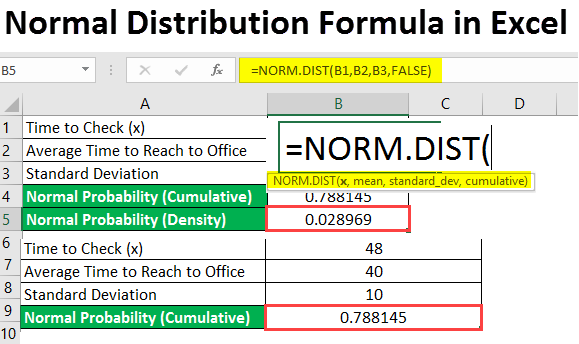

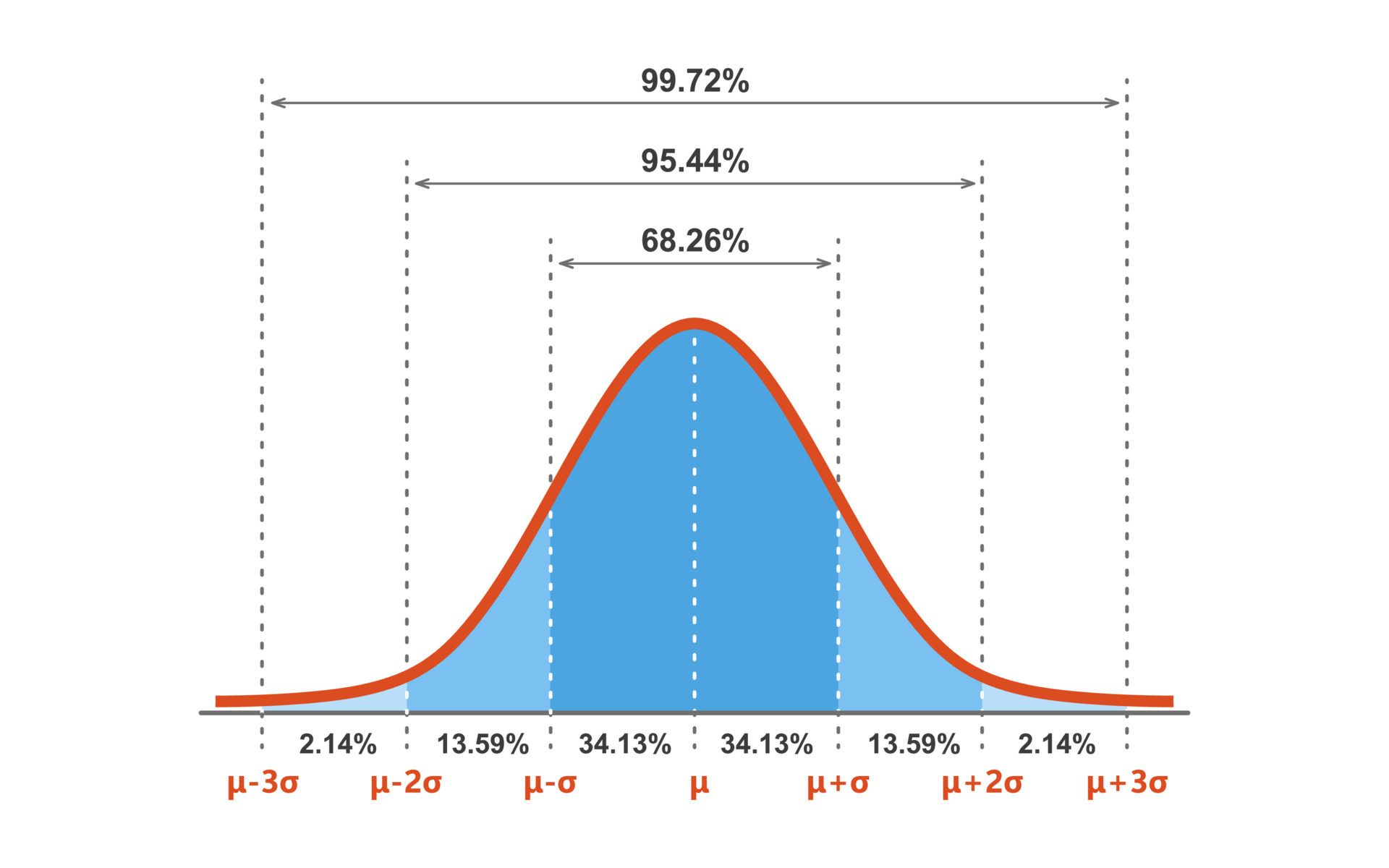

Normal Distribution Formula

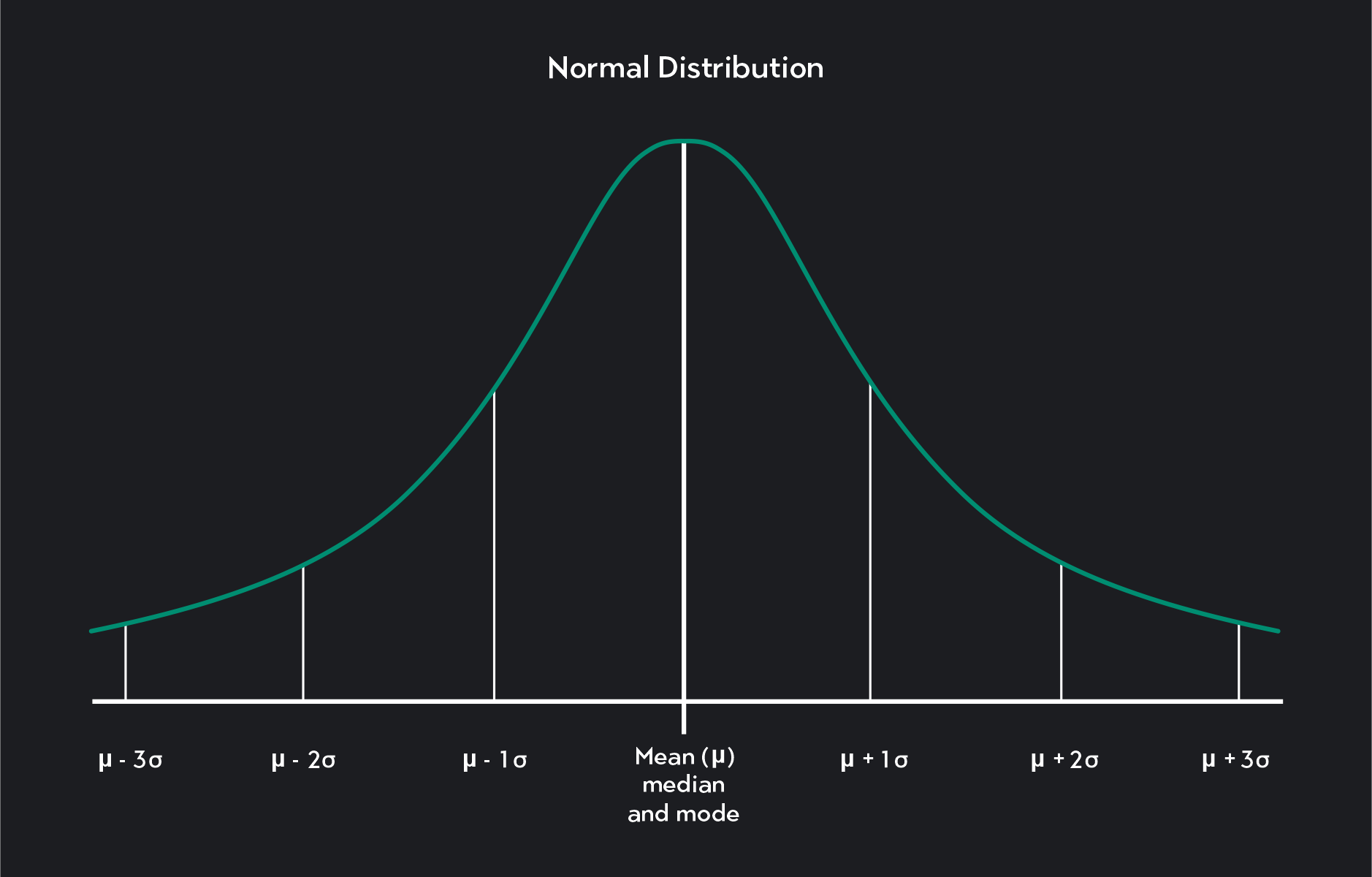

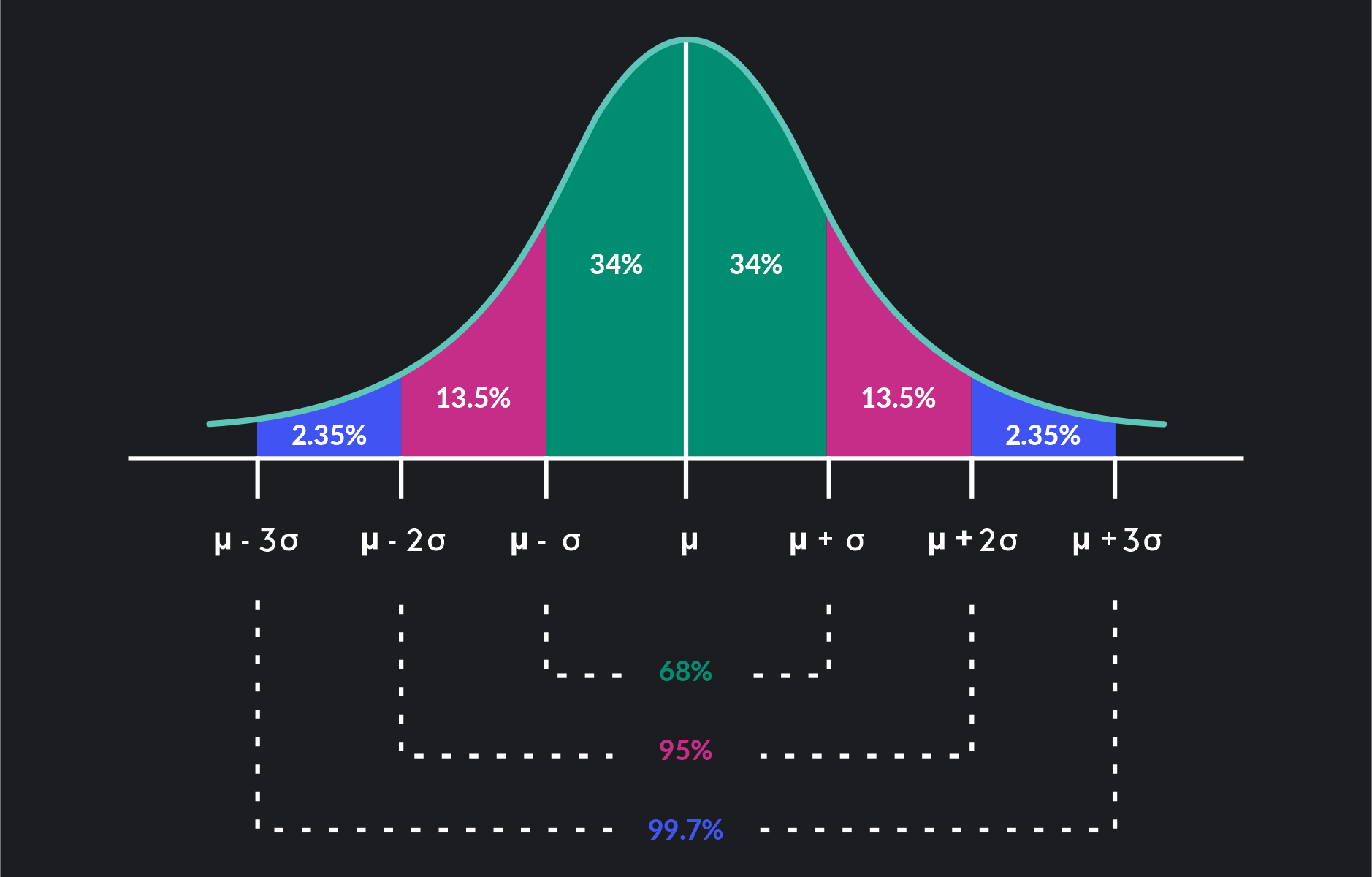

Understanding the Normal Distribution Curve | Outlier

CVaR vs. expected value and revenue distribution in Example 2 ...

How Do I Plot A Normal Distribution Curve In Excel - Design Talk

Example distribution over costs to showcase VaR and CVaR with threshold ...

The Concise Guide to Normal Distribution

CVaR at mean of the sampling distribution and trajectory of risk level ...

Standard normal curve distribution table - listingsopl

Normal Distribution | Examples, Formulas, & Uses

Ch. 6 Normal Distribution Excel Tutorial - YouTube

Normal Distribution Table

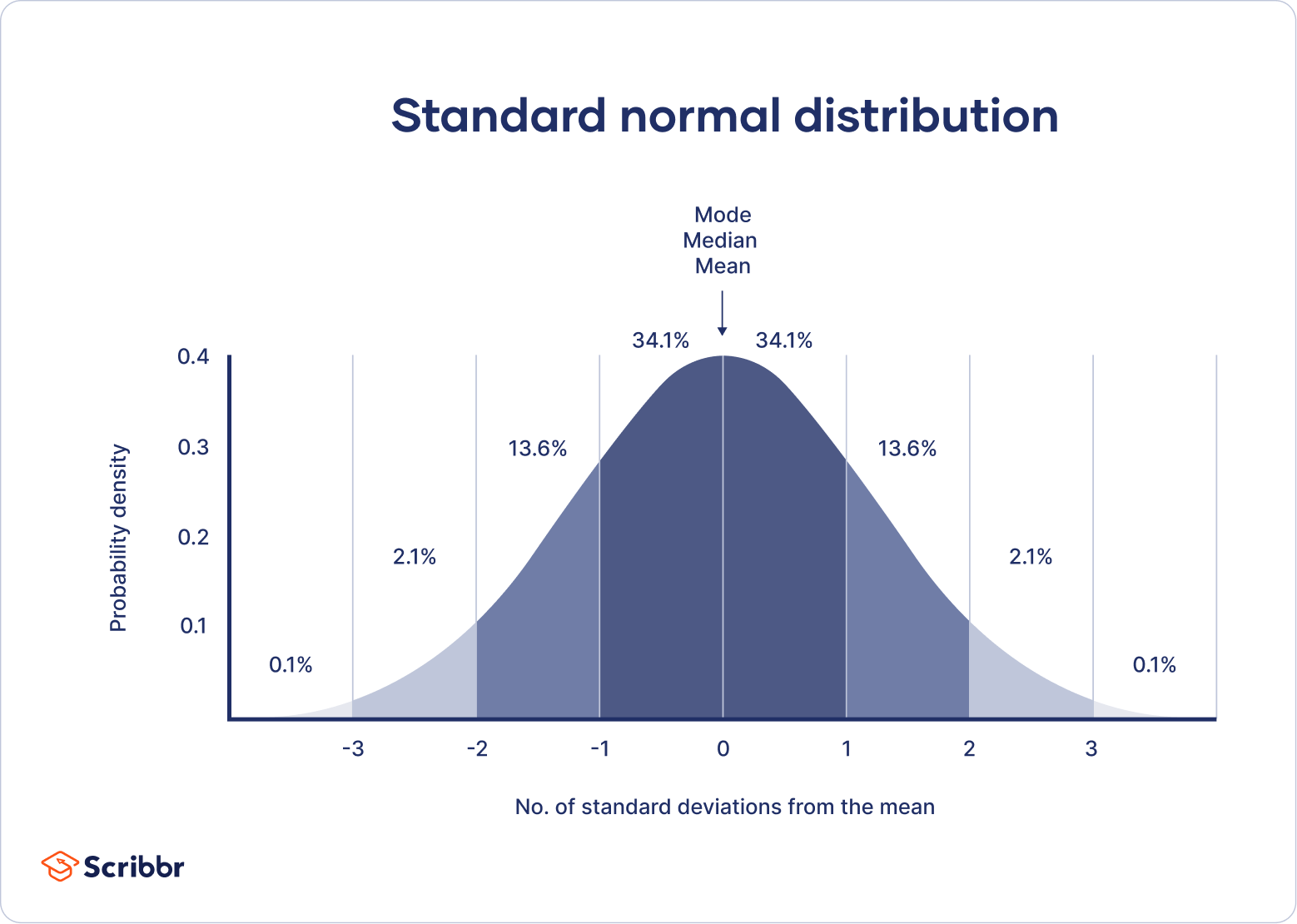

Normal Distribution in Business Statistics - GeeksforGeeks

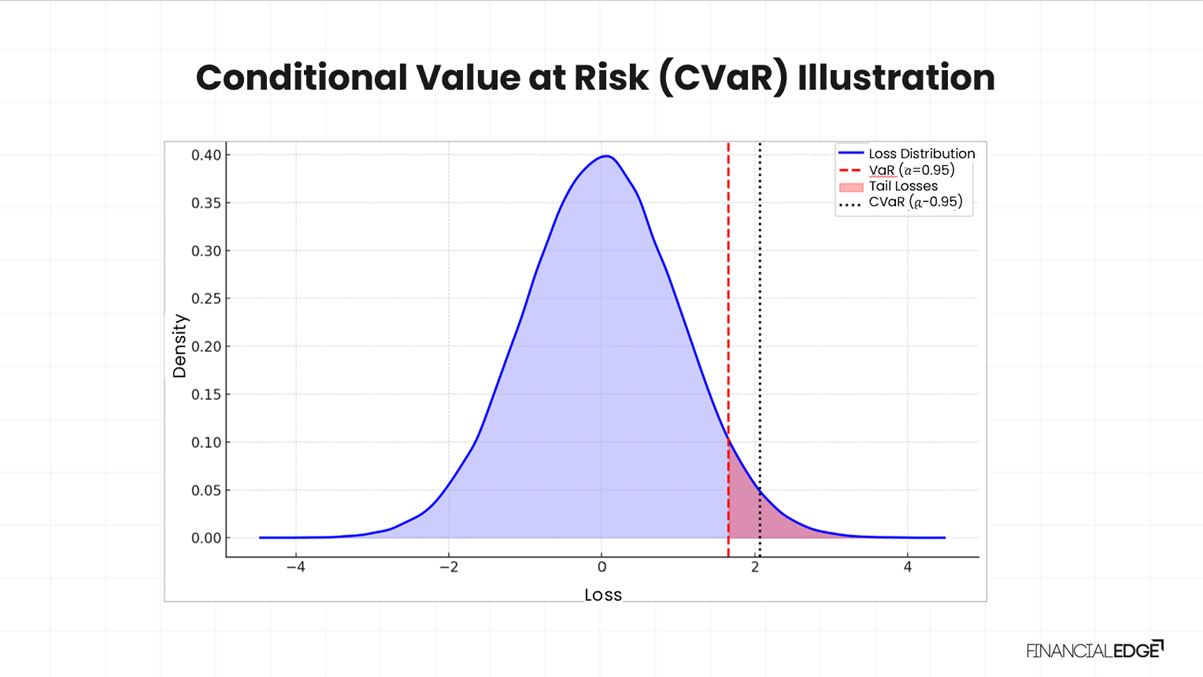

Illustrating the CVaR of a Gaussian distribution. The red area under ...

Example of VaR and CVaR at risk level β = 0.9. | Download Scientific ...

Risk functions: graphical representation of VaR, VaR Deviation, CVaR ...

CVaR and VaR -Probability Density Function Source: Lleo 2009, p. 12 ...

CVaR and VaR representation. | Download Scientific Diagram

VaR and CVaR values for the elementary example. | Download Scientific ...

Properties of VaR and CVaR Risk Measures in High-Frequency Domain: Long ...

Parametric VaR and CVaR (Gaussian/Normal Distribution) in Excel - YouTube

Illustrative example to show how CVaR is a more relevant risk metric ...

represents the CVaR in terms of costs. | Download Scientific Diagram

VaR and CVaR illustration. | Download Scientific Diagram

VaR and CVaR Graphical Representation | Download Scientific Diagram

A visualization of VaR and CVaR concepts. | Download Scientific Diagram

VaR and CVaR under the confidence level α (= 0.95), where x is a random ...

Graphical representation of CVaR for a discrete probability ...

VaR and CVaR Representation [35]. | Download Scientific Diagram

Representation of CVaR and VaR. | Download Scientific Diagram

VaR, CVaR and deviations adapted from Sarykalin et al. [74]. | Download ...

Graphical representation of VaR and CVaR | Download Scientific Diagram

Illustration of CVaR and CVaR-based deviation measure. | Download ...

(a) Cyber-Risk Aggregation Performance (on the CVaR Metric) for i.i.d ...

Calculating CVaR in Excel: Step-by-Step Guide

Illustration of mean and CVaR | Download Scientific Diagram

CVaR Example 1: computation of CVaR when α does not spilt the atom ...

Diagram of the VAR and CVAR calculation. | Download Scientific Diagram

Percentage CVaR contribution of asset 1 in function of its portfolio ...

VaR and CVaR Optimal Values for Various Confidence Levels | Download ...

Portfolio Optimization with CVaR - My Notes

VaR and CVaR Deviations [Source: Sarykalin et al (2008)] | Download ...

Demostración VaR-CVaR Normal | PDF | Distribución normal | Variable ...

The behaviour of robust CVaR as a function of | Download Scientific Diagram

CVaR estimates for the three portfolios | Download Table

Figure 1 from Exploring the properties of CVaR and Mean-Variance for ...

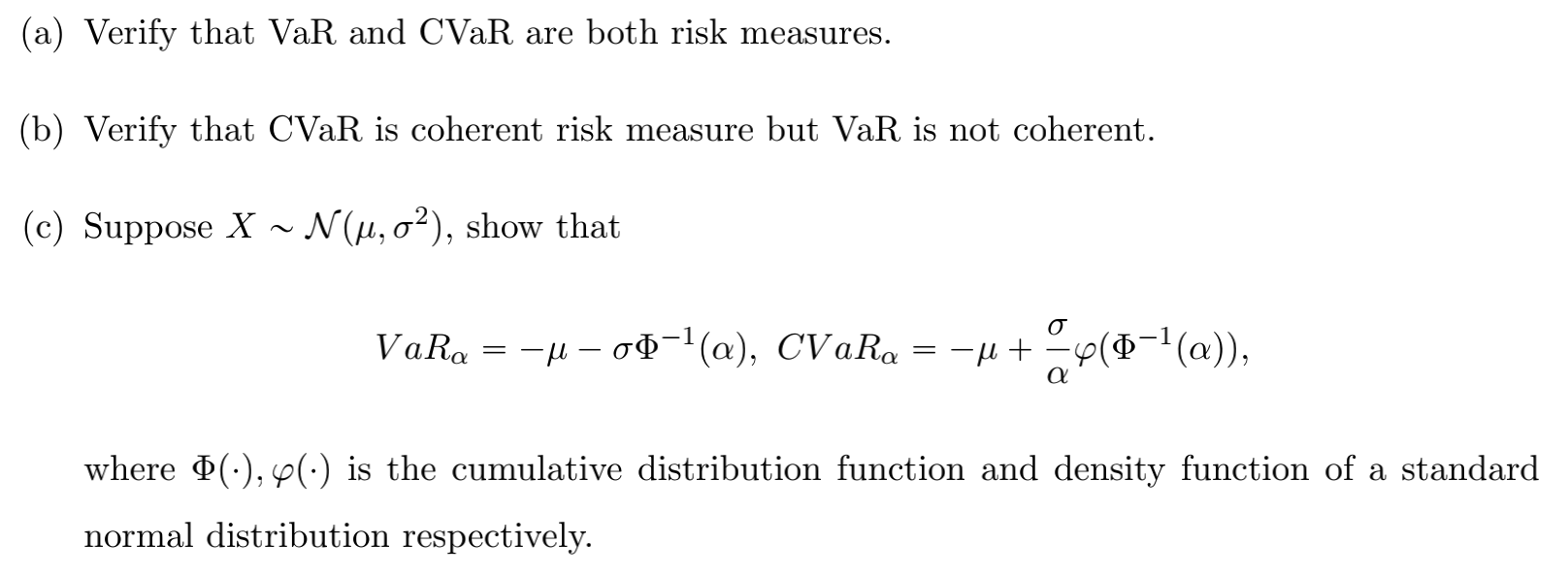

Solved (a) Verify that VaR and CVaR are both risk measures. | Chegg.com

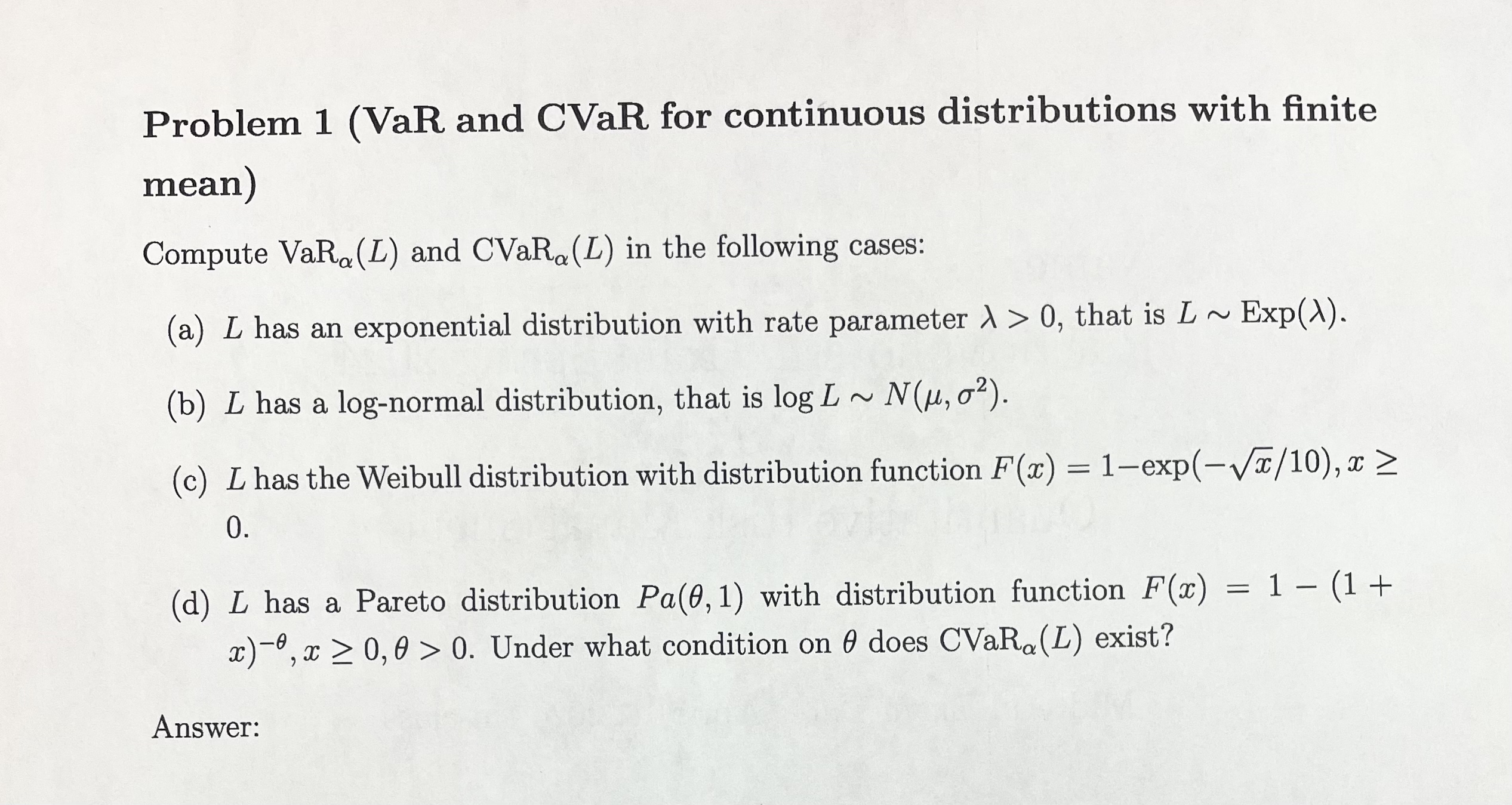

Solved Problem 1 (VaR and CVaR for continuous distributions | Chegg.com

Research on the Efficient Frontier of Mean-CVaR under Normal ...

Conditional Value at Risk (CVaR) or Expected Shortfall: Formula and ...

Capital at Risk vs Value at Risk: Your Investment Risk - Phemex Academy

10.2 Alternative Risk Measures | Portfolio Optimization

Portfolio VaR and CVaR. Scenario | by Nikesh Shrestha | Medium

Conditional value at risk (CVaR) compared with VaR | Download ...

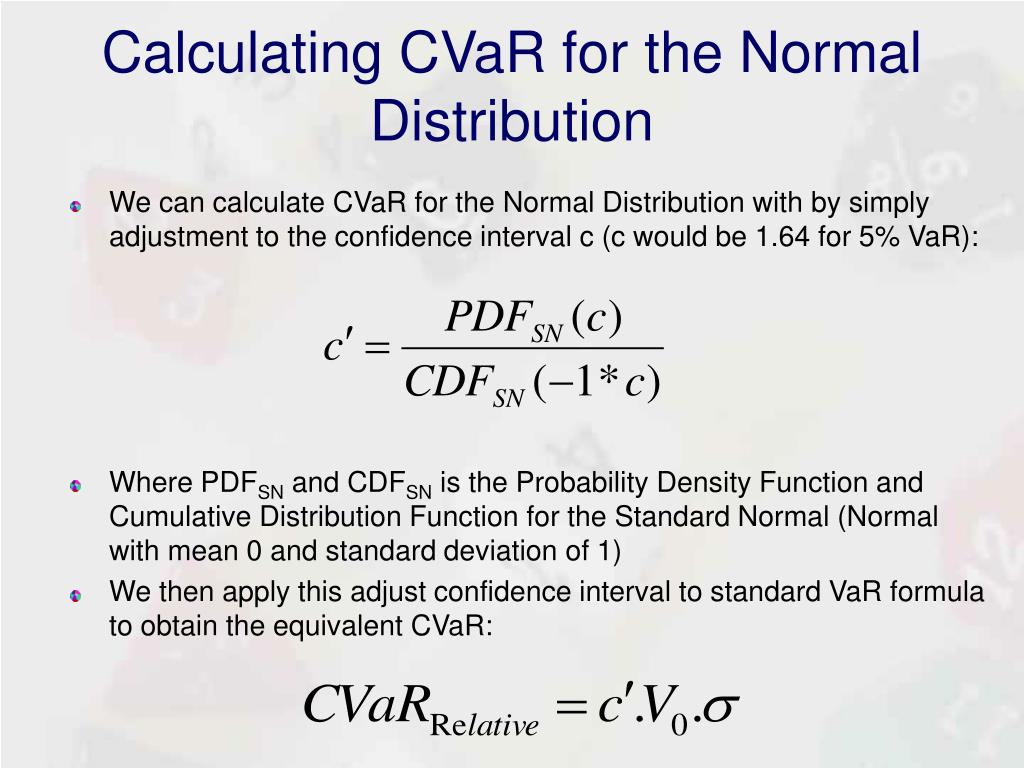

PPT - Risk Analysis & Modelling PowerPoint Presentation, free download ...

Relation to the expected value, VaR, CVaR, and EVaR for a given ...

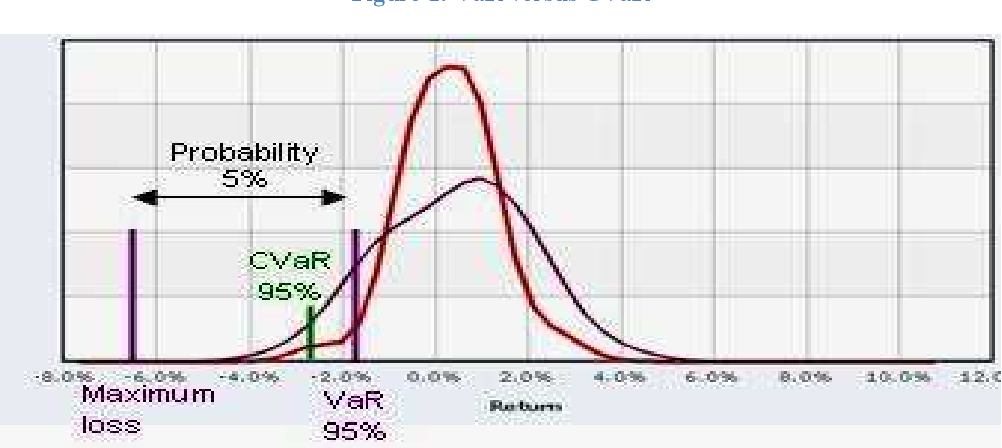

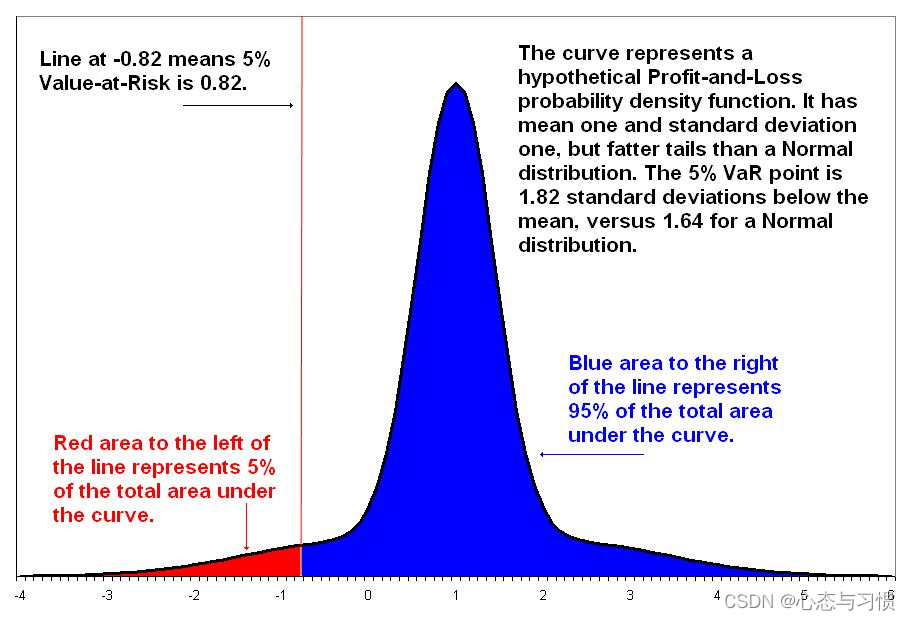

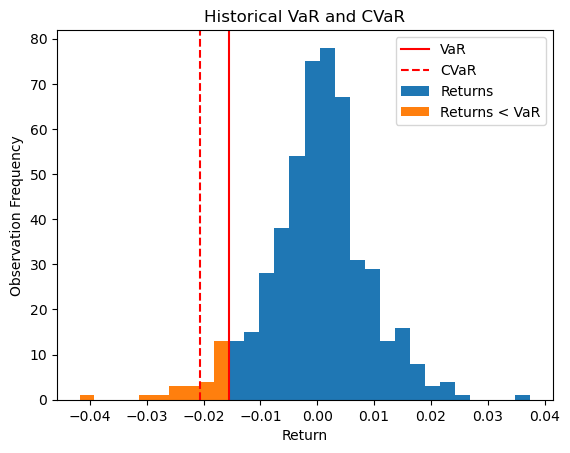

VaR for normally distributed returns at 95% and 99% confidence level ...

Value at Risk: Formula, Calculation, Python and more.

Accelerating Real-Time Financial Decisions with Quantitative Portfolio ...

VaR 与 CVaR_var和cvar-CSDN博客

Conditional Value at Risk Explained - Free Excel Template

Relationship between VaR and CVaR. | Download Scientific Diagram

A graphical depiction of VaR and CVaR. | Download Scientific Diagram

Extensions of VaR | CFA Level II Notes

Managing Risk in Investment Portfolios - A Guide to Calculating VAR and ...

Illustration of Expectation (solid line), FCVaR, WCVaR, HCVaR, VaR, and ...

Conditional Value-at-Risk | Expected Tail Loss | Shortfall Risk

An illustration of risk measures: VaR and CVaR. | Download Scientific ...

Graphical illustration of conditional value at risk (CVaR) in a ...

α -VaR and α -CVaR for a given loss distribution. | Download Scientific ...

A Stochastic-CVaR Optimization Model for CCHP Micro-Grid Operation with ...

Stochastic Programming

VaR and CVaR(shortage) | Download Scientific Diagram

Graphical illustration of CVaR, defined as expected cost of the worst ...

Computation of the corrected Cornish–Fisher expansion using the ...

Conditional Value at Risk (CVaR) | Meaning, Pros, and Cons

求问var 与cvar的区别与比较? - 知乎

Portfolio Optimization using Conditional Value at Risk | Thomas T. Bjerring

Risk management 101: Asset returns are not normally distributed. That's ...

Figure 1 from RM-CVaR: Regularized Multiple β-CVaR Portfolio | Semantic ...

:max_bytes(150000):strip_icc()/dotdash_Final_The_Normal_Distribution_Table_Explained_Jan_2020-04-414dc68f4cb74b39954571a10567545d.jpg)