Showing 120 of 120on this page. Filters & sort apply to loaded results; URL updates for sharing.120 of 120 on this page

FAVAR IMPORT

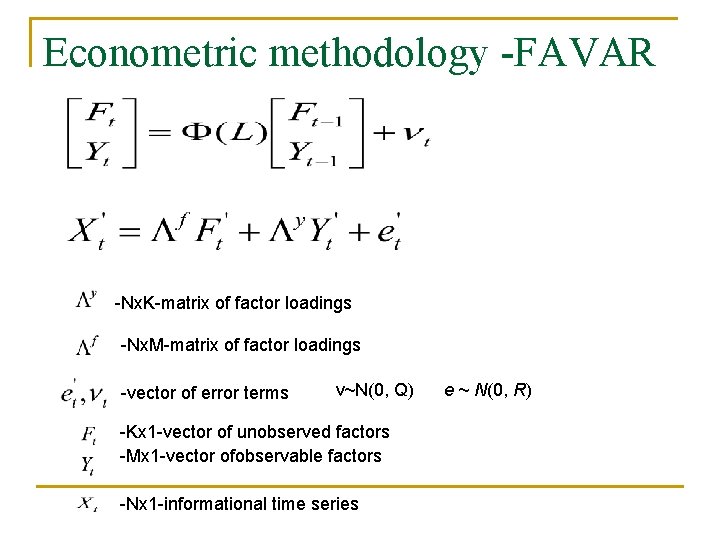

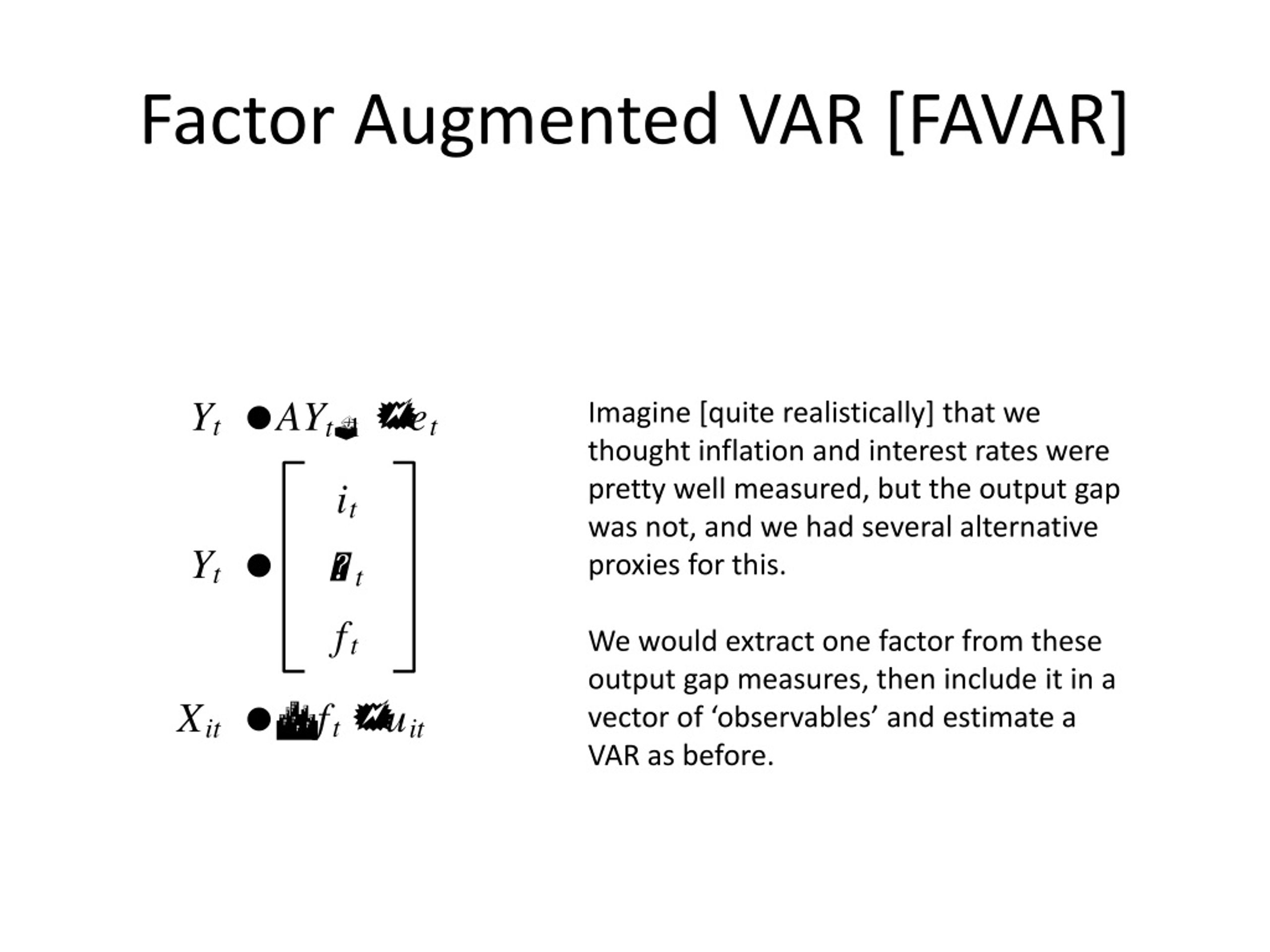

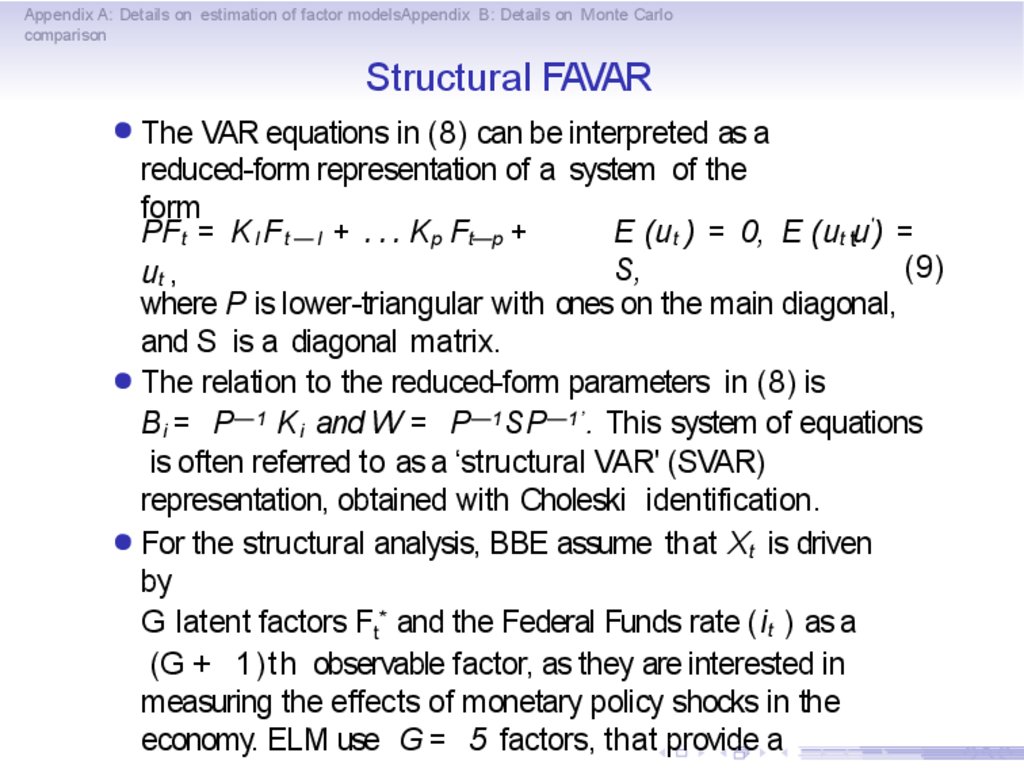

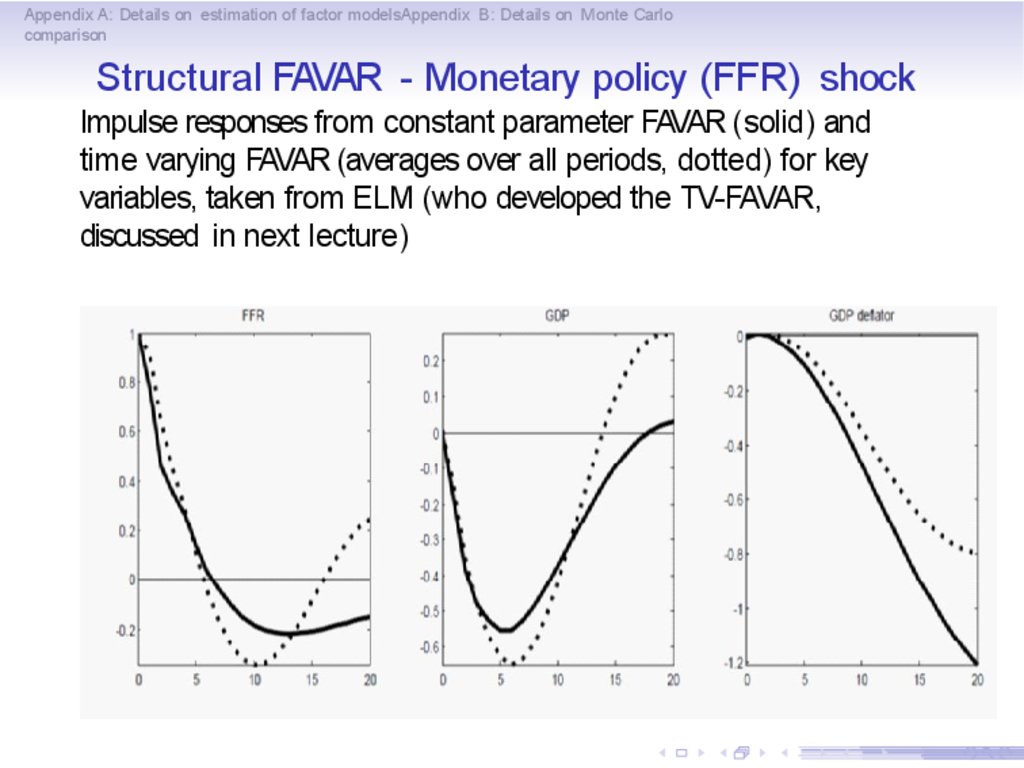

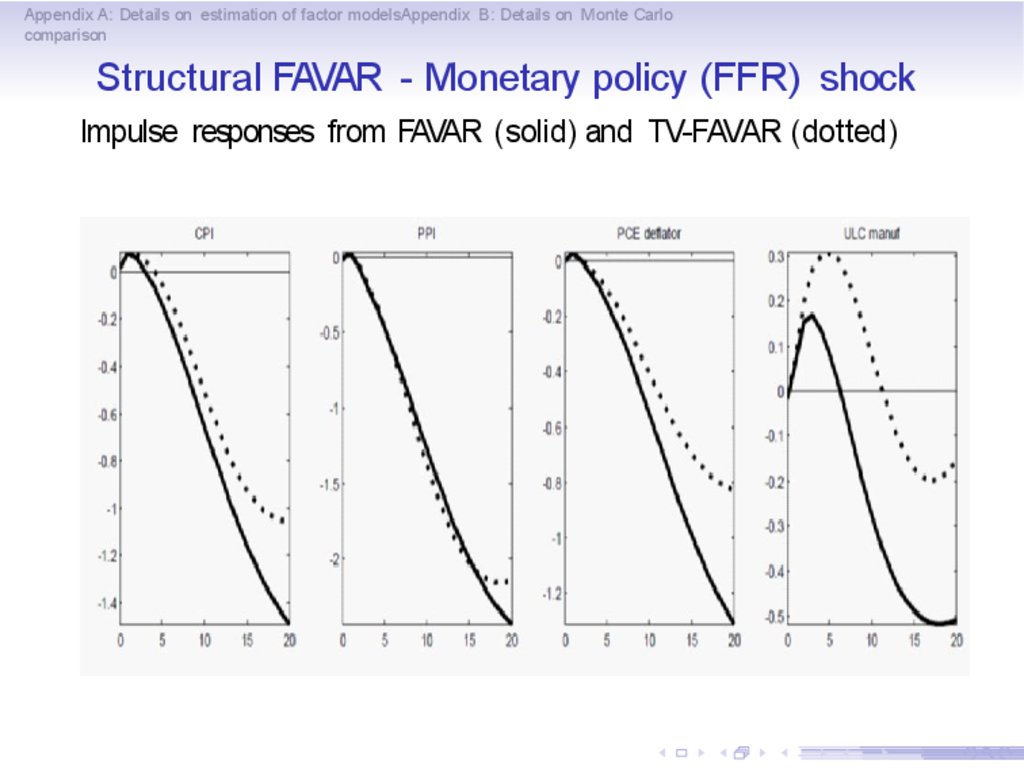

Illustration of A FAVAR model panel A: a typical FAVAR model panel B ...

A FAVAR An alysis of Bu siness Cycle

5-years yield Term Premium from MS-FAVAR and FAVAR models. | Download ...

(PDF) FAVAR (Factor-Augmented Vector Autoregression) Modeli Literatür ...

Favar Package | PDF | Vector Autoregression | Statistical Analysis

Figure C.25: R 2 plot for the FAVAR based on principal components ...

FAVAR Impulse Response Functions | Download Scientific Diagram

FAVAR | PDF | Autoregressive Model | Statistical Theory

FAVAR Select Impulse Response Functions to Monetary Policy Uncertainty ...

Summary of the model features for the Deep Dynamic FAVAR | Download ...

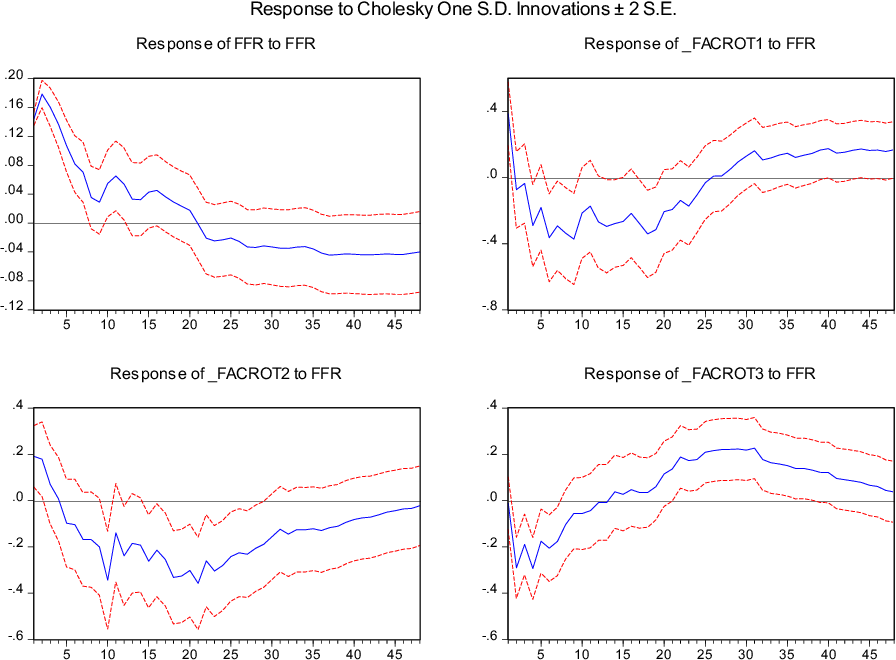

Impulse-Response Functions Estimated with a favar Model | Download ...

FAVAR | PDF | Vector Autoregression | Inflation

FAVAR with four factors | Download Scientific Diagram

FAVAR Impulse Responses of Common Factor | Download Scientific Diagram

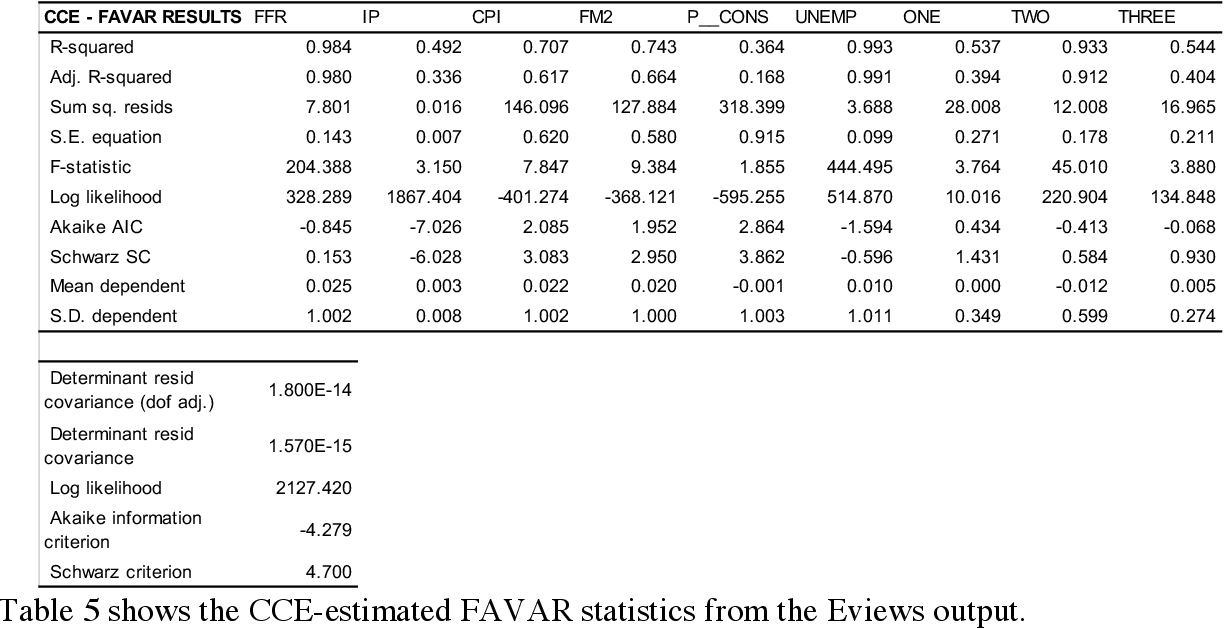

Table 5 from A simplified approach in FAVAR estimation | Semantic Scholar

The Forecasting Performance of the First and Last Iterations of a FAVAR ...

Studies on the Monetary FAVAR Models with Two-stage Estimation ...

FAVAR Approach: Full Sample Period | Download Scientific Diagram

Parameter estimates of the FAVAR model (Commodity indices). | Download ...

GitHub - LarsHernandez/FAVAR: VAR and FAVAR models in R for 8th ...

Figure 4 from A simplified approach in FAVAR estimation | Semantic Scholar

(PDF) Estimation of FAVAR Models for Incomplete Data with a Kalman ...

Orgulloso de formar parte de Favar Import S.A ️ | Fernando Drago

Favar - Dicio, Dicionário Online de Português

Spain, Impulse Response Function generated from FAVAR with four Factor ...

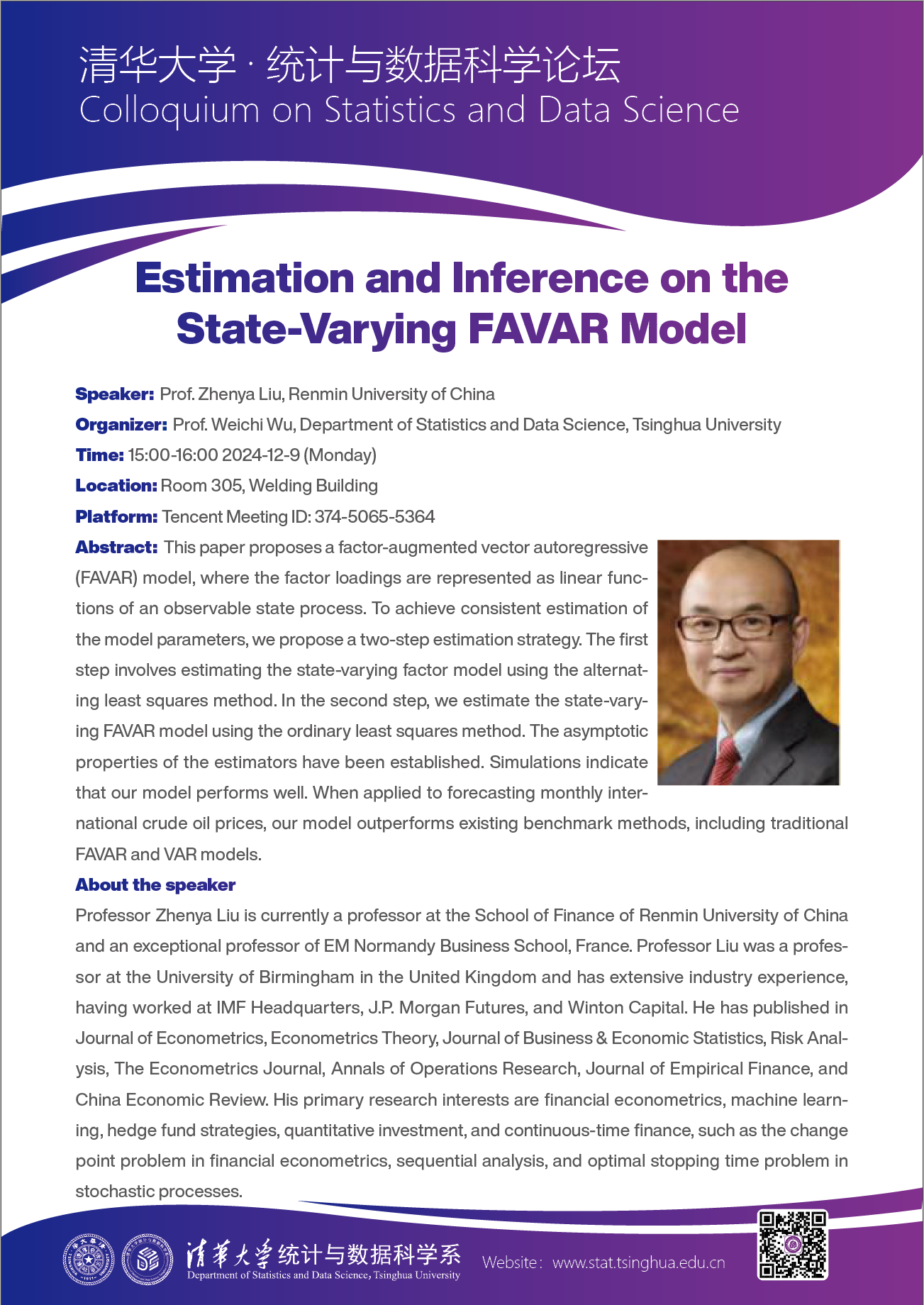

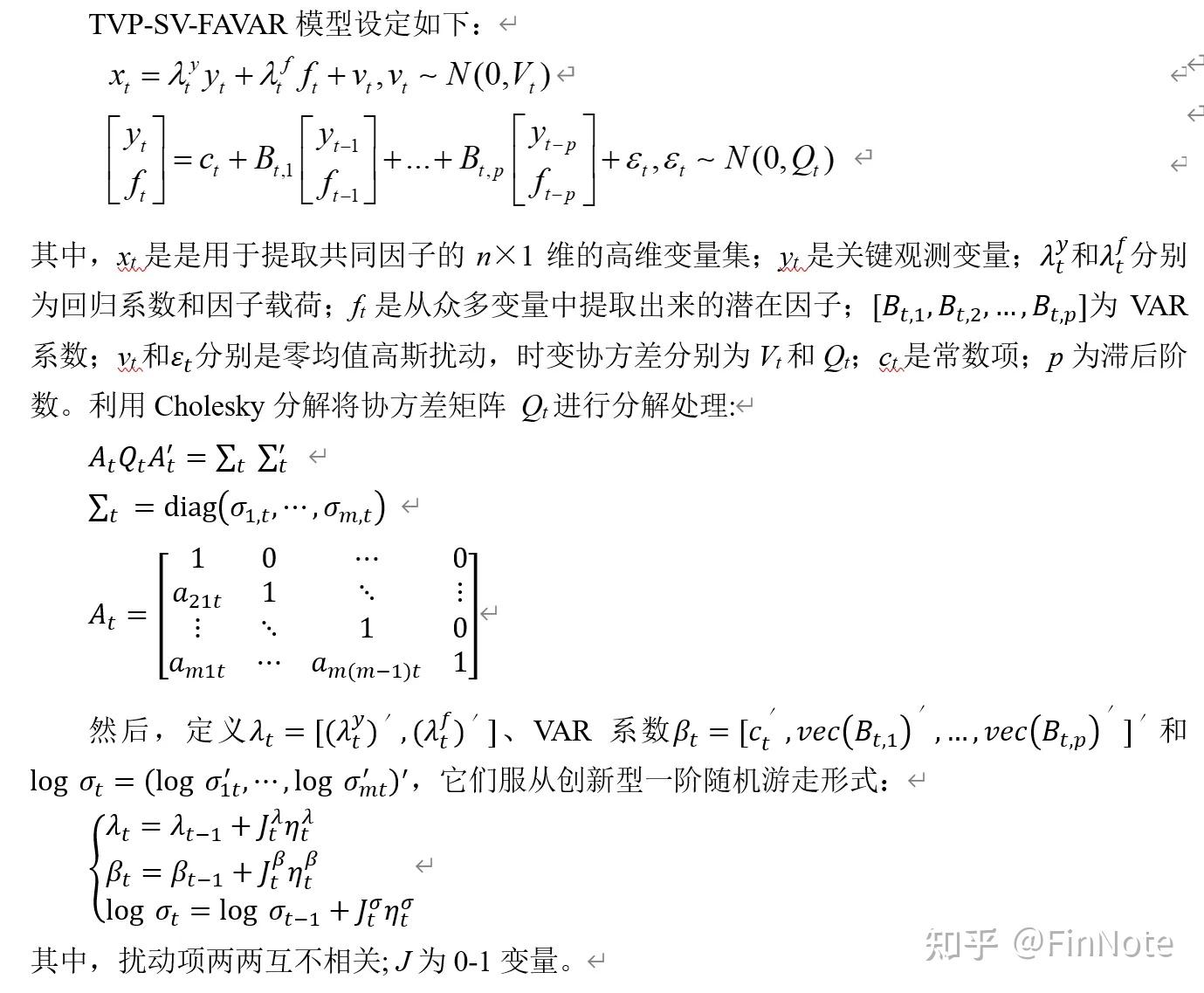

【统计与数据科学论坛】Estimation and Inference on the State-Varying FAVAR Model-清华 ...

Figure 1 from Identifying Observed Factors in FAVAR Models: A Bayesian ...

Impulse-responses for FAVAR incl. differences in transaction value in ...

Estimation of FAVAR Models for Incomplete Data with a Kalman Filter for ...

(a). Parameter estimates of the FAVAR model with respect to United ...

Estimation and inference of FAVAR models Munich Personal RePEc Archive

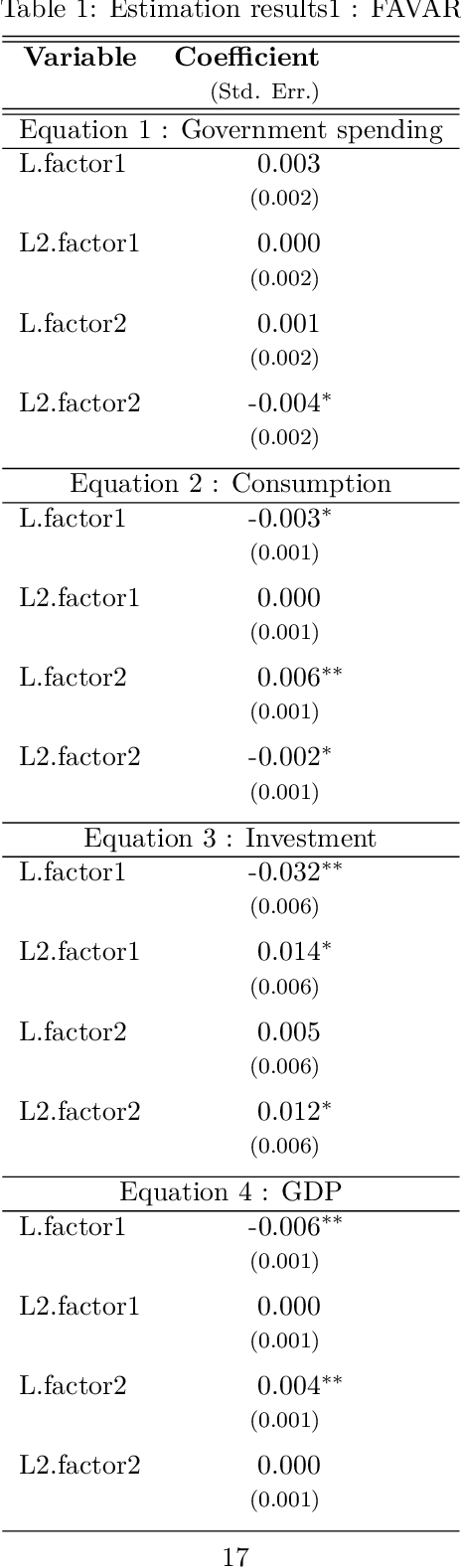

Table 1 from The Dynamic Effects of Fiscal Policy : A FAVAR Approach ...

The Impact of External Shocks on Emerging Countries

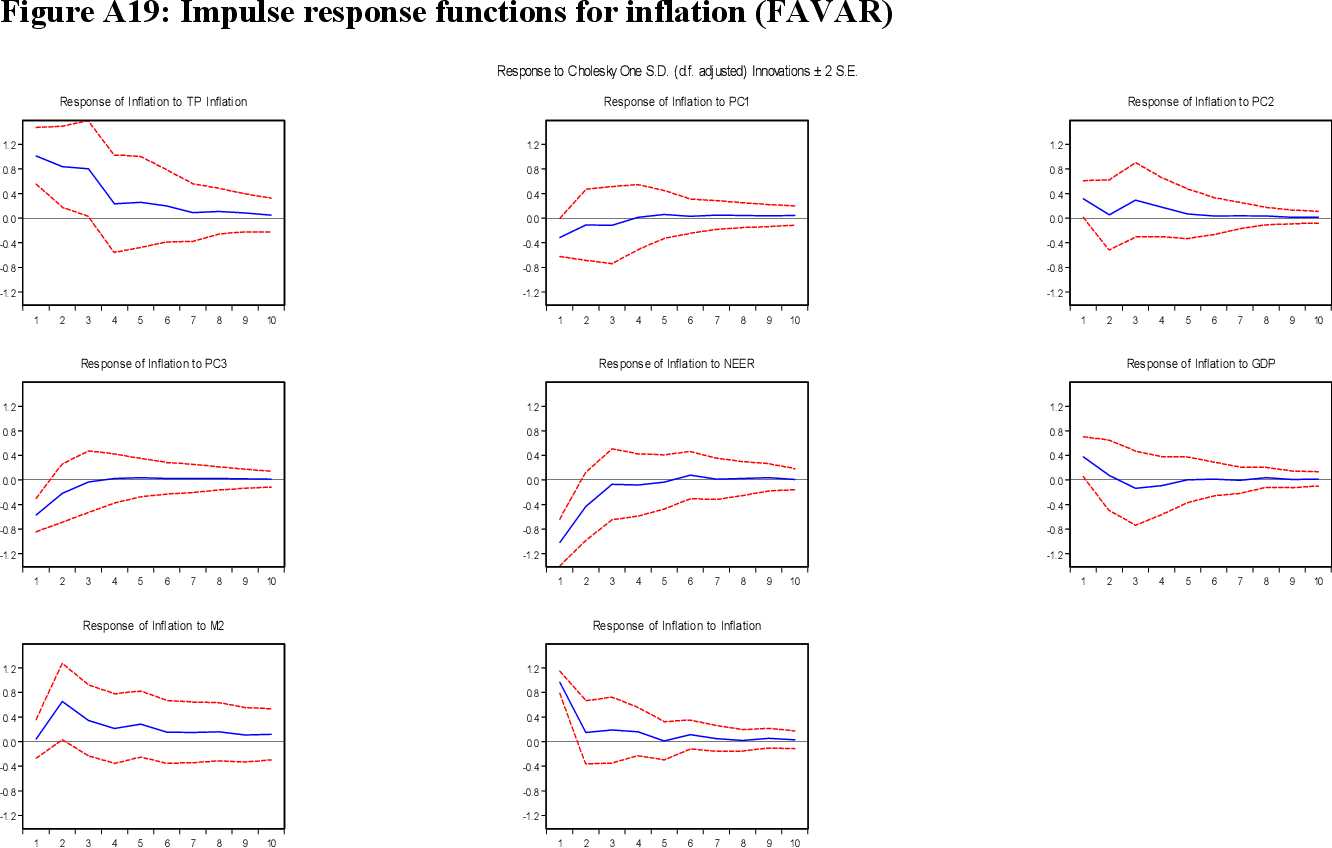

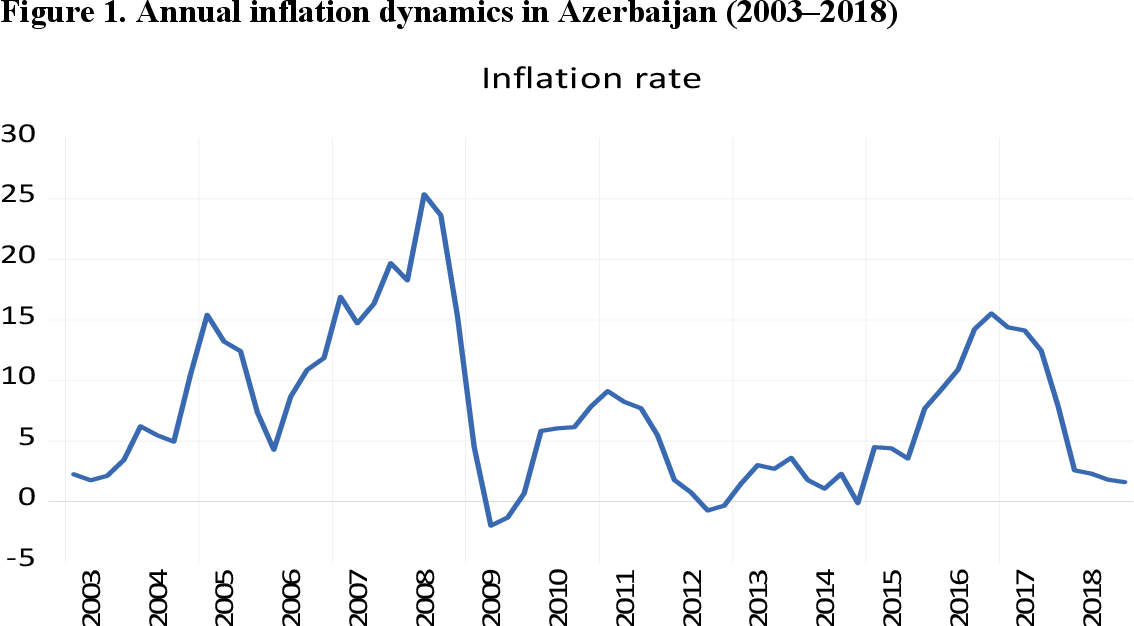

Figure A19 from Modeling Azerbaijan’s Inflation and Output Using a ...

【廣東話教學】Factor-Augmented Vector Autoregression Model (FAVAR) (With ...

A Factor-Augmented Vector Autoregressive (Favar) | PDF | Teaching ...

GitHub - lyx66/Factor-augmented-vector-autoregressive-FAVAR-WINRATS ...

Response of production and prices to an interest rate shock from VAR ...

GitHub - fawdywahyu18/TVP_FAVAR_Kalman_Filter: Estimating and ...

(PDF) Testing for the Effectiveness of Inflation Targeting in India: A ...

Table 4 from Modeling Azerbaijan’s Inflation and Output Using a Factor ...

GitHub - HoagieT/Factor-Augmented-Vector-Autoregression: An economic ...

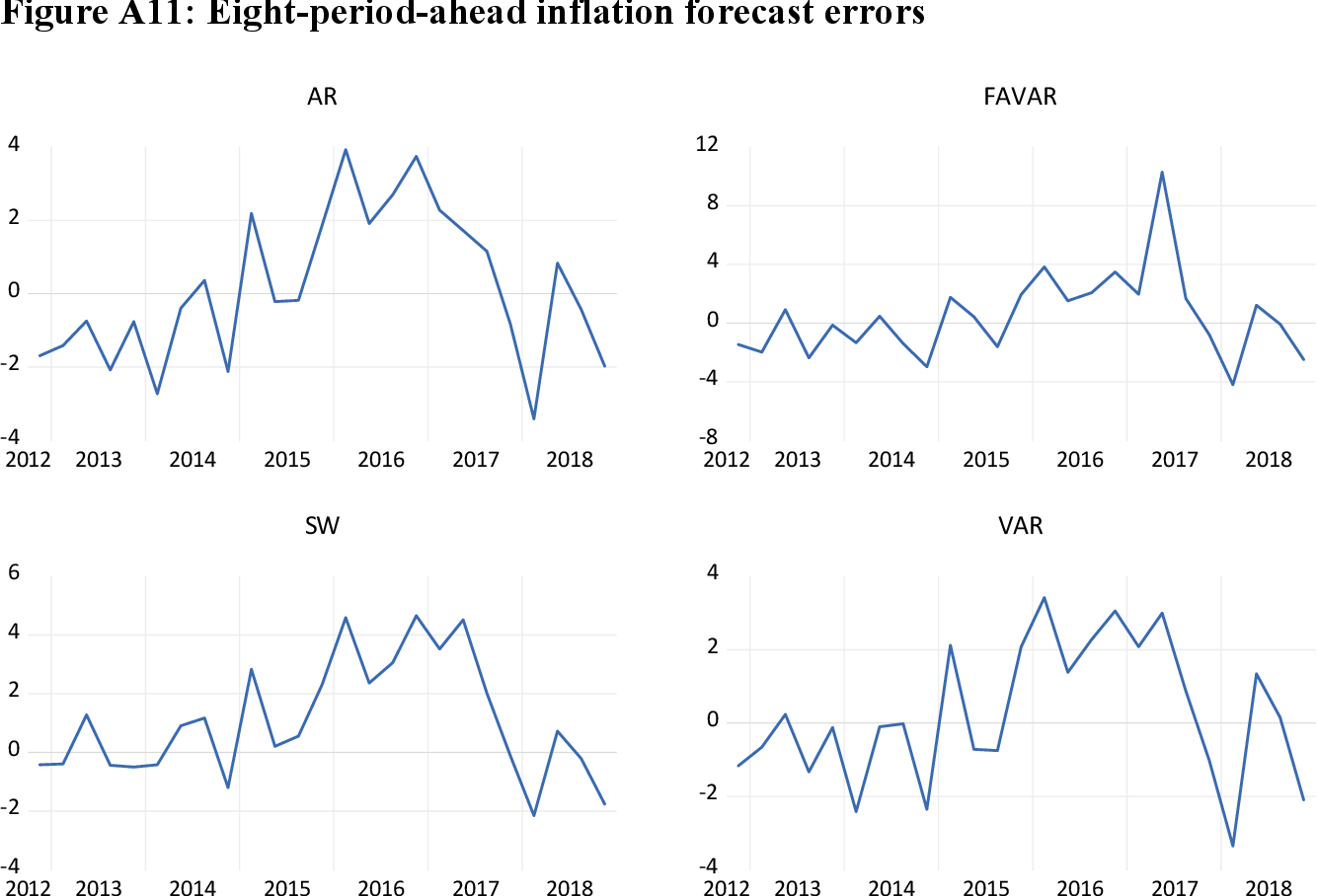

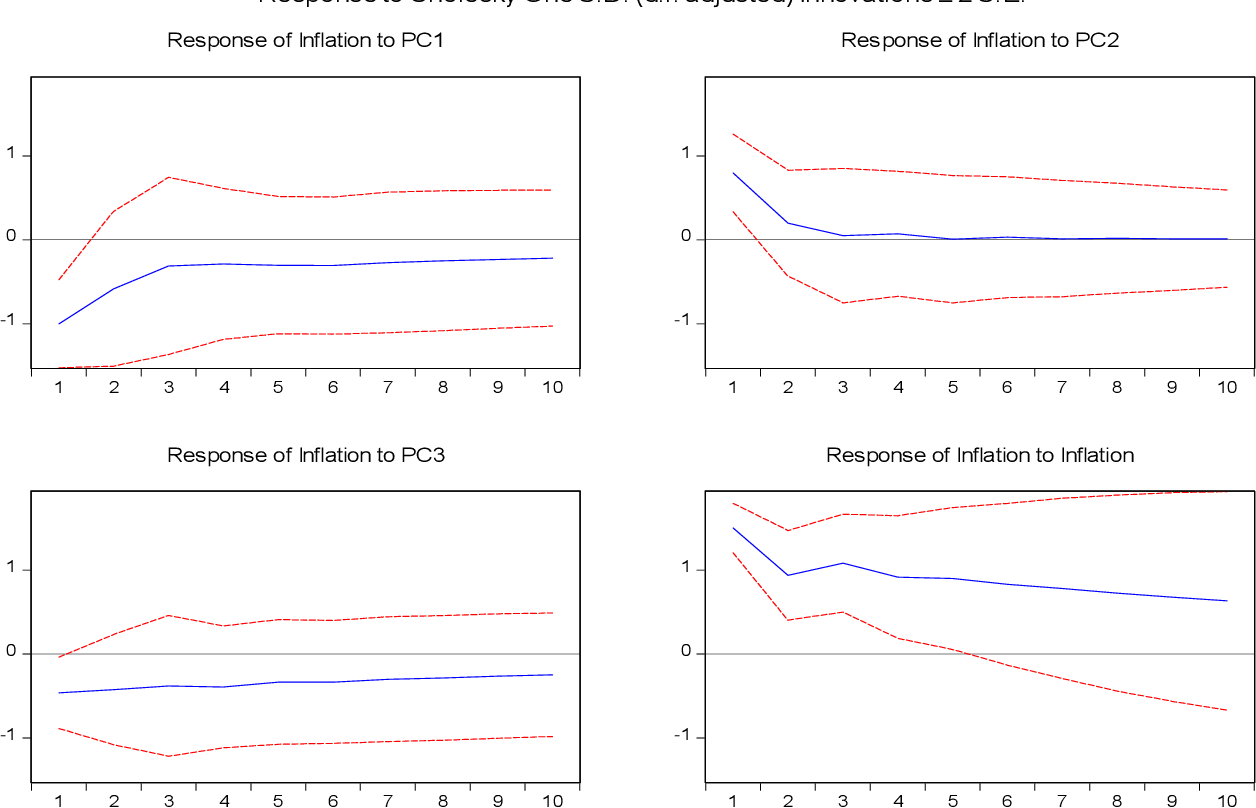

Figure A11 from Modeling Azerbaijan’s Inflation and Output Using a ...

Table 2 from Modeling Azerbaijan’s Inflation and Output Using a Factor ...

Figure A16 from Modeling Azerbaijan’s Inflation and Output Using a ...

Figure A12 from Modeling Azerbaijan’s Inflation and Output Using a ...

Impulse responses to exchange rate channel factor shock. Notes: The ...

(PDF) Regularized Estimation of High-dimensional Factor-Augmented ...

Figure A21 from Modeling Azerbaijan’s Inflation and Output Using a ...

Figure A17 from Modeling Azerbaijan’s Inflation and Output Using a ...

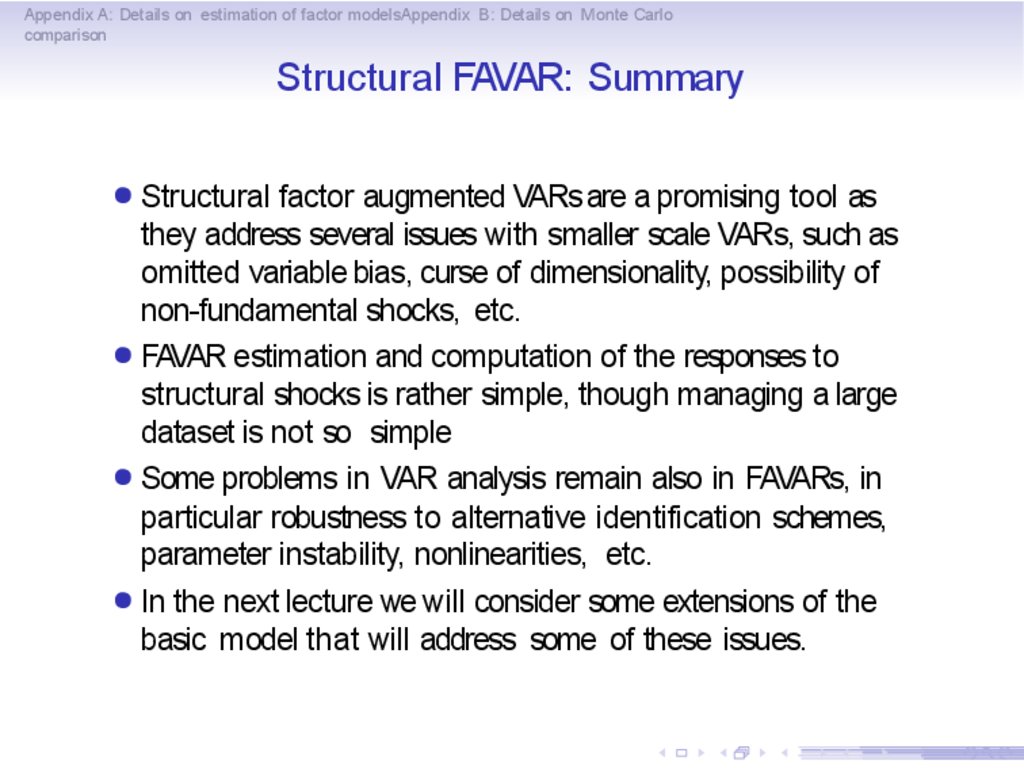

PPT - VARs and factors PowerPoint Presentation, free download - ID:375663

Figure A18 from Modeling Azerbaijan’s Inflation and Output Using a ...

(PDF) Measuring the Channels of Monetary Policy Transmission: A Factor ...

Figure 1 from Modeling Azerbaijan’s Inflation and Output Using a Factor ...

(PDF) MEASURING THE EFFECTS OF MONETARY POLICY: A FACTOR-AUGMENTED ...

(PDF) The effect of monetary policy on house price inflation: A factor ...

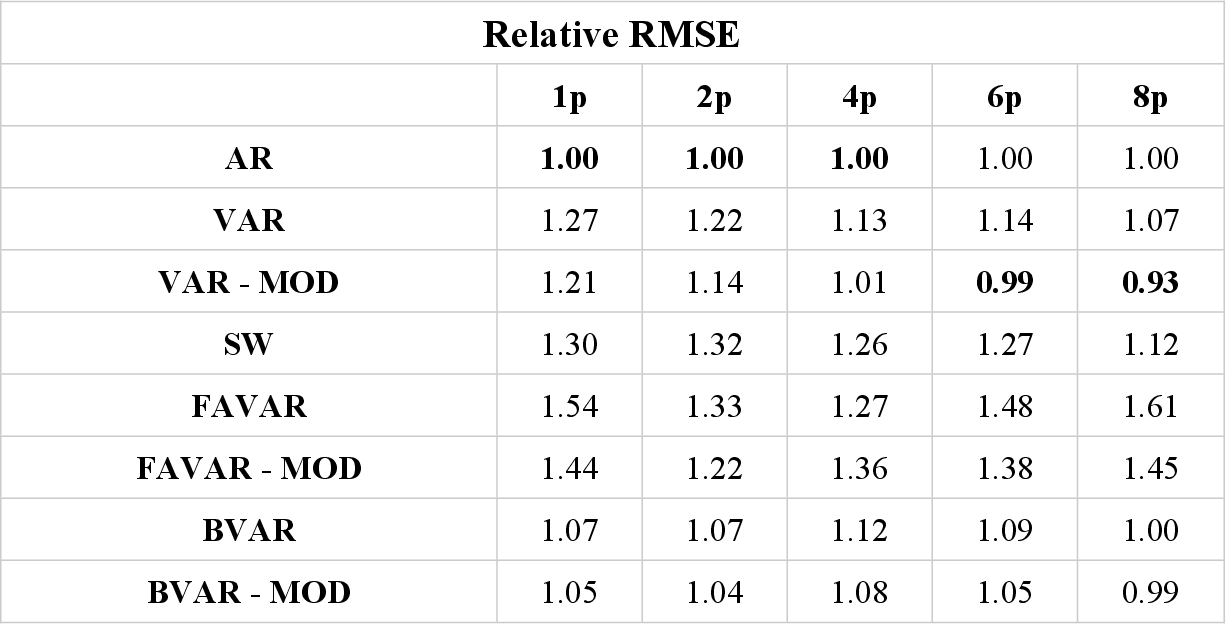

Comparisons of Mean Absolute Errors in Forecasts Produced based on the ...

Response of the credit channel variables to an interest rate shock from ...

Basics of factor models - online presentation

(PDF) Assessing the feasibility of monetary union in terms of business ...

The effect of monetary policy on housing: a factor-augmented vector ...

Impulse response functions of economic activity variables to a negative ...

Quiénes Somos

Impact of monetary policy on China’s tourism market development: An ...

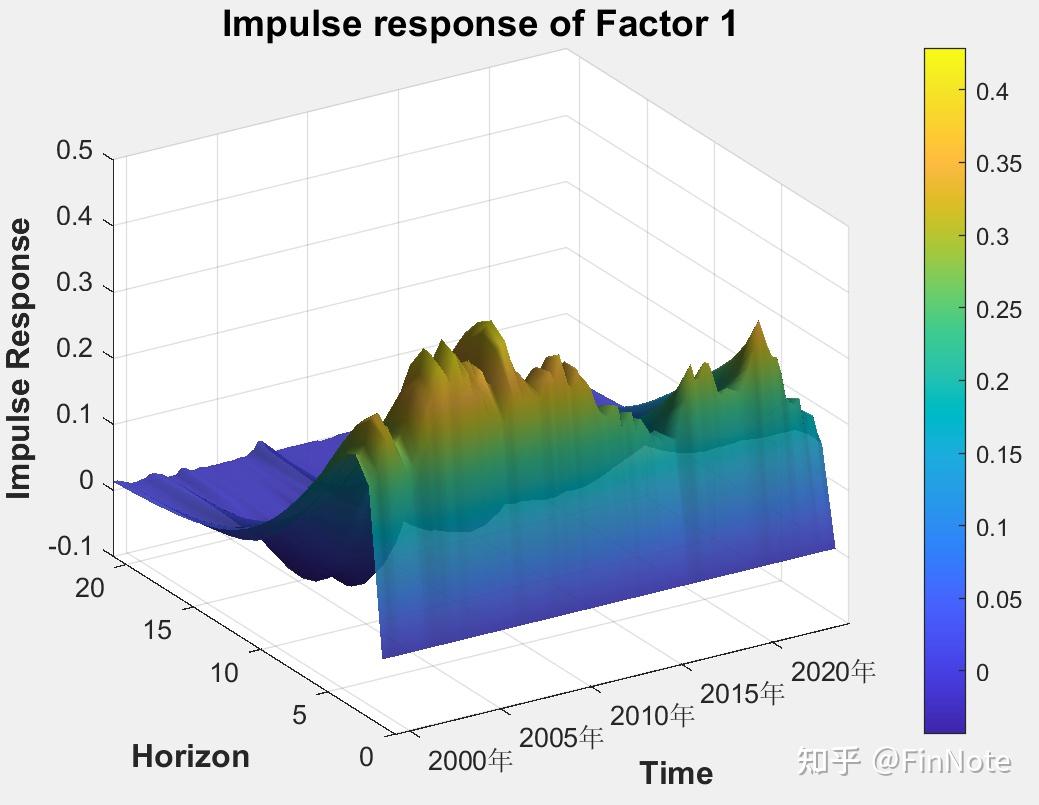

Figure B6. Impulse Responses of Common Factor Obtained from TVP-FAVAR ...

Factors 2001–2016. Note: Factors included in our FAVAR. Factors 1 and 4 ...

Favar24 - Status

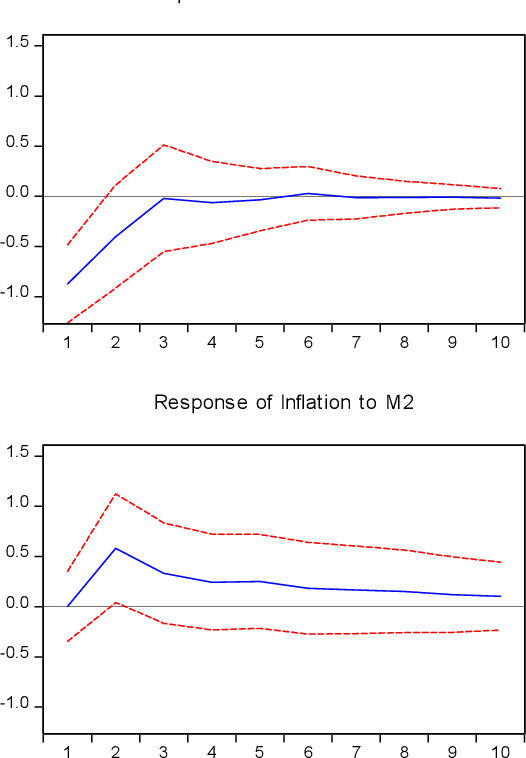

Impulse responses to a shock in M2 for the period of 1980-2017 ...

Figure B3. Impulse Responses of Common Factor Obtained from TVP-FAVAR ...

TVP-FAVAR模型原版及详细运行程序_tvp-var模型代码结果解析-CSDN博客

Time series and panel data in econometrics | PPT

Impulse responses to a shock in M2 for the period of 1980-1998 ...

【顶刊利器】TVP-SV-FAVAR模型的应用与实现 - 知乎

Impulse responses to a money supply channel factor shock. Notes: The ...

Basics of factor models

#macroeconomics #favar #uncertainty #euro_area | Carlos Cañizares Martínez

IRF of Variables to LCPI Changes in FAVAR. | Download Scientific Diagram

Linearity test: MS-FAVAR | Download Table

Impulse responses to a positive shock to the broad dollar index in the ...

Impulse responses to a shock in the base rate for the period of ...

Modelling mortality: A bayesian factor-augmented var (favar) approach ...

La tasa de cambio y sus impactos en los agregados económicos ...

中国货币政策的动态有效性研究--基于 TVP-SV-FAVAR 模型的实证分析_fvvar模型-CSDN博客

A Factor Model Analysis of the Effects of Inflation Targeting on the ...

fairmi模型,favar模型是什么-IoT知识

Estimation and analysis of fixed effects vector autoregressive models ...

GitHub - jhlinplus/High_dim_FAVAR_estimation: Regularized estimation of ...

Research on Dynamic Measurement and Early Warning of Systemic Financial ...

11.2 Vector autoregressions | Forecasting: Principles and Practice (2nd ed)

Tvp-Favar 模型精讲 – tvp-favar代码和使用方法 – OIGPY

Chapter 10 Factor-Augmented VAR | The Identification of Dynamic ...

global-commodity-cycles-and-linkages-favar-replication/Presentation ...

FRB: Finance and Economics Discussion Series: Screen Reader Version ...

Forecast error variance decompositions for 4 and 20 months -summary of ...