Showing 120 of 120on this page. Filters & sort apply to loaded results; URL updates for sharing.120 of 120 on this page

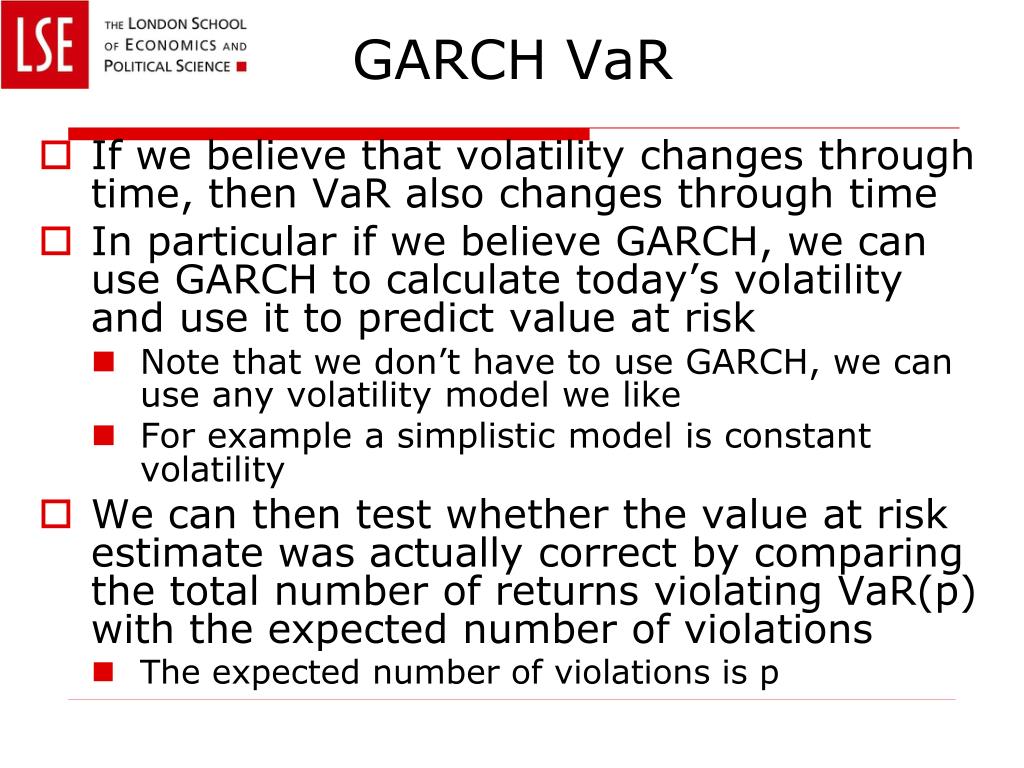

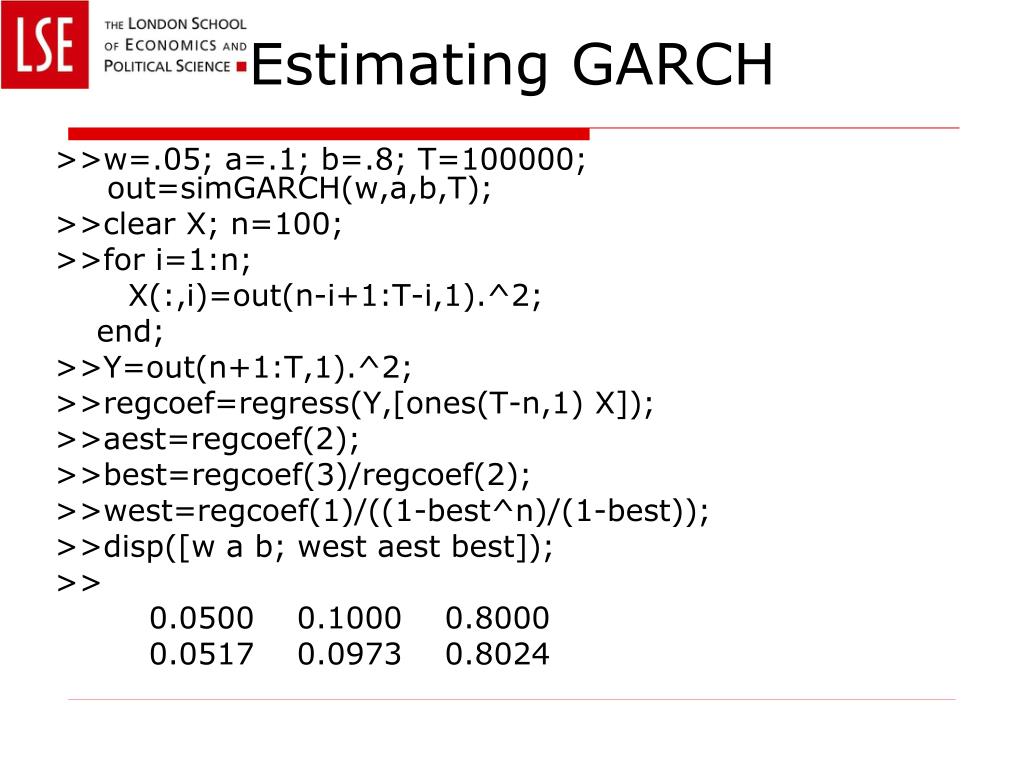

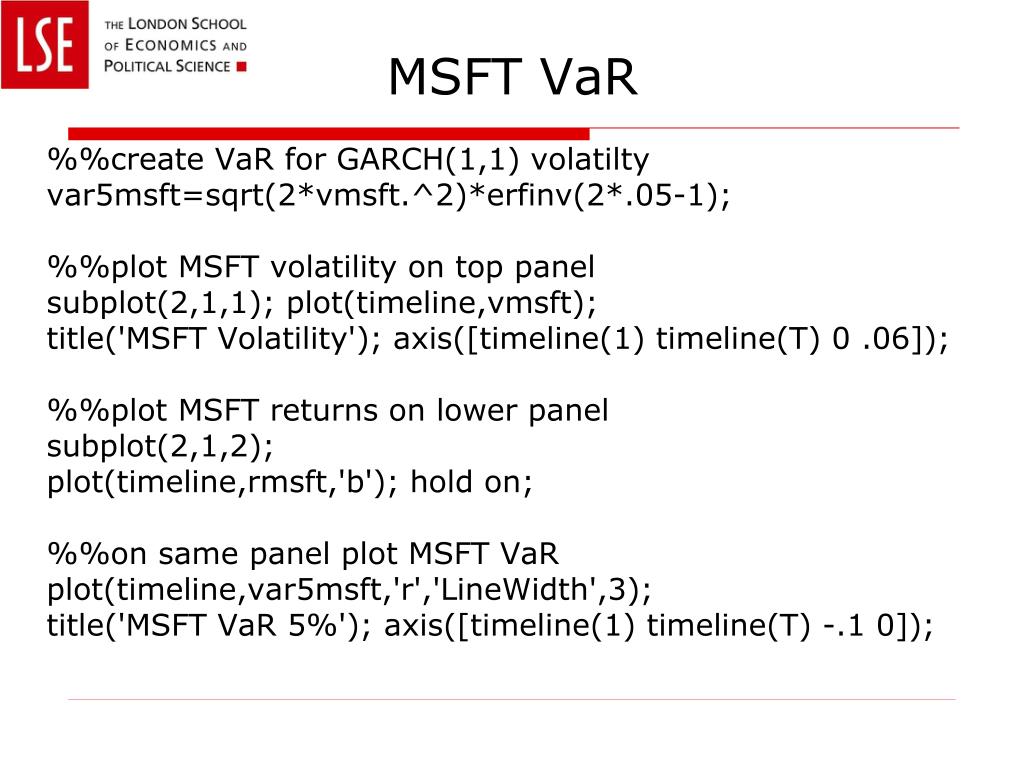

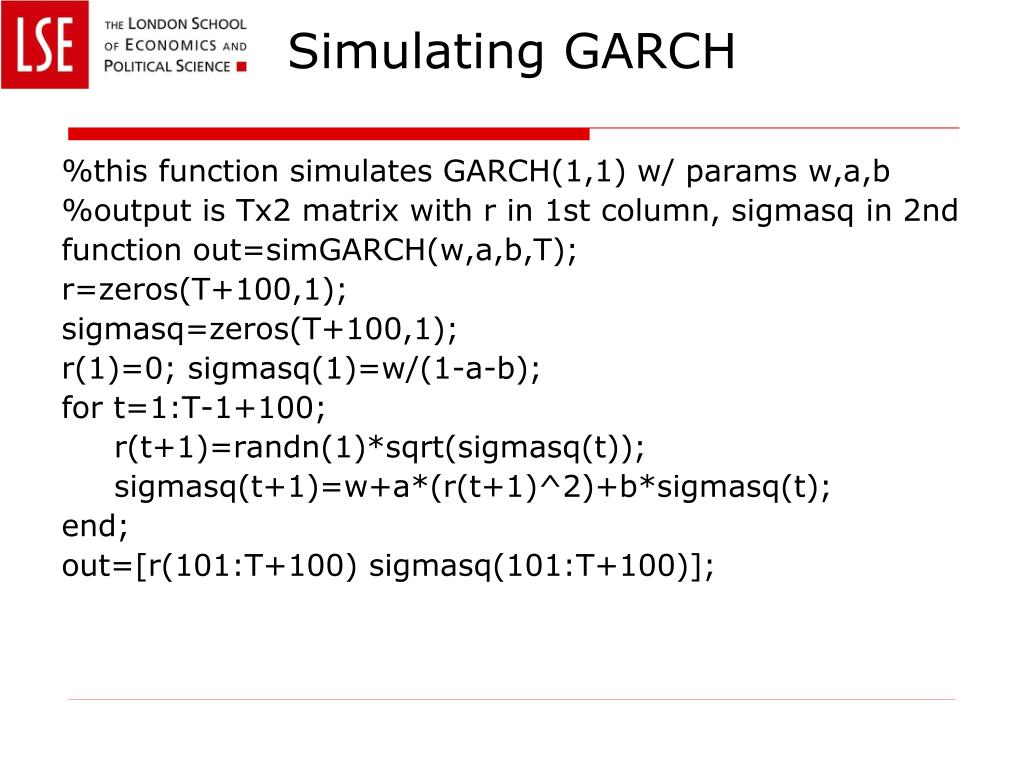

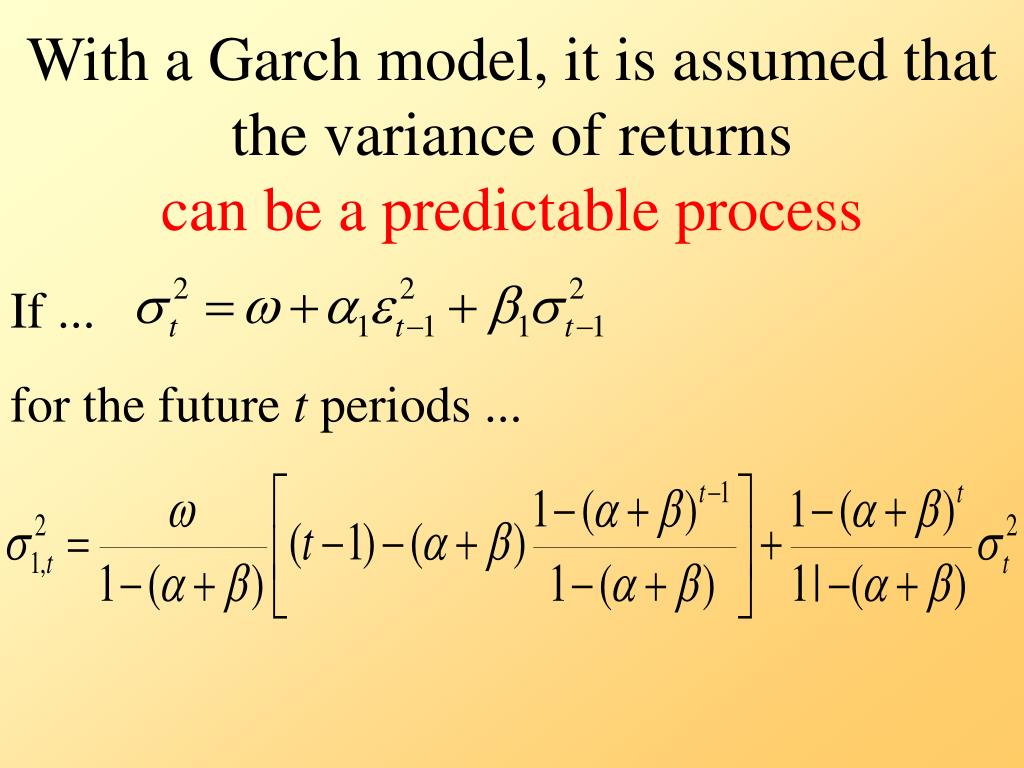

PPT - GARCH and VaR PowerPoint Presentation, free download - ID:6961496

PPT - Week 10: VaR and GARCH model PowerPoint Presentation, free ...

1-day, 1% VaR GARCH comparative graphs | Download Scientific Diagram

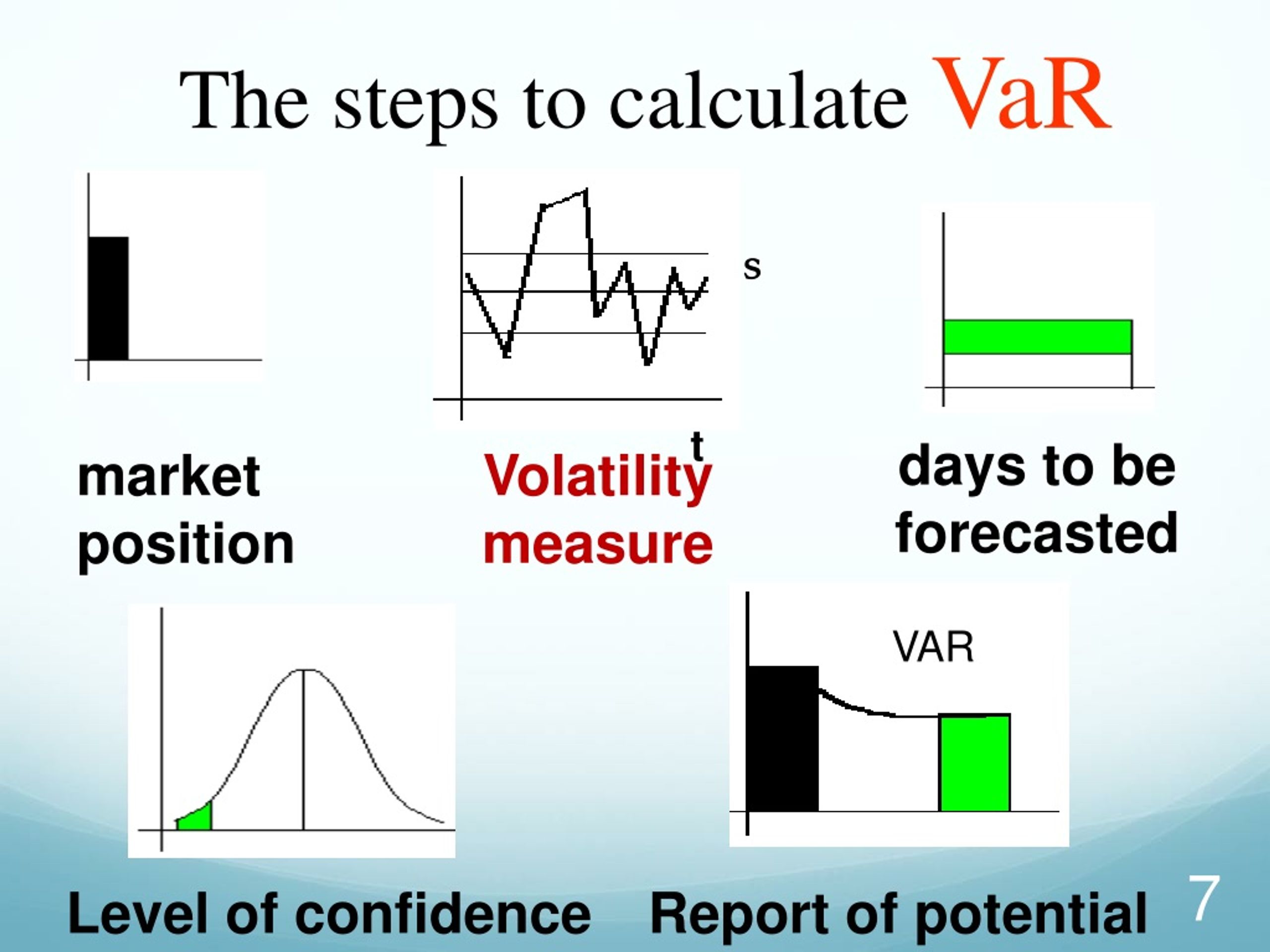

The steps for calculating the VaR by the GARCH method | Download ...

1-day, 1% VaR GARCH DCC comparative graphs | Download Scientific Diagram

Var and garch.pptx - How to use GARCH to calculate VAR 1. Estimate by ...

(PDF) A GARCH APPROACH TO VaR CALCULATION IN FINANCIAL MARKET

PPT - The Garch model and their Applications to the VaR PowerPoint ...

In-sample VaR evaluation using GARCH model | Download Table

1. Applied Econometrics VaR Modeling Using GARCH - YouTube

VaR computed using GARCH model | Download Scientific Diagram

Calcul de la VaR par le modèle GARCH #portefeuille #modèle # ...

In sample VaR for the single and regime-switching GARCH models ...

Understanding GARCH Models and VaR Calculation in Finance | Course Hero

estimation VaR by the GARCH model | Download Scientific Diagram

Figure 1 from A GARCH APPROACH TO VaR CALCULATION IN FINANCIAL MARKET ...

Unconditional coverage and CONDITIONAL coverage of VaR GARCH (1.1 ...

Comparison of VaR and CVaR series based on Normal Distribution of GARCH ...

Comparative Evaluation of Var Models: Historical Simulation, Garch ...

Figure 1 from The Use of GARCH Models in VaR Estimation | Semantic Scholar

VaR value based on the GARCH-N model. | Download Scientific Diagram

Daily VaR forecasts of GJR-GARCH models for BIST-100 index | Download ...

An Introduction to GARCH Models - YouTube

a. VAR-AGDCC GARCH Equations: Parameter Estimates for Daily Returns ...

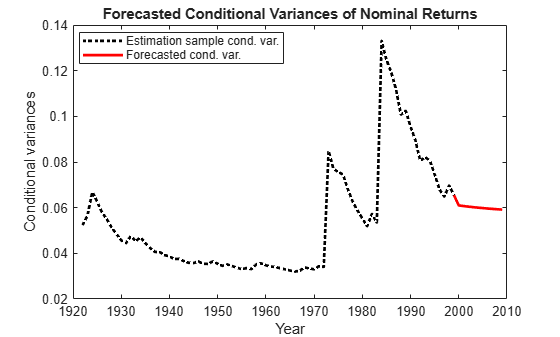

garch - GARCH conditional variance time series model - MATLAB

Schematic diagram of VaR and logarithmic returns calculated using ...

Value at Risk (VaR) Analysis: GARCH and Implied Volatility Insights ...

VaR calculado pelo GARCH(1,1) | Download Scientific Diagram

The estimated bivariate VAR DCC-GARCH-in-mean model for the Industrials ...

The estimated bivariate VAR DCC-GARCH-in-mean model for the Consumer ...

21): Backtesting VaR graph for EVT-GARCH (full line), EVT (dashed line ...

How to Model Volatility with ARCH and GARCH for Time Series Forecasting ...

GARCH conditional variance time series model - MATLAB - MathWorks India

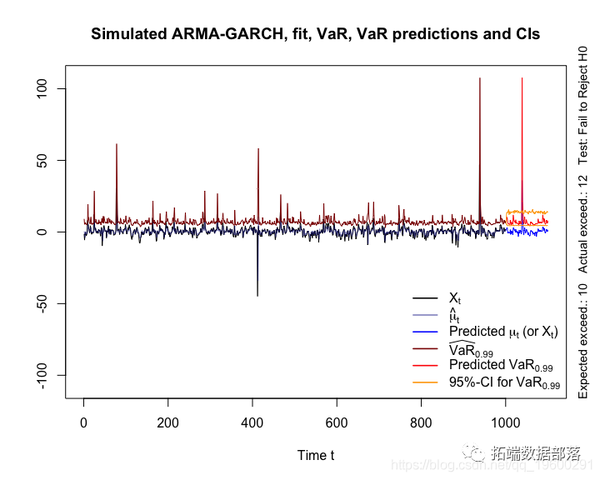

The 99% VaR (VaR0.99) for AR(1)-GARCH(1,1) model, with normal ...

Performance of VaR estimated using ARMA-GARCH model | Download ...

The estimated bivariate VAR DCC-GARCH-in-mean model for the Technology ...

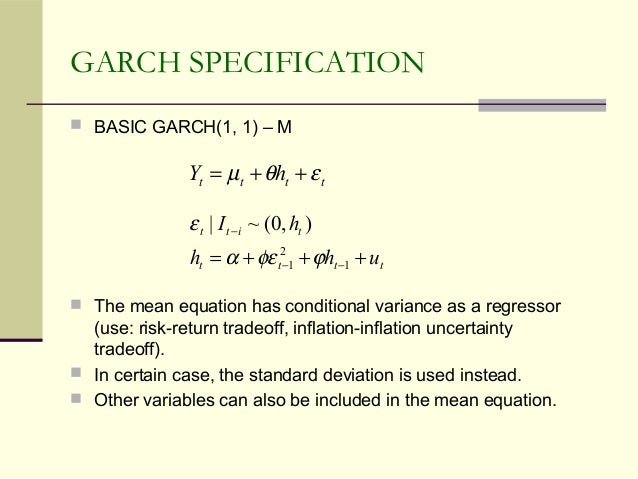

Financial econometrics xiii garch

In-sample GARCH-PIV MaxVaR to GARCH-PIV VaR ratio and GARCH-PIV ...

Comparison of VAR-GARCH model risk value and return rate at different ...

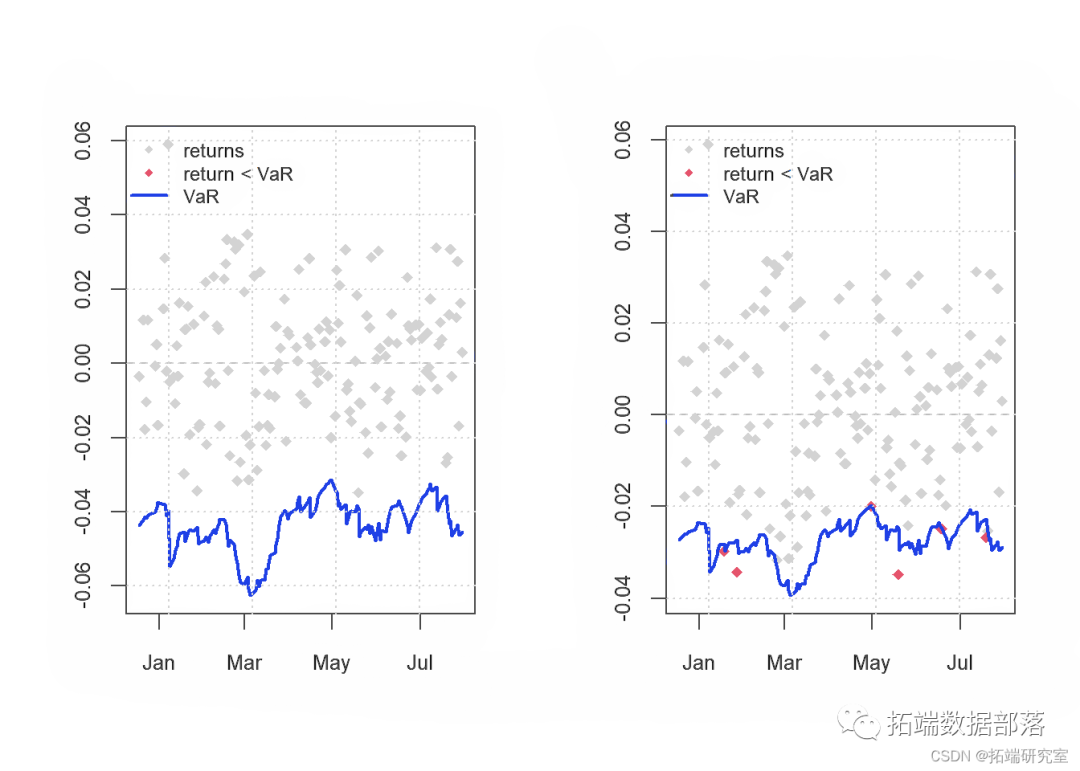

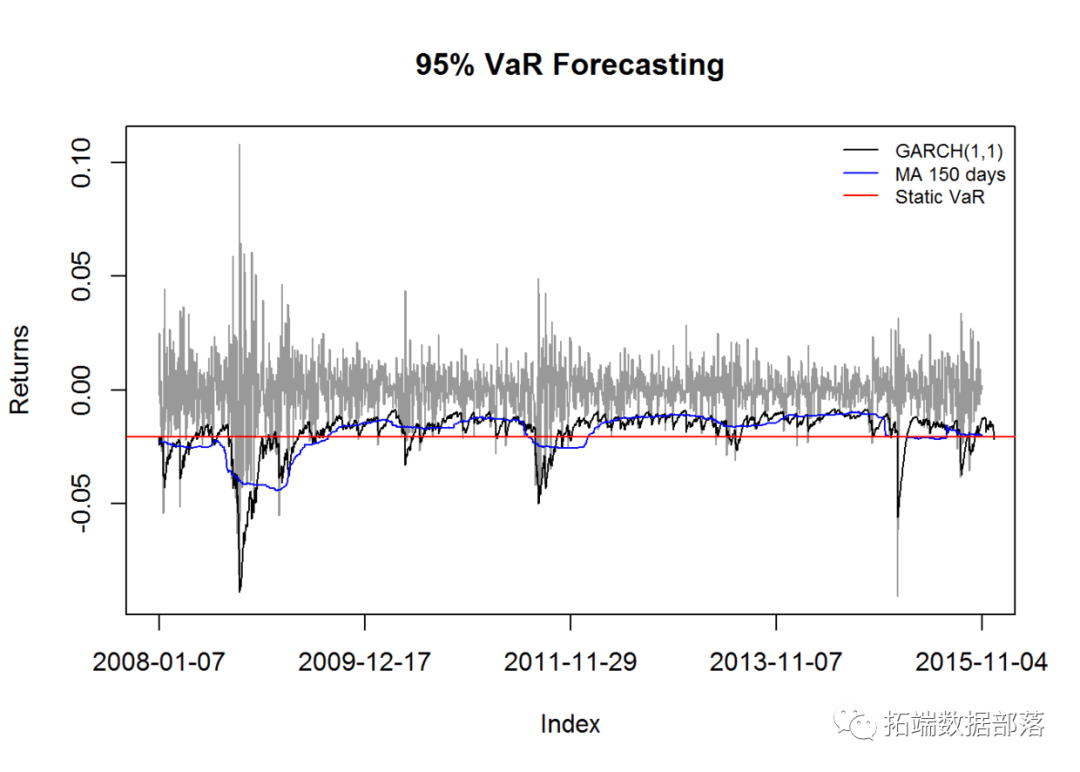

R语言用GARCH模型波动率建模和预测、回测风险价值 (VaR)分析股市收益率时间序列|附代码数据 - 知乎

An Introduction to Value at Risk Methodologies - QuantPedia

R语言用GARCH模型波动率建模和预测、回测风险价值 (VaR)分析股市收益率时间序列_garch模型怎么看预测结果-CSDN博客

a VECM-GARCH and VAR-GARCH variance coefficients for CEE and German ...

a Comparison of VECM-GARCH and VAR-GARCH variance coefficients for CEE ...

a-VAR(1) GARCH-WN b-VAR(1) Break-WN | Download Scientific Diagram

VAR-GARCH(1,1) conditional correlations between bond spreads and ...

Estimates of conditional variance VAR-DCC-GARCH model. | Download ...

Eviews7.2建立VaR-GARCH模型步骤_哔哩哔哩_bilibili

VaR-Garch模型理论与操作详解(实操)_哔哩哔哩_bilibili

garch-var模型-千图网

Estimated VAR-GARCH(1, 1) model with control variables | Download ...

Estimates of multivariate VAR-DCC-GARCH model for Bitcoin, Ethereum ...

Estimated VAR-GARCH(1,1) model | Download Scientific Diagram

VAR-BEKK-GARCH/Complete_Analysis_Revised1.R at main · prokashdeb01/VAR ...

Getting Started with garchmodels • garchmodels

PPT - ARCH/GARCH Models PowerPoint Presentation, free download - ID:8824700

Comparison of VAR-GJR-GARCH model risk value and return rate at ...

GitHub - anhdanggit/volatility-garch-VaR: Simulate and estimate ...

Estimated VAR-GARCH(1, 1) model | Download Scientific Diagram

A Hybrid Model of VAR-DCC-GARCH and Wavelet Analysis for Forecasting ...

Summary of the estimation of the VAR(1)-ECCC-GARCH(1,1) model ...

Estimated VAR-GARCH(1,1) model | Download Table

GitHub - ottodahlin/GARCH-ARCH-and-Value-at-risk-VaR-: GARCH/ARCH ...

(PDF) Application of VAR-GARCH for Modeling the Causal Relationship of ...

Estimated VAR-GARCH(1,1) Models | Download Table

R语言风险价值:ARIMA,GARCH模型滚动估计,预测VaR和回测分析股票时间序列_51CTO博客_garch模型预测var案例

VAR, GARCH-in-mean, asymmetric BEKK model | Download Scientific Diagram

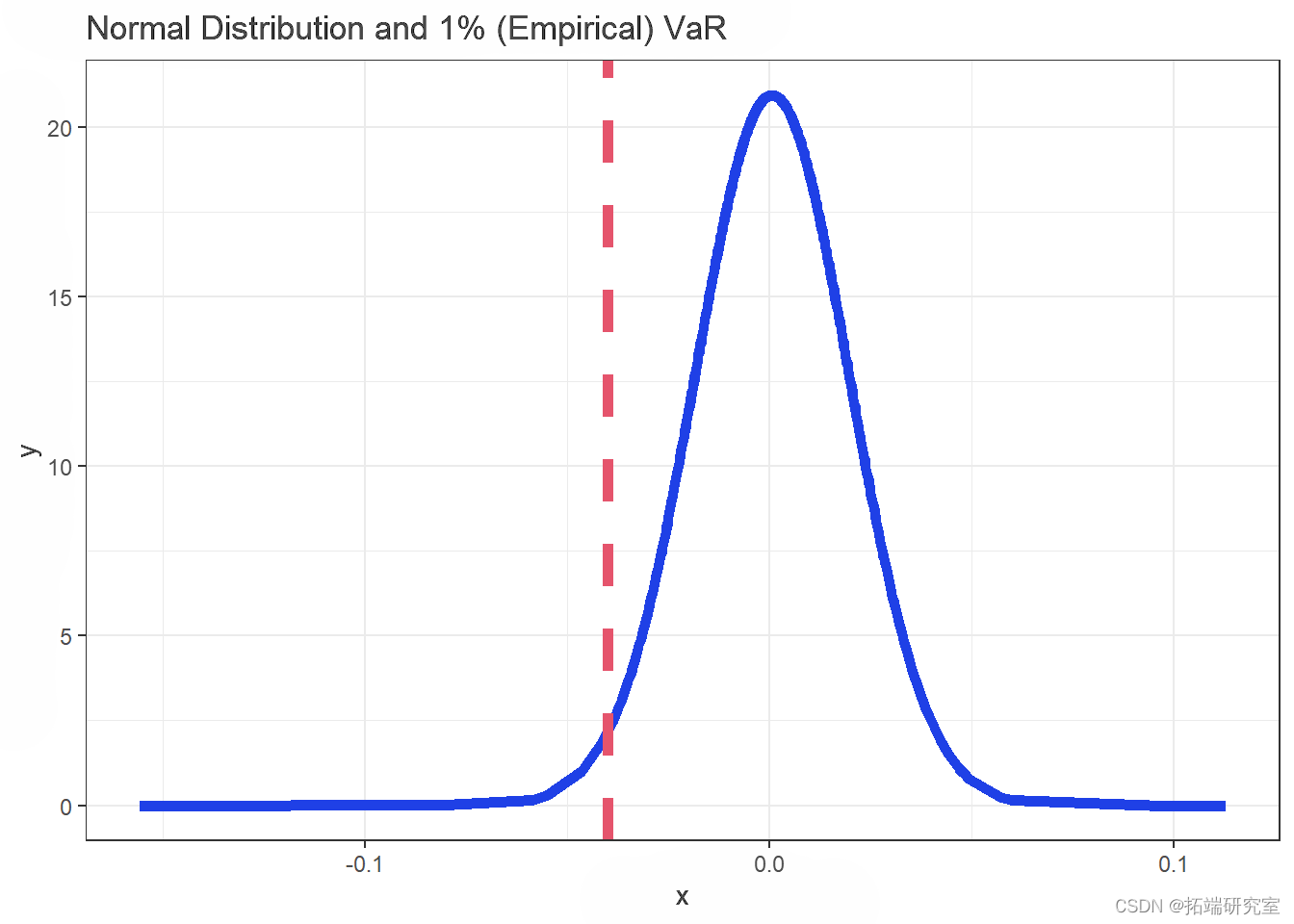

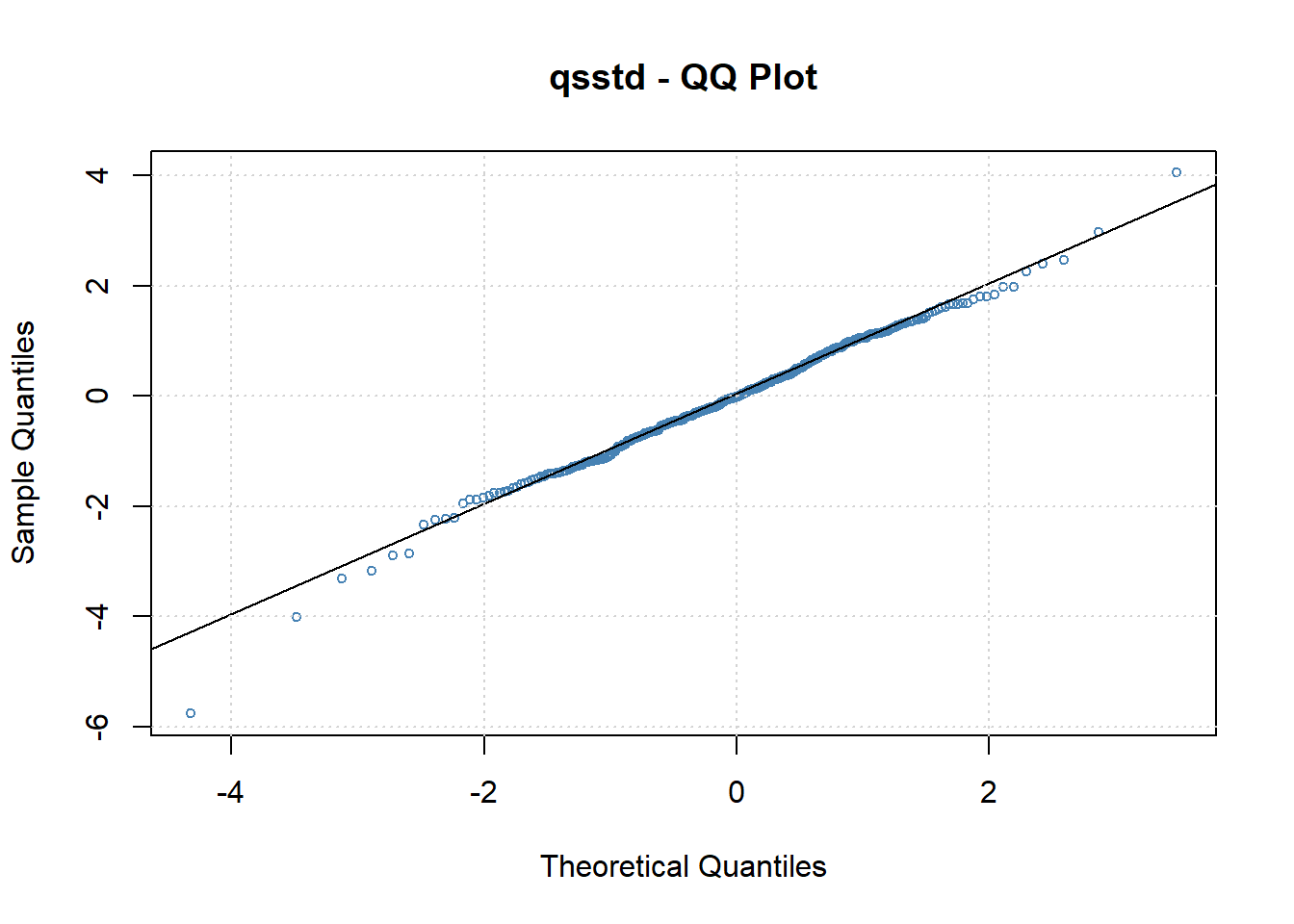

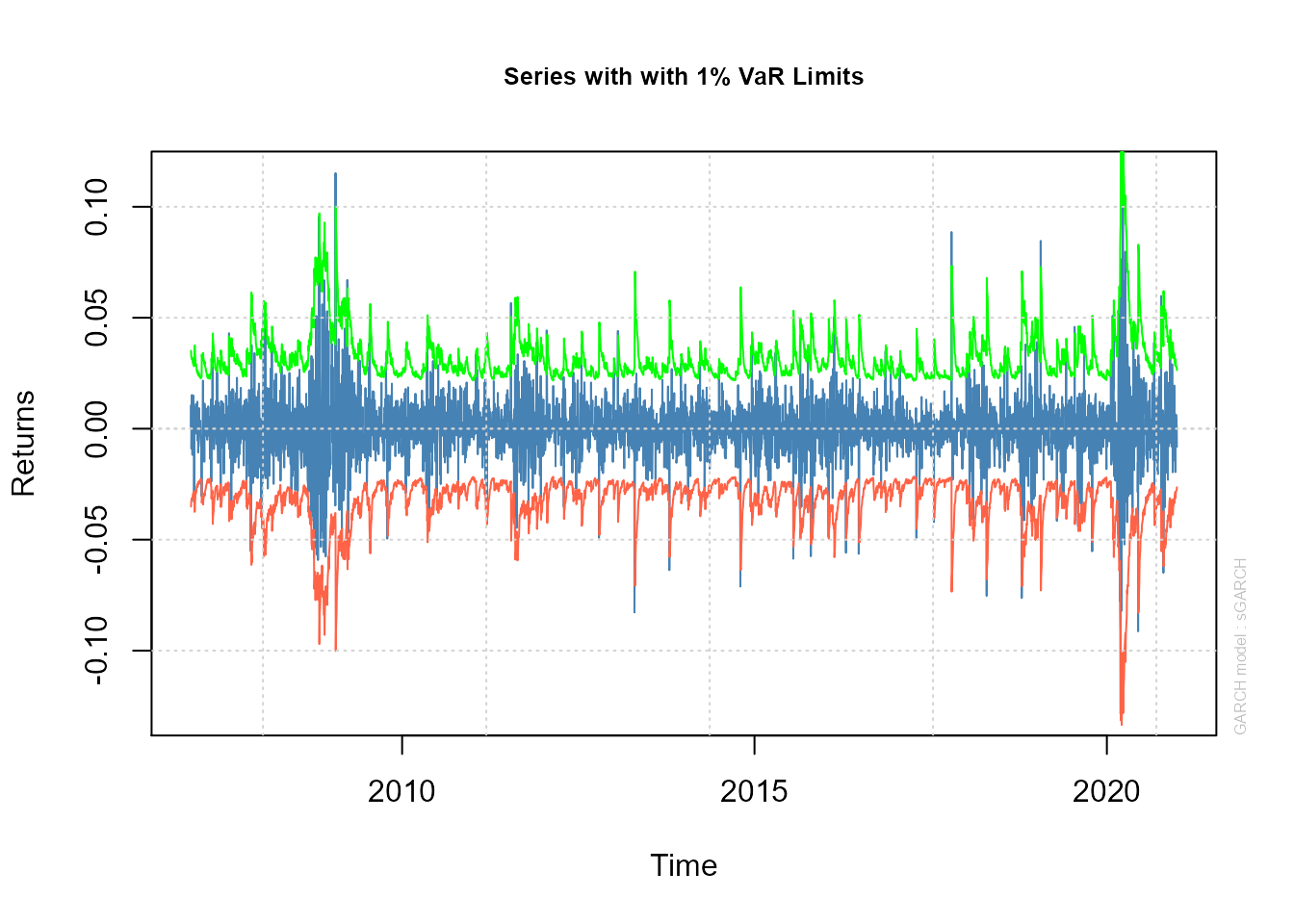

深度学习 - R语言GARCH族模型:正态分布、t、GED分布EGARCH、TGARCH的VaR分析股票指数|附代码数据 - 拓端数据 ...

PPT - Evolution of Inter and Intra-Regional Linkages to MENA Equity ...

Estimation of VAR-CCC-GARCH model | Download Table

R语言用GARCH模型波动率建模和预测、回测风险价值 (VaR)分析股市收益率时间序列...-CSDN博客

3: EURUSD forecast methods (GJR-GARCH-simulation Vs. VAR) - YouTube

ARCH/GARCH Models. - ppt download

Mastering Volatility Forecasting: A Step-by-Step Guide to Building a ...

GARCH(1,1),MA以及历史模拟法的VaR比较 - 墨天轮