Showing 120 of 120on this page. Filters & sort apply to loaded results; URL updates for sharing.120 of 120 on this page

The Yang and Zhang Volatility Estimation Model | by Gilbert Teklevchiev ...

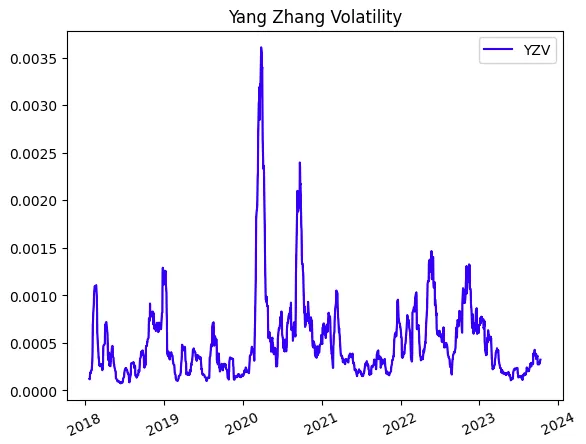

Yang Zhang Volatility - QuantConnect.com

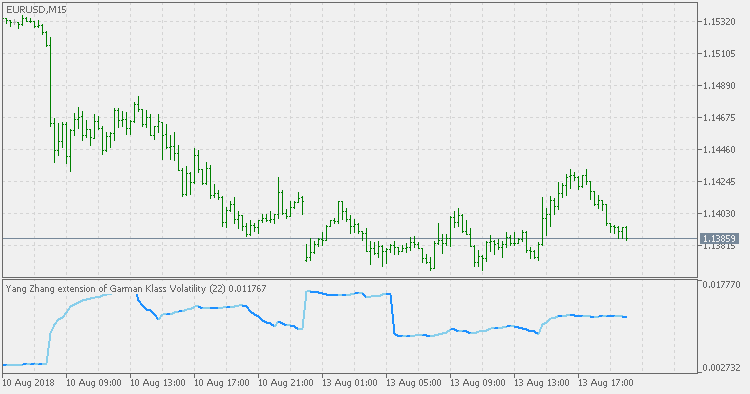

指标: Yang Zhang 扩展的 Garman Klass Volatility - 文章,程序库评论 - MQL5 算法交易论坛

Yang-Zhang Volatility in Python - by Sofien Kaabar, CFA

Yang & Zhang’s realized volatility: Automated estimation in Python ...

Volatility Modeling With Python 1725384188 | PDF | Volatility (Finance ...

Option Implied Volatility using Newton's Method in Python - YouTube

Free download of the 'Yang Zhang extension of Garman Klass Volatility ...

how to calculate volatility in python - YouTube

Python for Finance: Understanding Return Calculations and Volatility ...

Implied Volatility and Volatility Smile: Computing IV in Python ...

Quant Project | Build a Volatility Surface in Python - YouTube

Highly Cited Researcher 2025 - Prof. Yang Zhang - NUS CSI

How to Build a Volatility Trading Dashboard in Python with Interactive ...

programming - Volatility differences - Quantitative Finance Stack Exchange

Yang-Zhang Volatility Estimator | VolRadar

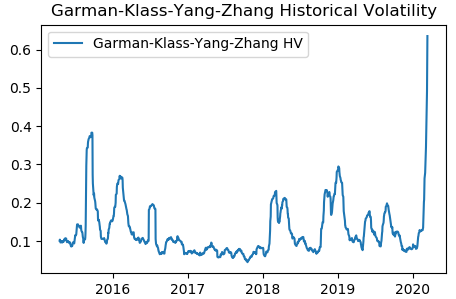

Garman-Klass-Yang-Zhang Historical Volatility Calculation Volatility ...

A complete set of volatility estimators (based on Euan Sinclair's ...

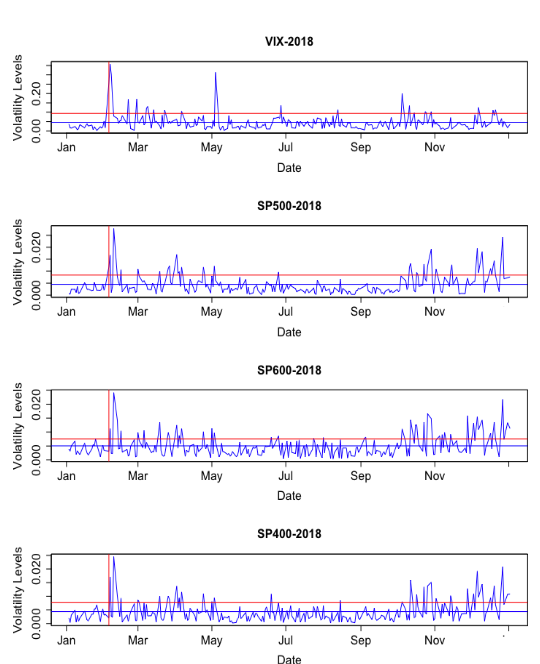

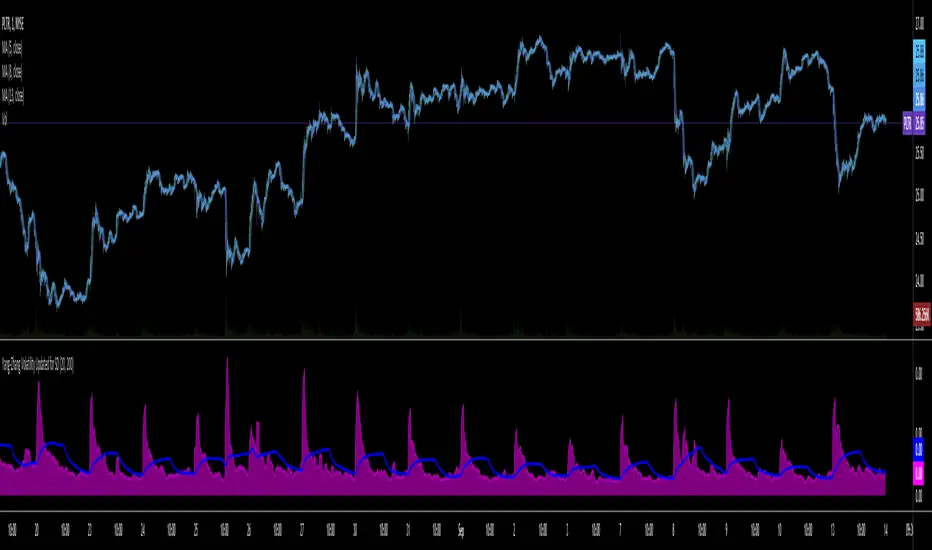

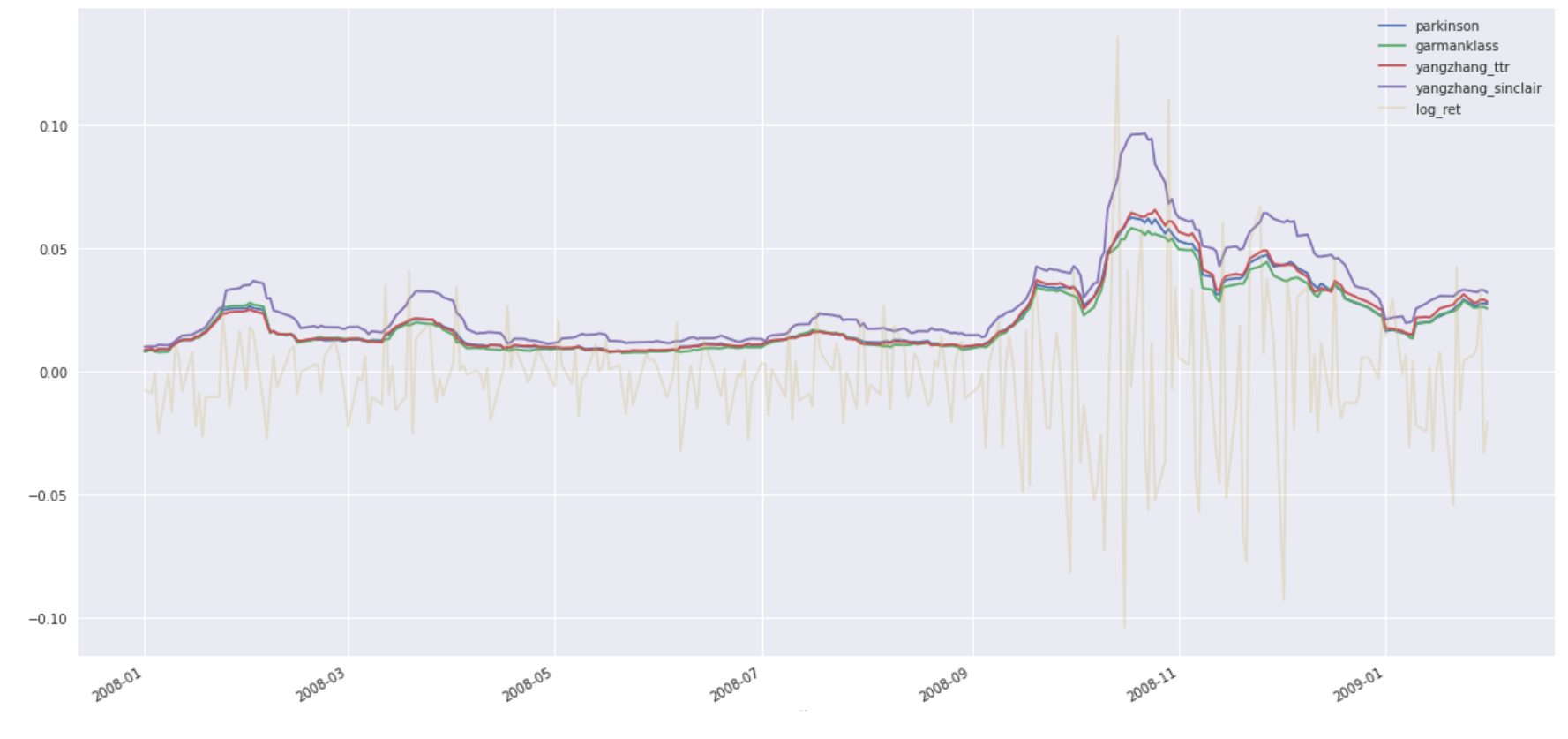

S&P 500 volatility for a 20 day time interval produced by the ...

S&P 500 volatility for a 60-day time interval produced by the ...

Garman-Klass-Yang-Zhang Historical Volatility Calculation – Volatility ...

Yang-Zhang Volatility (YZVol) by CoryP1990 – Quant Toolkit — CoryP1990的 ...

Garman-Klass-Yang-Zhang Historical Volatility Bands [Loxx] — Indicator ...

Volatility formulas in Sinclair's "Volatility Trading" book differs ...

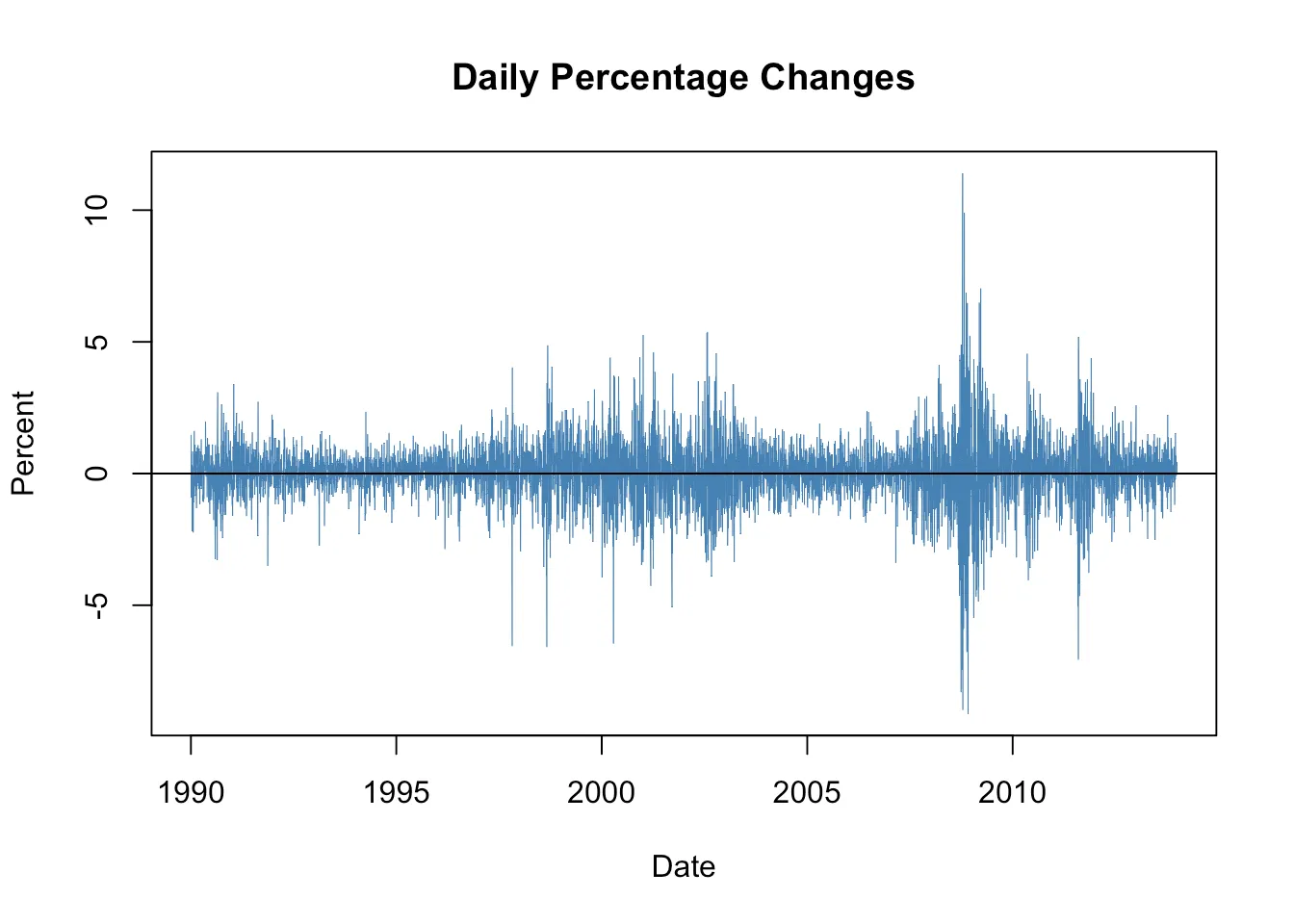

Relating Returns to Market Volatility | by Deephaven Data Labs | The ...

Garman-Klass-Yang-Zhang Volatility Estimator — Indicator by Firedrops ...

Yang-Zhang Volatility - by Jakub - Quant Journey with Code

Stream episode Garman-Klass-Yang-Zhang Historical Volatility ...

Volatility Trading Systems with Python: From Vol Surfaces to Gamma ...

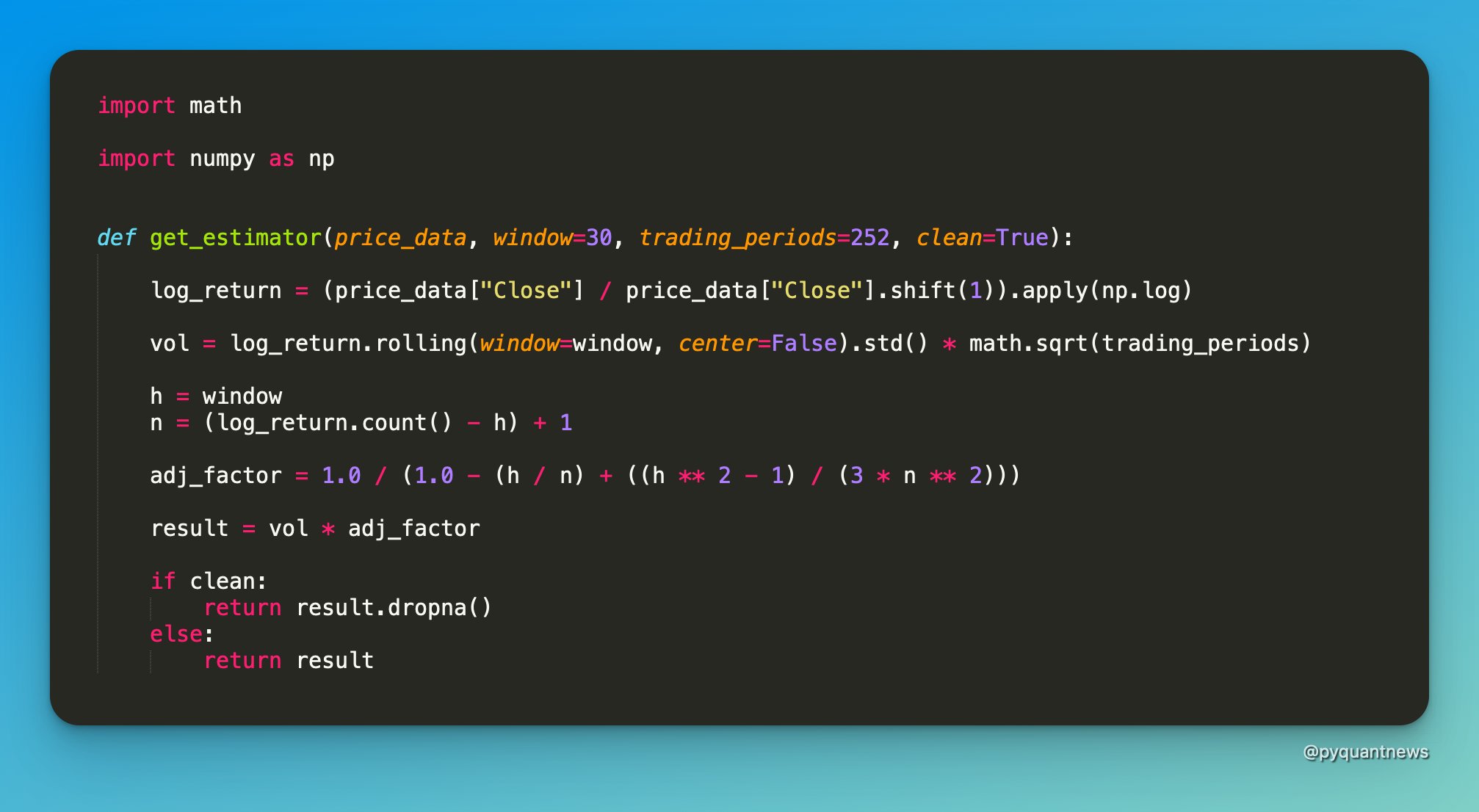

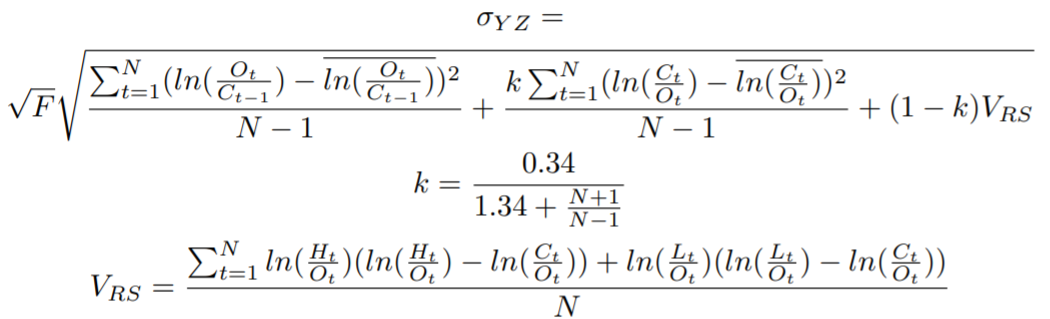

Introduction to Volatility Estimation and Yang-Zhang Estimation Method ...

Working with Binary Files in Python | by Gilbert Teklevchiev | Medium

Yang-Zhang Volatility — Indicator by kochub — TradingView

Standard Volatility Vs Yang-Zhang's Volatility over Regimes | Download ...

Exploring the predictability of range‐based volatility estimators using ...

S&P 500 volatility for a 20-day time interval produced by the ...

GitHub - white07S/cross-validation: Volatility measure and visulization ...

YANG-ZHANG extension of the GARMAN-KLASS volatility for ProRealTime ...

Volatility Trading Strategies with Python: From VIX to Vega Neutral ...

The volatility estimators from Euan Sinclair's Volatility Trading ...

用 Python 打造市场情绪指标:volatility、VIX 比率与板块动态分析 - 知乎

(PDF) Trinomial Option Pricing Model with Yang-Zhang Volatility

Chapter 13. Form : 4. Compute stock volatility

Yang-Zhang Volatility Updated for SD — Indicator by izzycalderisi ...

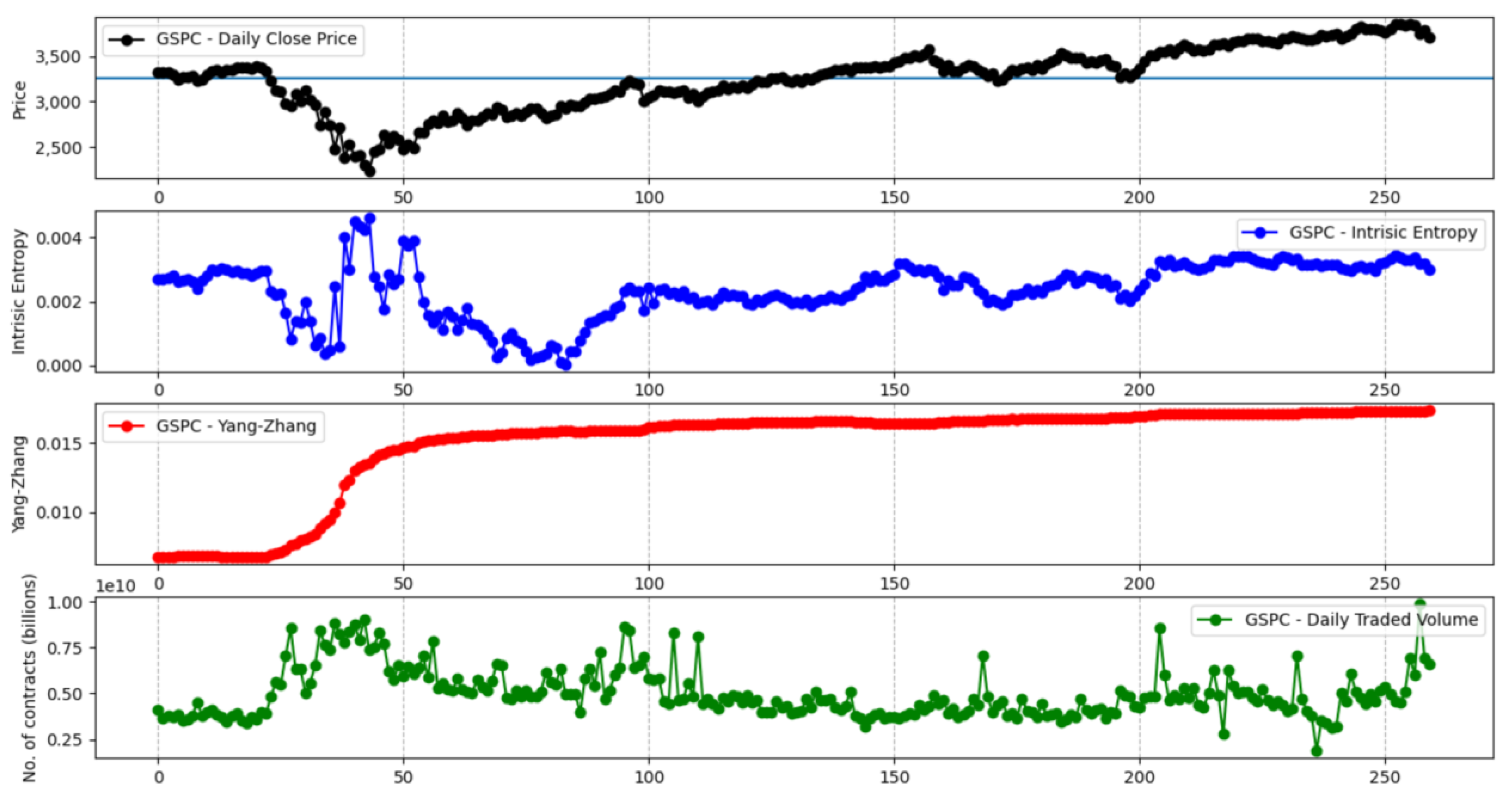

A Volatility Estimator of Stock Market Indices Based on the Intrinsic ...

Volatility | Options trading strategy in Python: Basic | Quantra Course ...

OHLC volatility (Part 2): Rogers-Satchell and Yang-Zhang (Excel) - YouTube

Intraday Implied Volatility: What Python + Options Data Reveal - YouTube

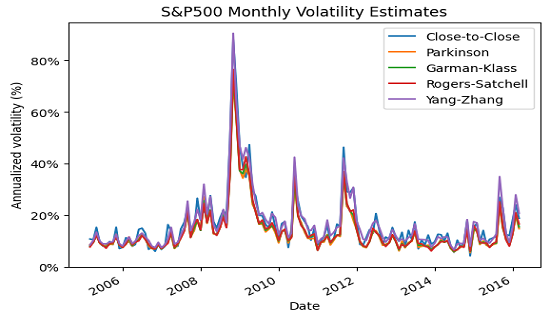

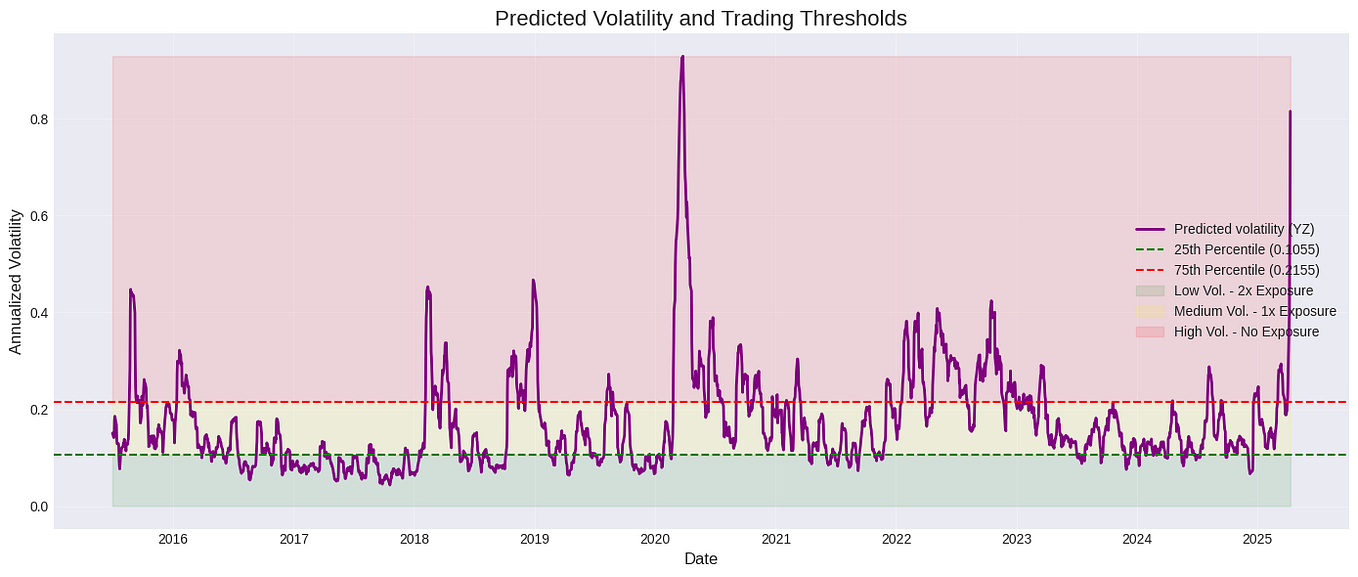

Volatility Estimators - QUANTREO

Volatility Trading With Python(Preview) #python #trading # ...

Yang-Zhang Volatility — Indicator by wpatte15 — TradingView

Range-Based Volatility Estimators: Overview and Examples of Usage ...

The Volatility Odyssey: A Journey Through Time Series Models with ...

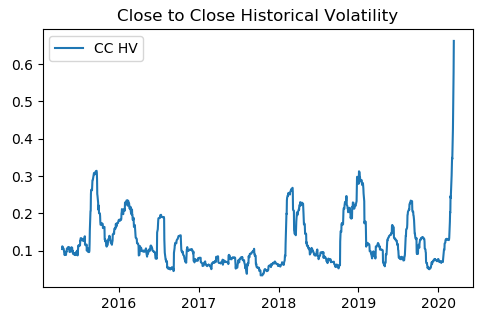

Close-to-Close Historical Volatility Calculation Volatility Analysis in ...

Volatility Engines: Building Adaptive Volatility-Driven Trading Systems ...

Volatility Modeling 101 in Python: Model Description, Parameter ...

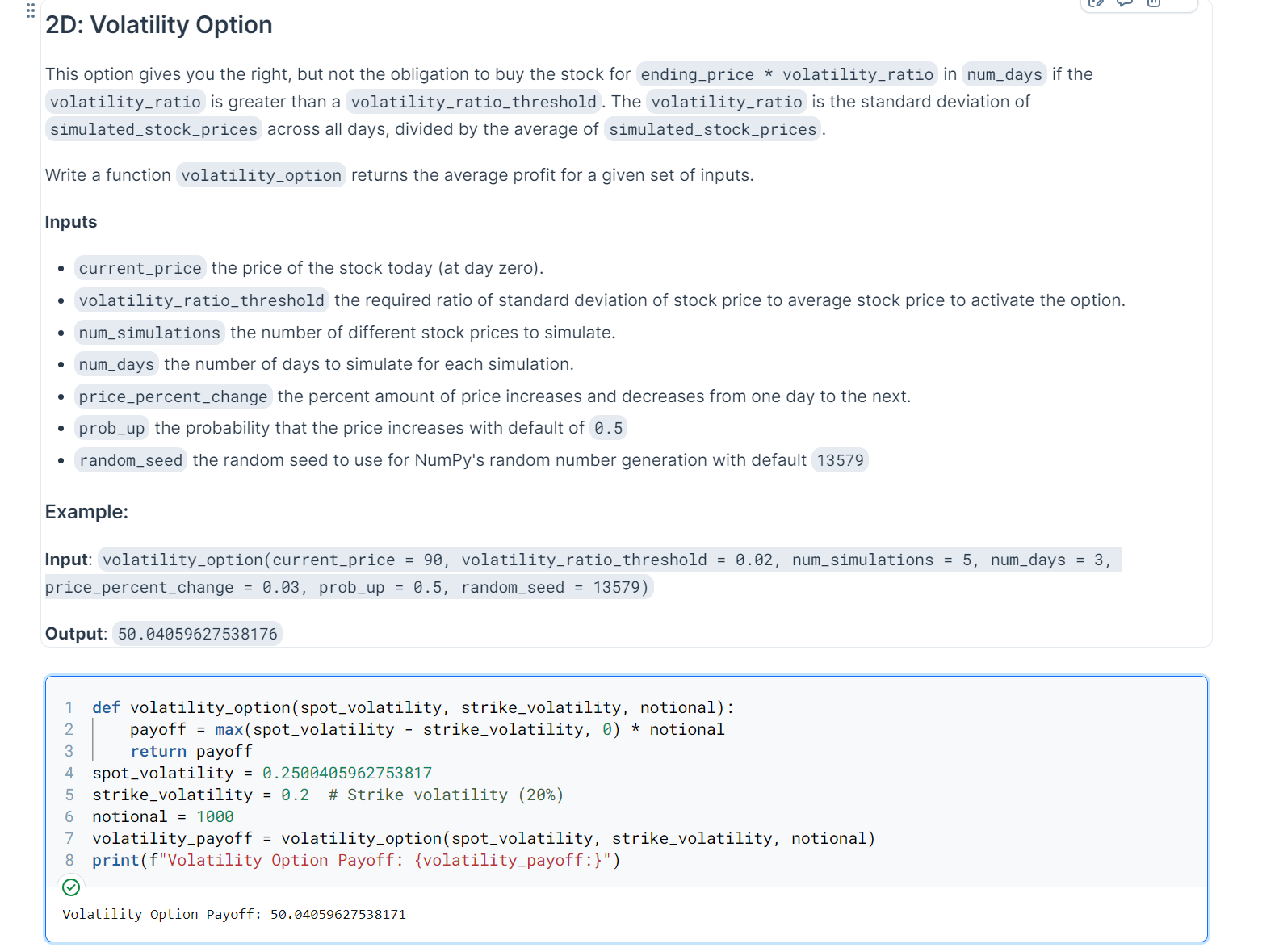

Solved Volatility Option in Python: I am trying to figure | Chegg.com

PyQuant News 🐍 on Twitter: "Hodges-Tompkins Hodges-Tompkins volatility ...

The Ultimate Guide To Pricing Options and Implied Volatility With ...

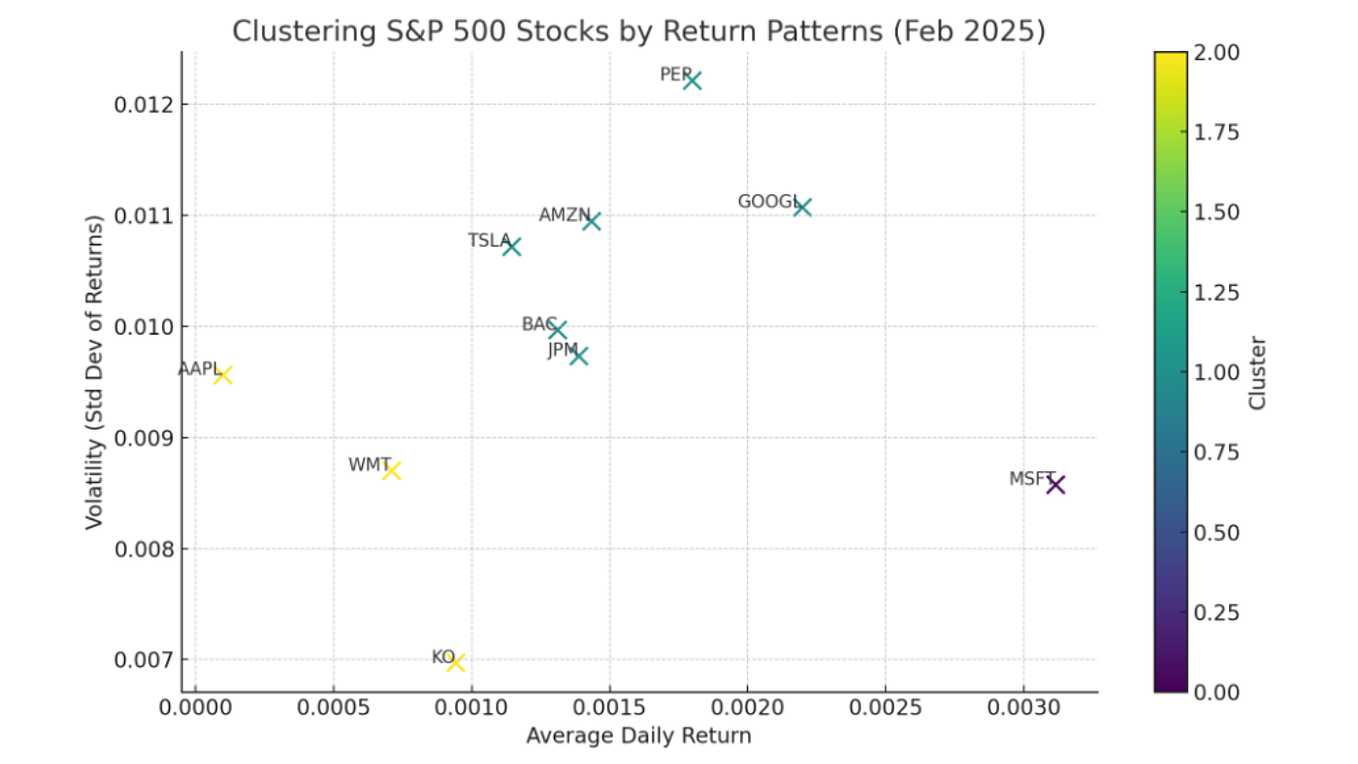

Exploratory Data Analysis (EDA) in Finance using Python

GitHub - hugogobato/Yang-Zhang-s-Realized-Volatility-Automated ...

Fernando J. De Mendonca on LinkedIn: #mql4 #metatrader #mt4 #mql4 # ...

GTC vs. Day Orders: Which Order Type Wins for Systematic Traders? | by ...

7 Maneras de Calcular la Volatilidad

How do you measure realized volatility? Let me count the ways ...

Yang-Zhang Volatility: The Indicator Most Traders Ignore | by Nayab ...

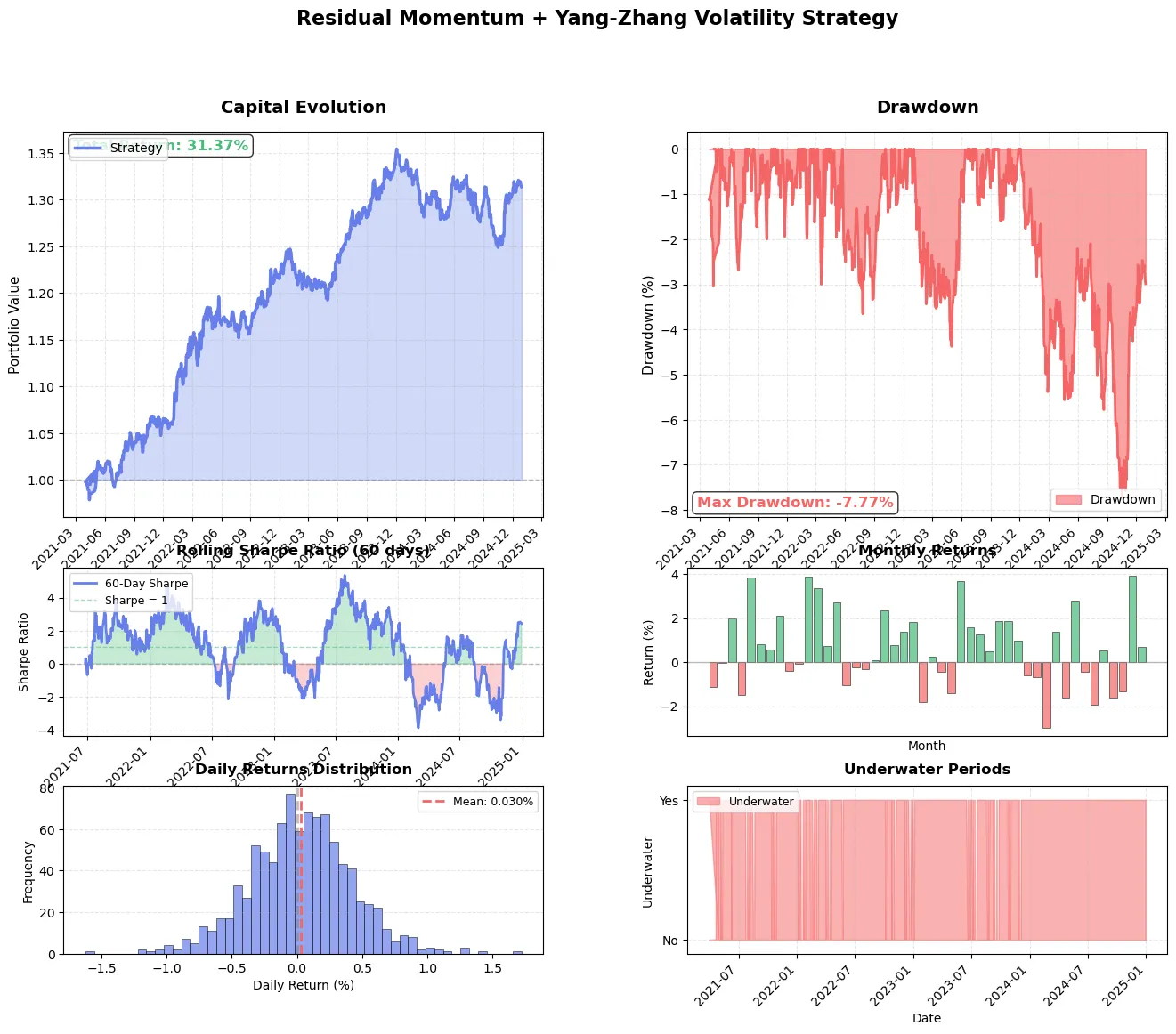

The Sophisticated Momentum Secret: Residual Alpha + Yang-Zhang ...

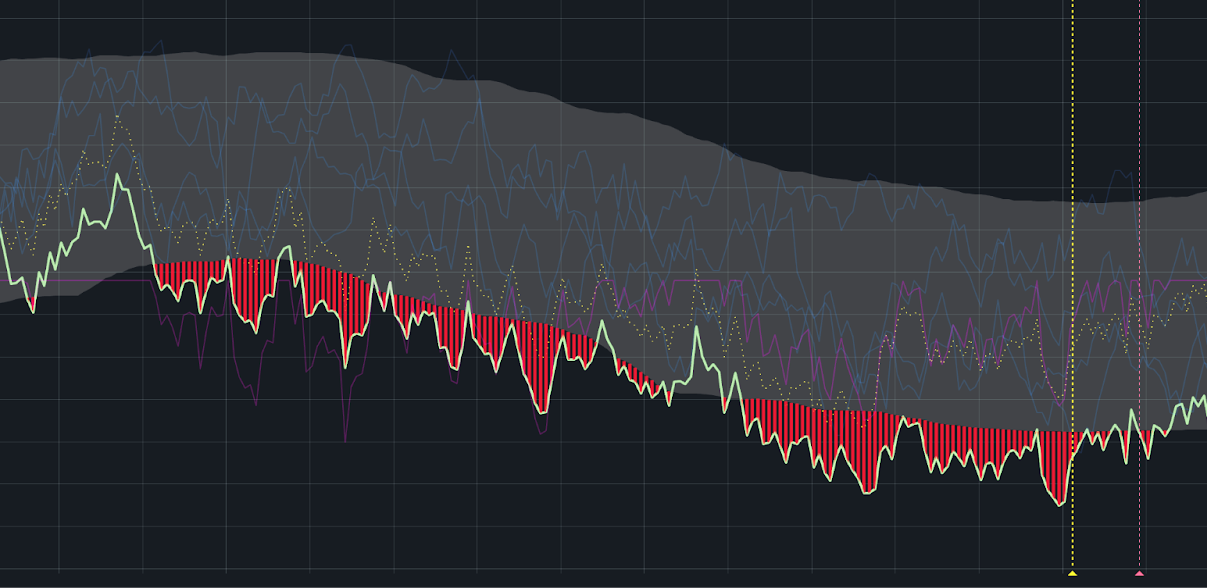

Timing re-entry into equities with a market regime model · Principia Mundi

Daily Yang-Zhang volatility, 23. Nov. 2012 -15. Aug. 2018 | Download ...

GitHub - MajorLift/volatility-modeling-python-datasci: "Modeling ...

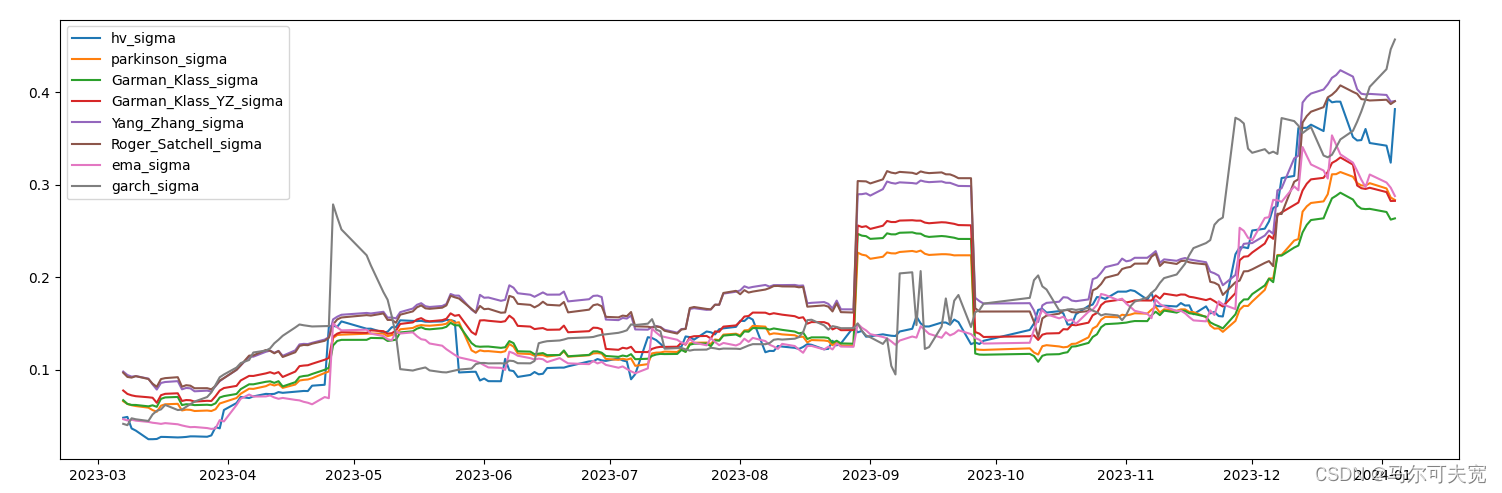

How do you measure volatility? Let me count the ways: • Garman Klass ...

Figure A10. Yang-Zhang estimates and the intrinsic entropy-based ...

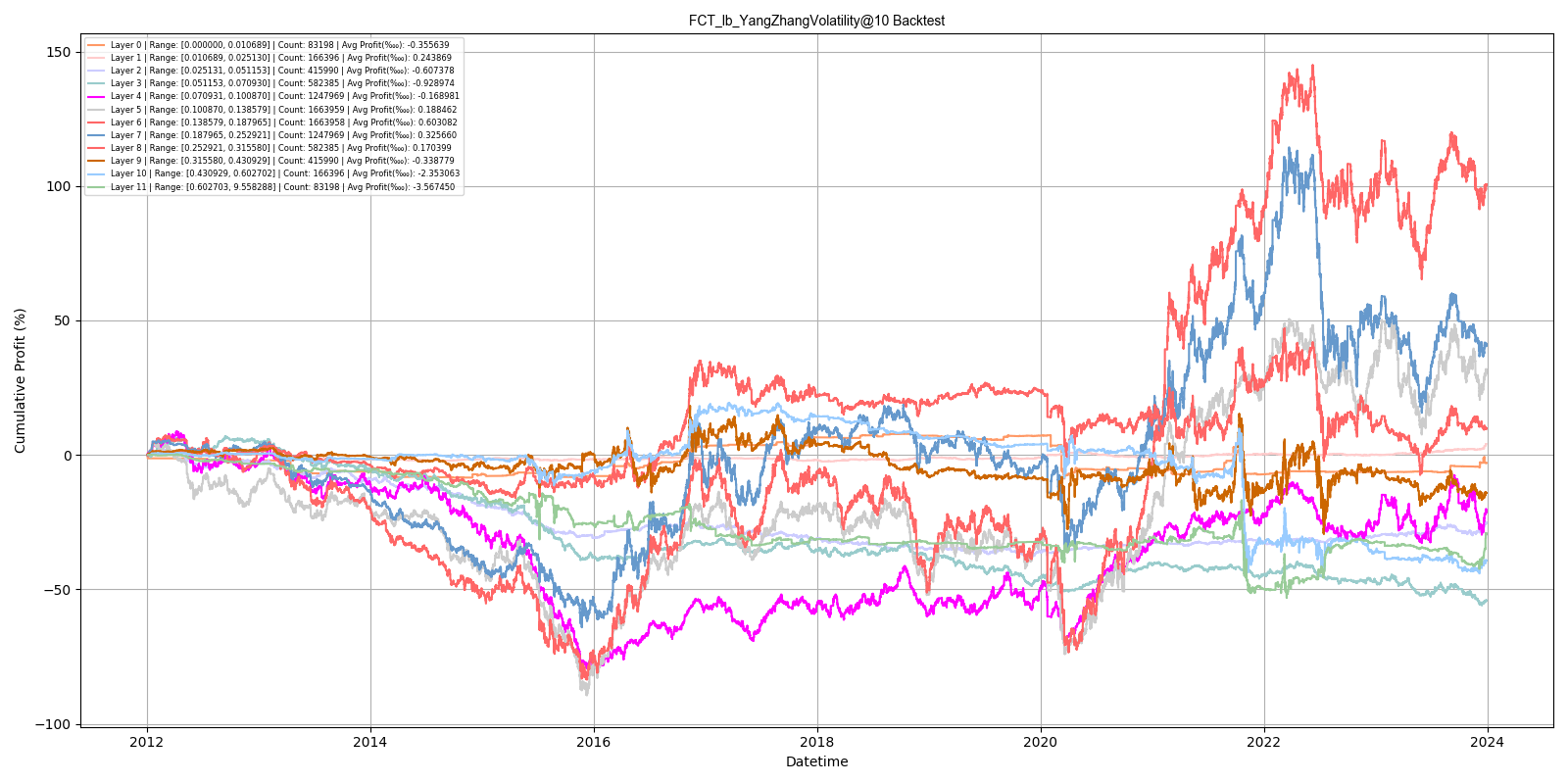

FCT_lb_YangZhangVolatility@10_evluation_minutes_2025-11-11_17_38_07.html

期权定价模型系列【13】标的资产波动率估计_yang-zhang波动率-CSDN博客

Third Generation Neural Networks: Deep Networks - MQL5 Articles

GitHub - inevitable2103/Volatility-Forecasting-using-Signature-Methods ...

Data Science Faculty | University of North Texas

Implied Volatility: Formula, Options, Python, Calculations and more ...

I will show 5 ways to compute "volatility" #python using #plotly | Zaur ...