Showing 120 of 120on this page. Filters & sort apply to loaded results; URL updates for sharing.120 of 120 on this page

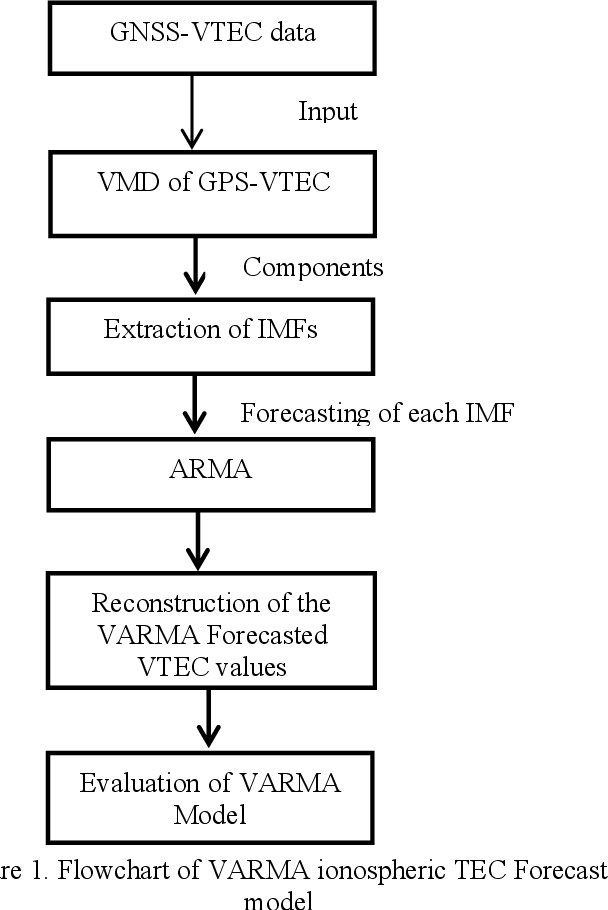

Figure 1 from Implementation of VARMA Model for Ionospheric TEC ...

| tPDC estimates for VARMA model with nonminium phase data in Example 4 ...

DeepVARMA: A Hybrid Deep Learning and VARMA Model for Chemical Industry ...

Battery Voltage Forecasting with VARMA | PDF | Autoregressive Model ...

VARMA model with Kronecker indices (2,1) and sample of 500 observations ...

VARMA model parameterization using MLLE approach for intraday wind ...

Time difference in fitting of VAR and VARMA model · Issue #6519 ...

GFESM ratio relativ to VARMA model for one-step-ahead forecasts ...

(PDF) Adjustment of a VARMA model for precipitation anomalies in ...

R : How to fit an VARMA time series model in R? - YouTube

Design an efficient VARMA LSTM GRU model for identification of deep ...

Varma Model Digital India: Varma Model Digital India

Monthly sales and corresponding forecasts with VARMA models (top ...

The best vector autoregressive moving average (VARMA) model for each ...

CCF plot for actual (transformed) and modified VARMA forecasted time ...

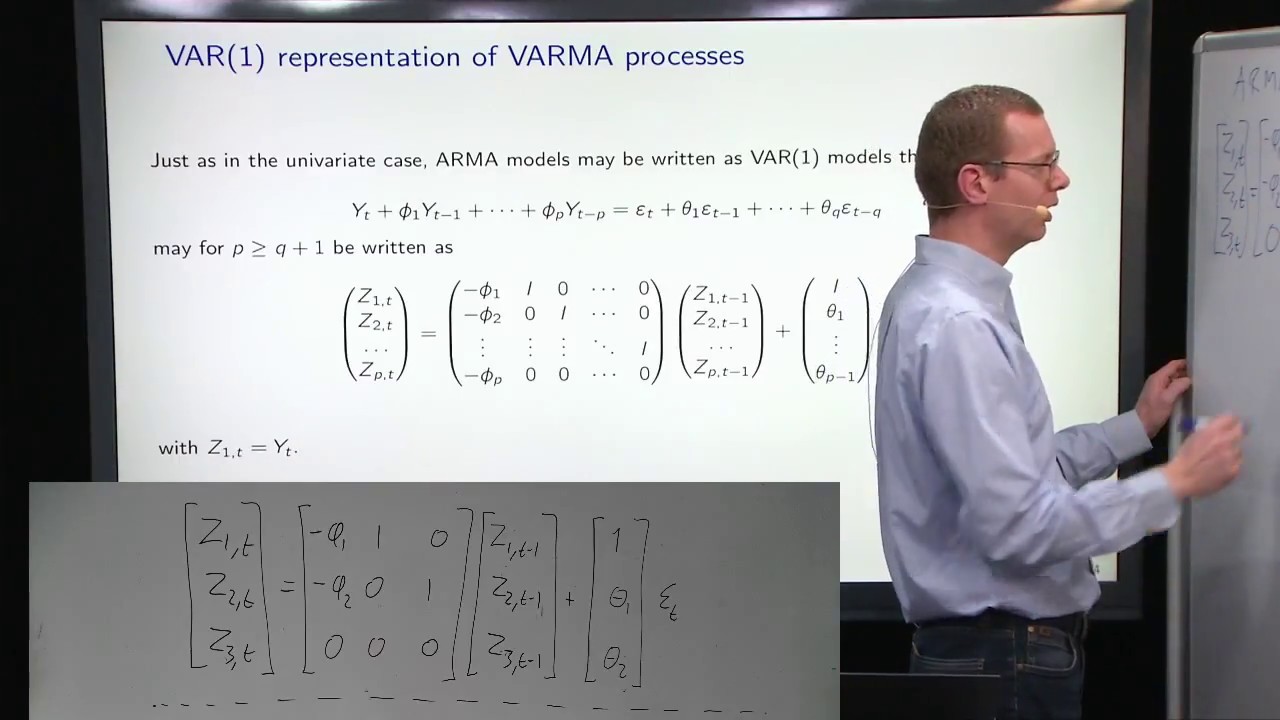

02417 Lecture 9 part D : VARMA(p,q) as VAR(1) model - YouTube

VARMA and VARMAX Models in Time Series Forecasting - YouTube

Figure 2 from Estimating structural VARMA models with uncorrelated but ...

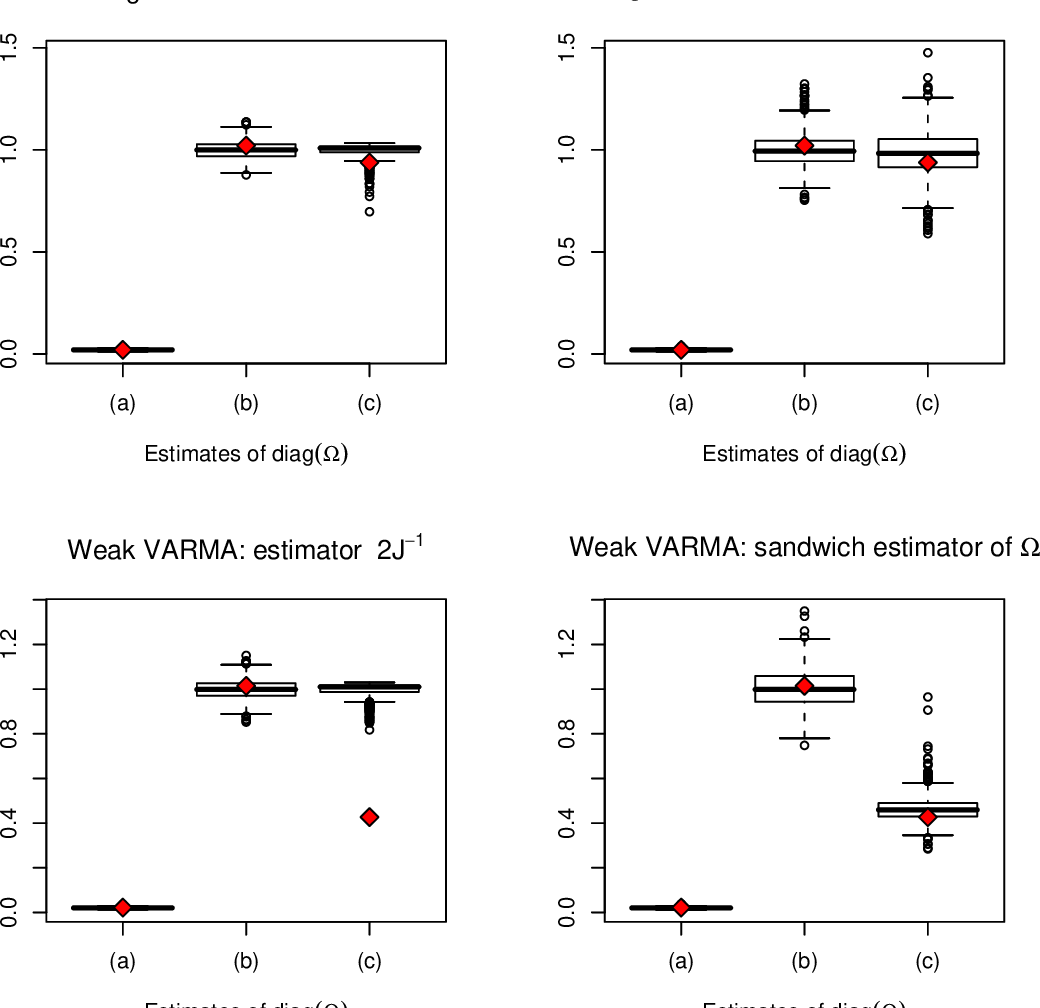

(PDF) Selection of Weak VARMA Models by Modified Akaike's Information ...

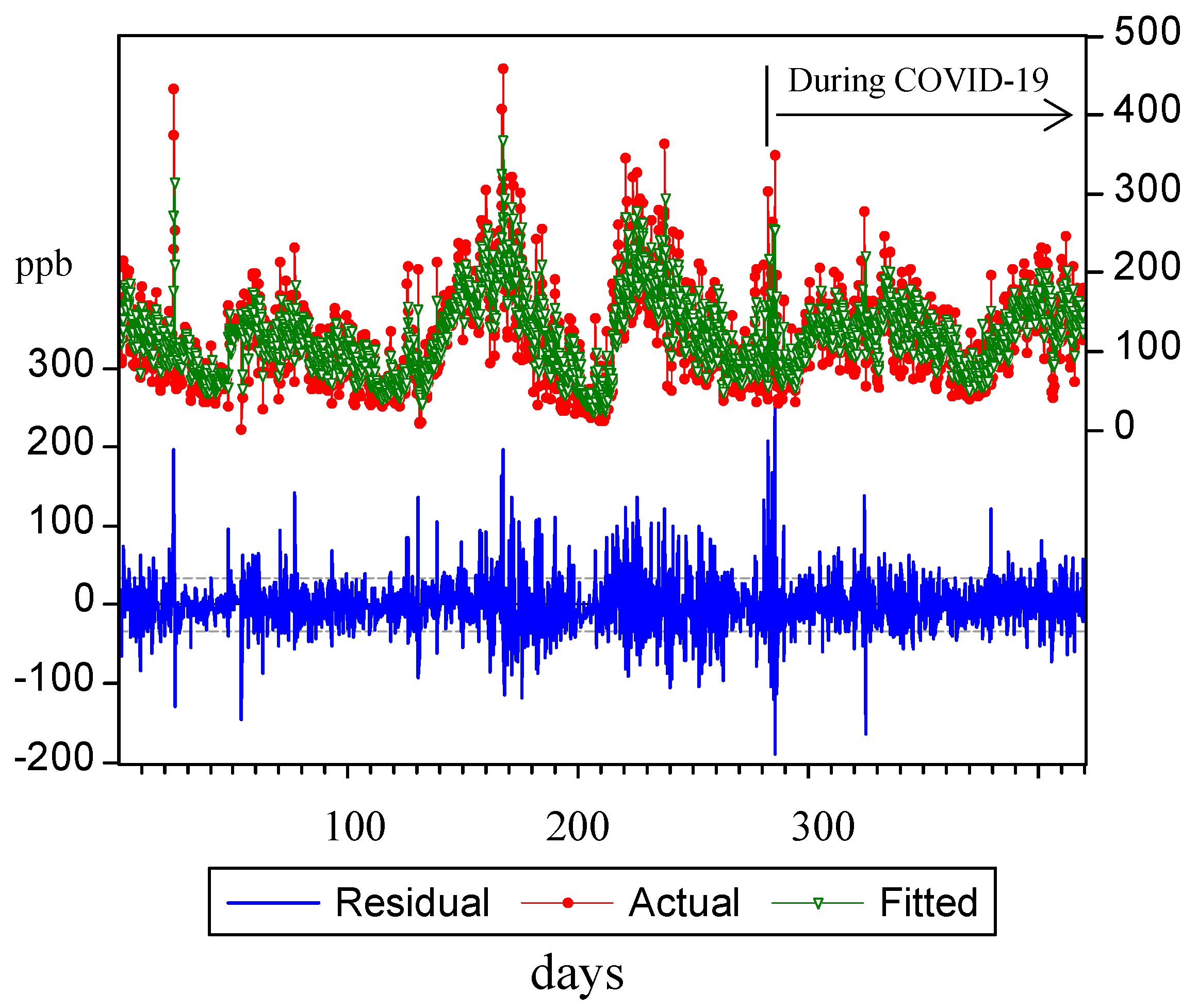

VARMA-EGARCH Model for Air-Quality Analyses and Application in Southern ...

(PDF) VARMA Models with Single- or Mixed-Frequency Data: New Conditions ...

Evaluation and test VARIMA model assumptions | Download Scientific Diagram

(PDF) The Estimators of Vector Autoregressive Moving Avarege Model ...

Dynamic factor and VARMA models: equivalent representations, dimension ...

Multivariate Time Series using VAR model | by Soubhik Khankary | Medium

(PDF) Forecasting VARMA processes: VAR models vs. subspace-based state ...

Graph showing the p-values of the Durbin-Watson test for the VARMA ...

Figure 1 from FACTOR DECOMPOSITION OF VARMA MODELS BASED ON WEIGHTED ...

Estimates of coefficients of optimal VARMA (0, 1) models. | Download ...

Identification and estimation of Structural VARMA models using higher ...

(PDF) The Use of Varma Models in Forecasting Macroeconomic Indicators

SOLUTION: Weighted covariance factor decomposition of varma models ...

(PDF) Forecasting VARMA processes using VAR models and subspace-based ...

(PDF) For Estimating Varma Models with a Macroeconomic Application

(PDF) Estimating structural VARMA models with uncorrelated but non ...

(PDF) Maximum Likelihood Estimation of VARMA Models Using a State-Space ...

Fit model using VARMA-X model | Download Table

VARMA Models for Macroeconomic Forecasting | PDF | Vector ...

Stochastic Volatility of TVP-VARMA Model Source: Research finding ...

In brief: Vijay Varma models John Jacobs; CFDA, Genesis promote Asian ...

(PDF) Switching VARMA term structure models

(PDF) VARMA models for Malaysian Monetary Policy Analysis

(PDF) Estimation of Causal Invertible VARMA Models

Figure 1 from Estimating structural VARMA models with uncorrelated but ...

ComparisonARIMA-X model and VARMA-X model | Download Table

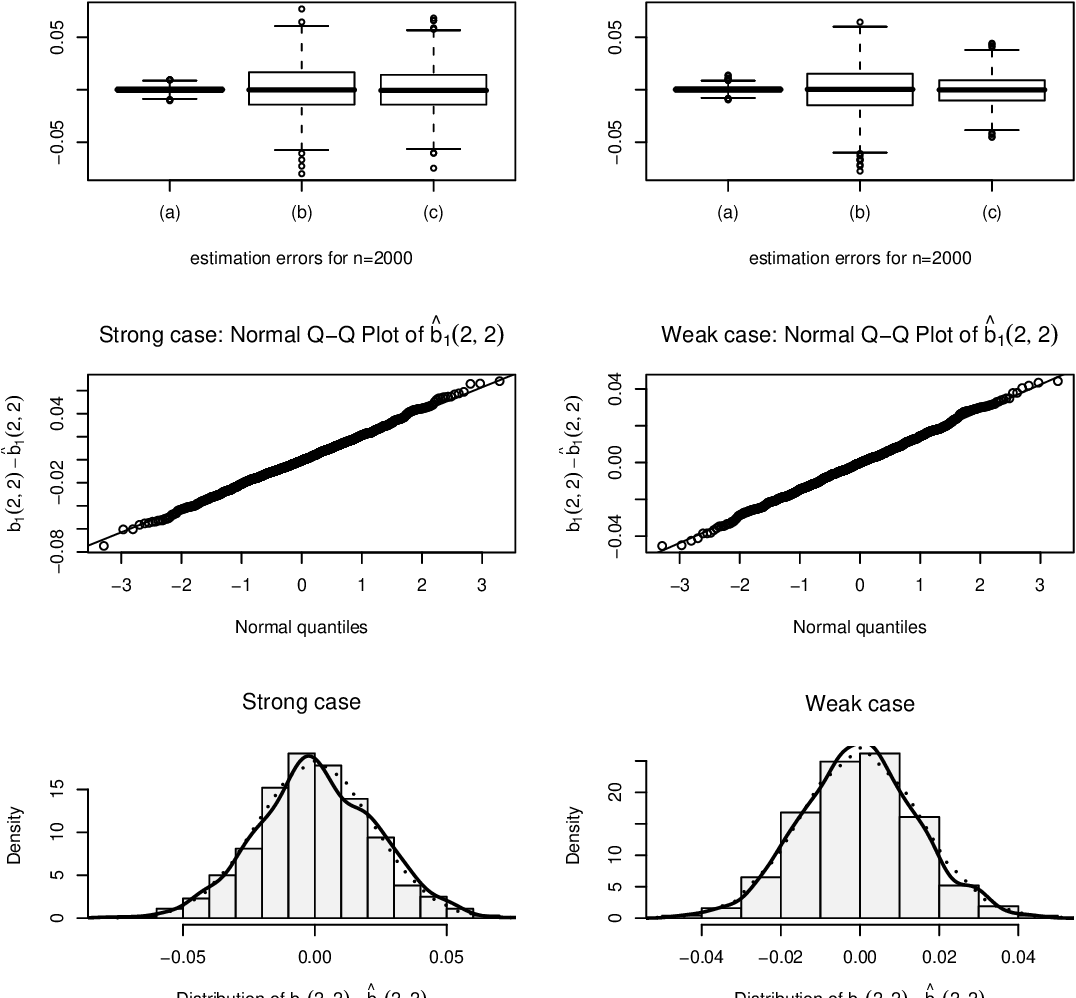

(PDF) Center-Outward R-Estimation for Semiparametric VARMA Models

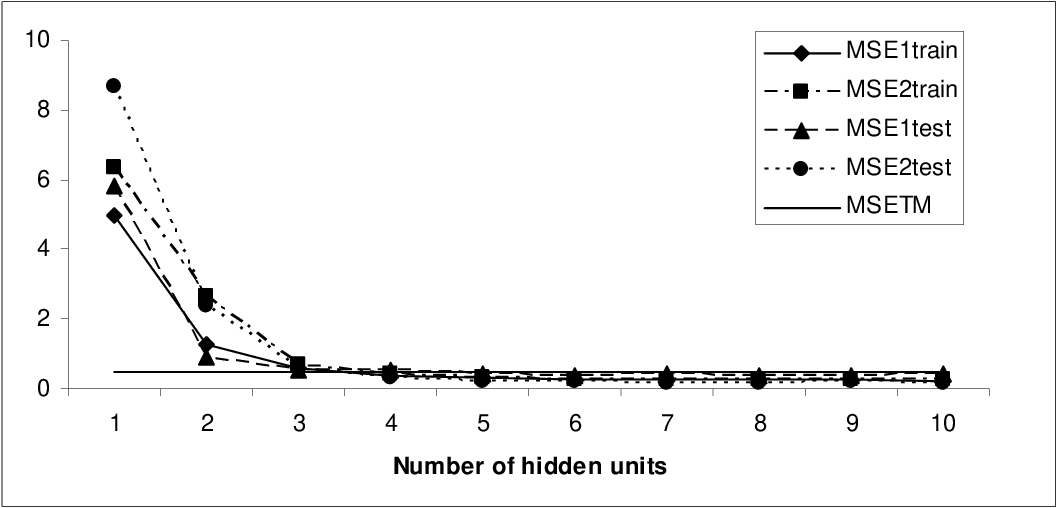

Figure 2 from Forecasting Performance of VAR-NN and VARMA Models ...

A Guide to VARMA with Grid Search in Time-Series Modelling

(PDF) Testing for A Set of Linear Restrictions in VARMA Models Using ...

(PDF) Measuring the Effects of Malaysian Monetary Policy : VARMA vs VAR ...

(PDF) Forecasting Time Series with VARMA Recursions on Graphs

PB counts for |M S F E| for canonical SCM VARMA models versus canonical ...

(PDF) The exact Gaussian likelihood estimation of time-dependent VARMA ...

(PDF) Fiscal and Monetary Policy Interaction in Iran: A TVP-VARMA Model

(PDF) Identification of outliers in time series with VARMA models using ...

Multivariate time series forecasting using VAR, VARMA and VARMA with ...

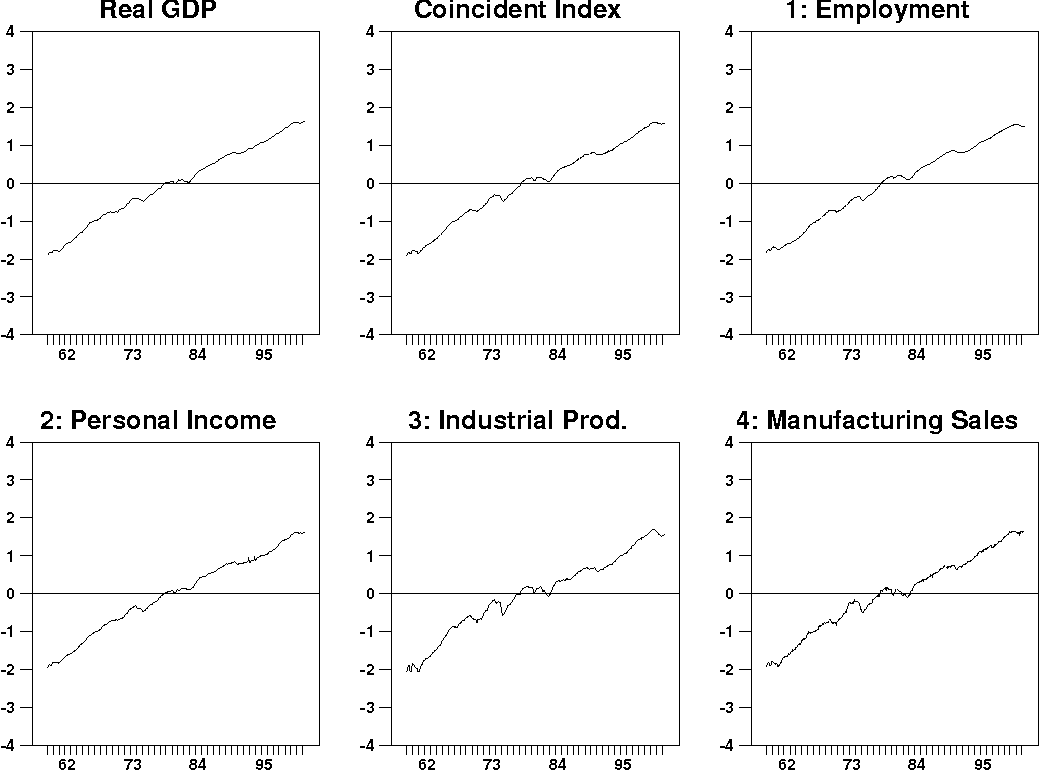

Table 1 from Business cycle analysis and VARMA models | Semantic Scholar

Port of Gijón. Results of the VARMA models using variables SO 2 , NO ...

Coefficients and their standard errors of a VARMA(5, 0) model fitted on ...

Understanding Varma Vector Autoregressive Moving Average Models

PB counts for tr(M S F E) for canonical SCM VARMA models versus ...

Figure 1 from Graphical models for structural VARMA representations ...

Figure 11 from Forecasting Time Series With VARMA Recursions on Graphs ...

Figure 4 from FACTOR DECOMPOSITION OF VARMA MODELS BASED ON WEIGHTED ...

Figure 2 from Forecasting Time Series With VARMA Recursions on Graphs ...

Customizing your models with data with Paroma Varma - YouTube

Mô hình VMA và VARMA tổng quát - Vietlod

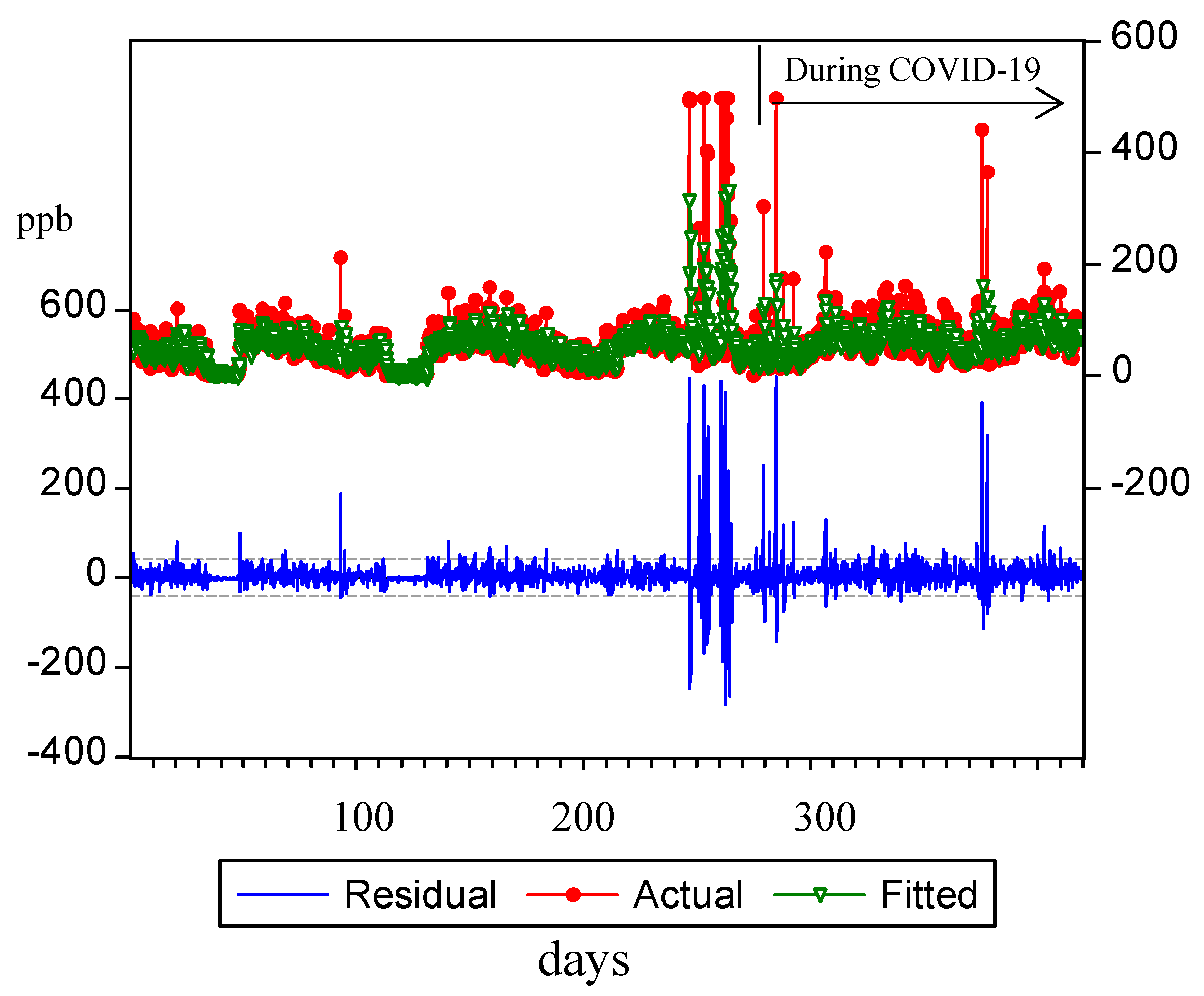

EWMA Control Chart Integrated with Time Series Models for COVID-19 ...

GAUSS varmaPredict Example | Aptech

| tPDC estimates by all four methods-VAR, VMA, VARMA, and WN-for the ...

GitHub - WolfgangScherrer/VARMA-modeling: Supplementary material for ...

(PDF) Comparative Performance of Vector Autoregressive (VAR) and Vector ...

VARMA-GARCH and VARMA-AGARCH models for Brent | Download Table

VARMA(Vector Auto Regressive Moving Average) in Time Series Modelling ...

Estimation of parameters of А1 matrix of a VARMA-model (1, 1 ...

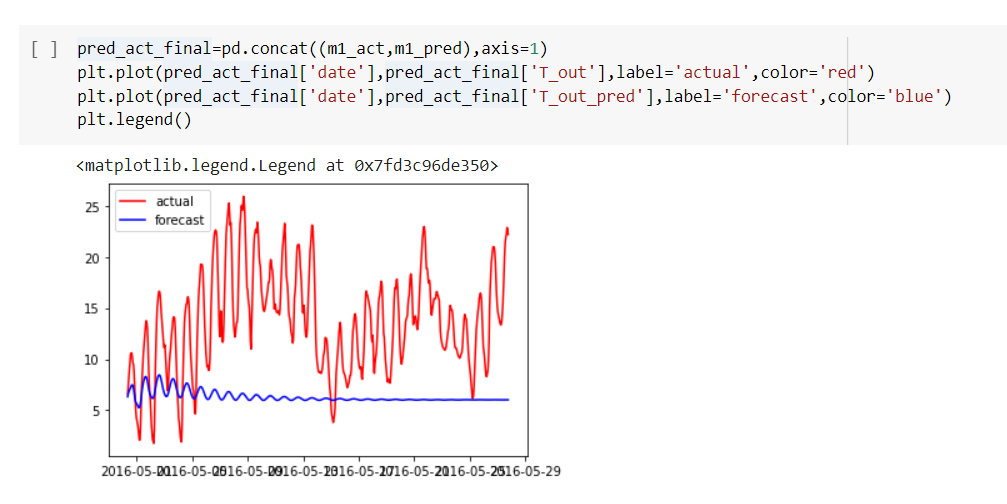

Step-by-Step Guide to Multivariate Time Series Forecasting with VAR ...

Chapter 17: Multivariate VARMA-GARCH Models - Multiple Time Series ...

Proposed VARMA‐based WPF methodology. | Download Scientific Diagram

(PDF) A program for computing the exact fisher information matrix of a ...

(PDF) A new diagnostic tool for VARMA( p , q ) models

Robustness of out-of-sample results with respect to the order ...

Estimation results of the parameters of the VECM-DCC-VARMA- AGARCH ...

Figure 2 from Simple Identification and Specification of Cointegrated ...

(PDF) Modified Schwarz and Hannan–Quinn information criteria for weak ...

Figure 3 from Simple Identification and Specification of Cointegrated ...

Figure 1 from The exact Gaussian likelihood estimation of time ...

estimation - Are consecutive zeros across multiple dimensions in ...

Table 1 from The exact Gaussian likelihood estimation of time-dependent ...

(PDF) Estimating the Kronecker Indices of Cointegrated Echelon‐form ...

Variational Analysis and Reliability Modeling Algorithms (VARMA) | VIP ...

Statistics: Multivariate time series analysis — fundamental concepts ...

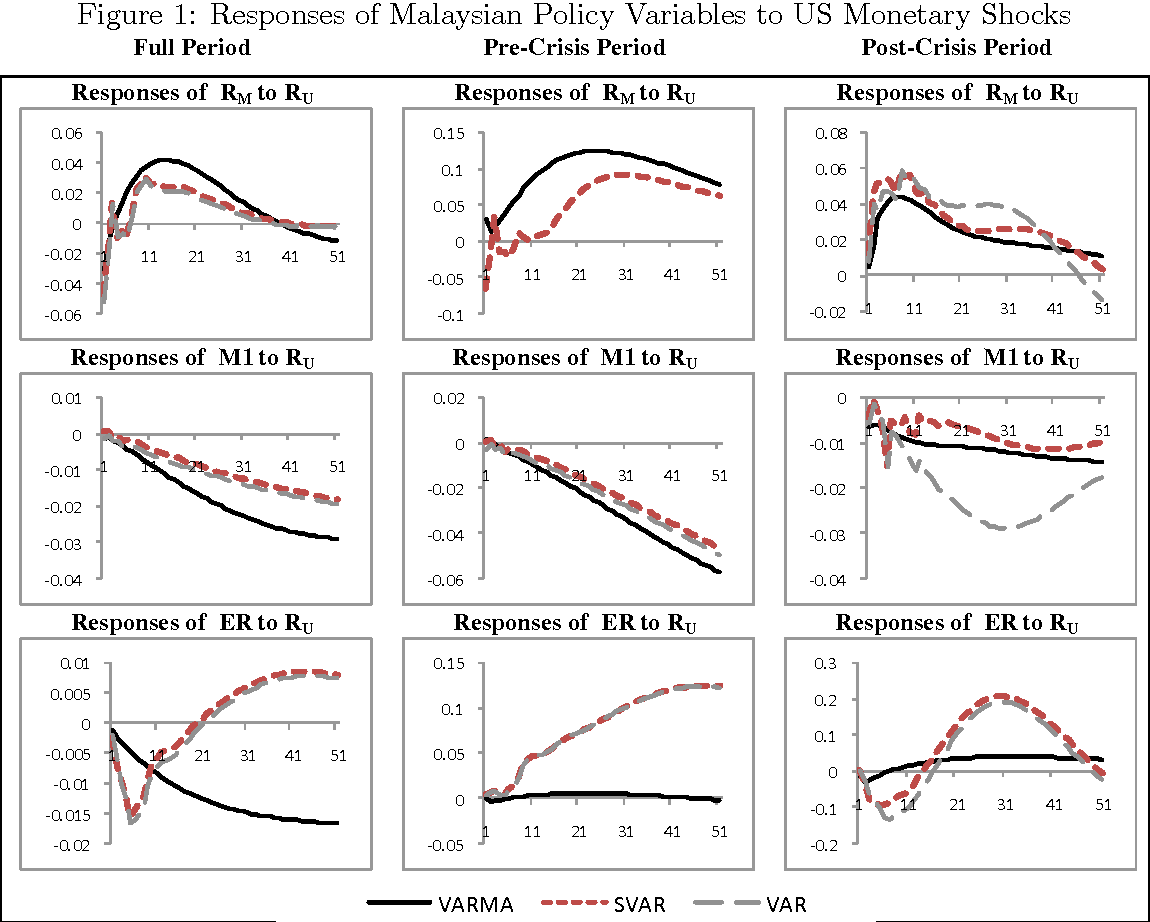

Figure 1 from Measuring the Effects of Malaysian Monetary Policy ...