Showing 120 of 120on this page. Filters & sort apply to loaded results; URL updates for sharing.120 of 120 on this page

Estimates of the EGARCH Equation Dependent Variable: INF t | Download ...

EGARCH estimation equation on the BOVESPA Daily Returns. | Download ...

EGARCH estimation equation on the IPyC Daily Returns. | Download ...

Specify EGARCH Models - MATLAB & Simulink

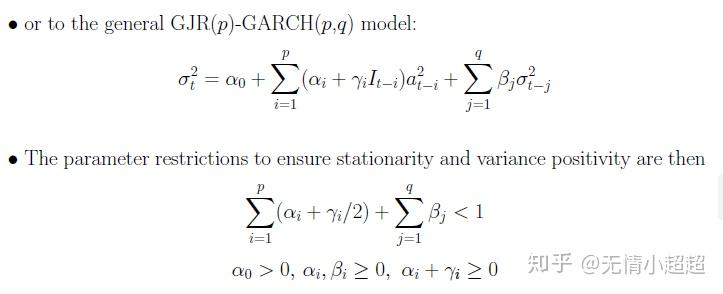

GJR-ARCH model & EGARCH model - 知乎

Regression results of EGARCH (1,1) and TGARCH (1,1) | Download ...

Estimation results of EGARCH model with normal and student's t ...

Parameters of Variance Equation (EGARCH) | Download Scientific Diagram

Estimated coefficients of conditional variance equations for EGARCH (1 ...

Conditional Variance EGARCH Model | Download Scientific Diagram

Estimated EGARCH models: Variance equation. | Download Scientific Diagram

EGARCH (1,1) Estimate of Returns | Download Scientific Diagram

G#4 EGARCH Model Introduction - YouTube

egarch - EGARCH conditional variance time series model - MATLAB

EGARCH model: exponential asymmetric volatility persistence (Excel ...

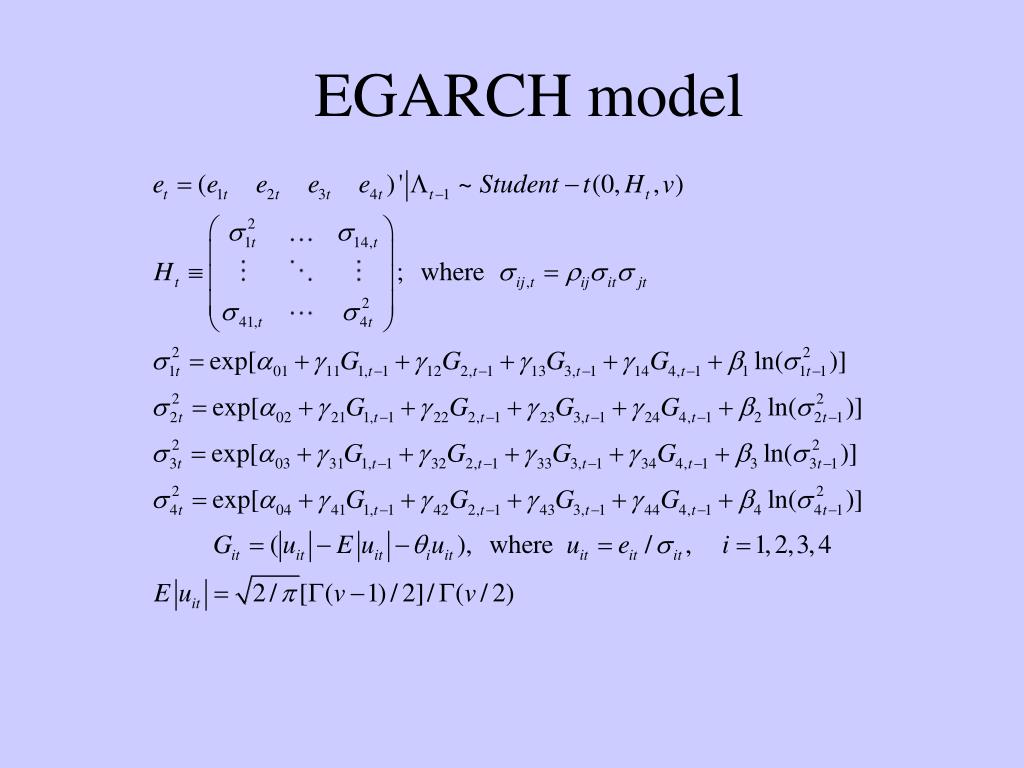

Estimation results of the switching bivariate EGARCH (1,1) model ...

Statistics for EGARCH and TGARCH Parameters for both Periods | Download ...

EGARCH: estimated coefficients of the conditional volatility equation ...

Estimation results for EGARCH model with MA specification. | Download Table

Estimates of EGARCH-ECM coefficients for variance equation | Download ...

Univariate EGARCH results (baseline model). | Download Scientific Diagram

EGARCH Process For Determining The Exchange Rate Volatility | Download ...

interpretation - Interpret Eviews Output: EGARCH - ARCH and GARCH term ...

DCC-(MV)-EGARCH variance equation results | Download Table

Result of EGARCH (1, 1) and TARCH (1, 1) Model | Download Scientific ...

Solved The following is EGARCH model for which of the time | Chegg.com

Results of EGARCH (1.1) model during the whole period | Download ...

(PDF) GARCH, GJR GARCH & EGARCH

Simulation of an EGARCH process with low θ and high γ parameters ...

Results of EGARCH (Variance Equation) Impact of Terrorism on Stock ...

EGARCH Estimates for the Common Components of IPG | Download Table

Maximum Likelihood Estimation of EGARCH Model | Download Scientific Diagram

Results of EGARCH (Variance Equation) Impact of Terrorism (Event Day ...

Results of EGARCH (Variance Equation) Impact of Terrorism (Post Event ...

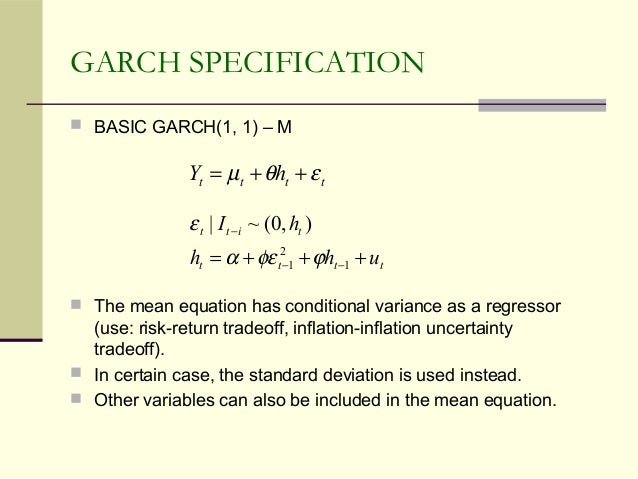

Egarch (1, 1), and the egarch (1, 1) - m models

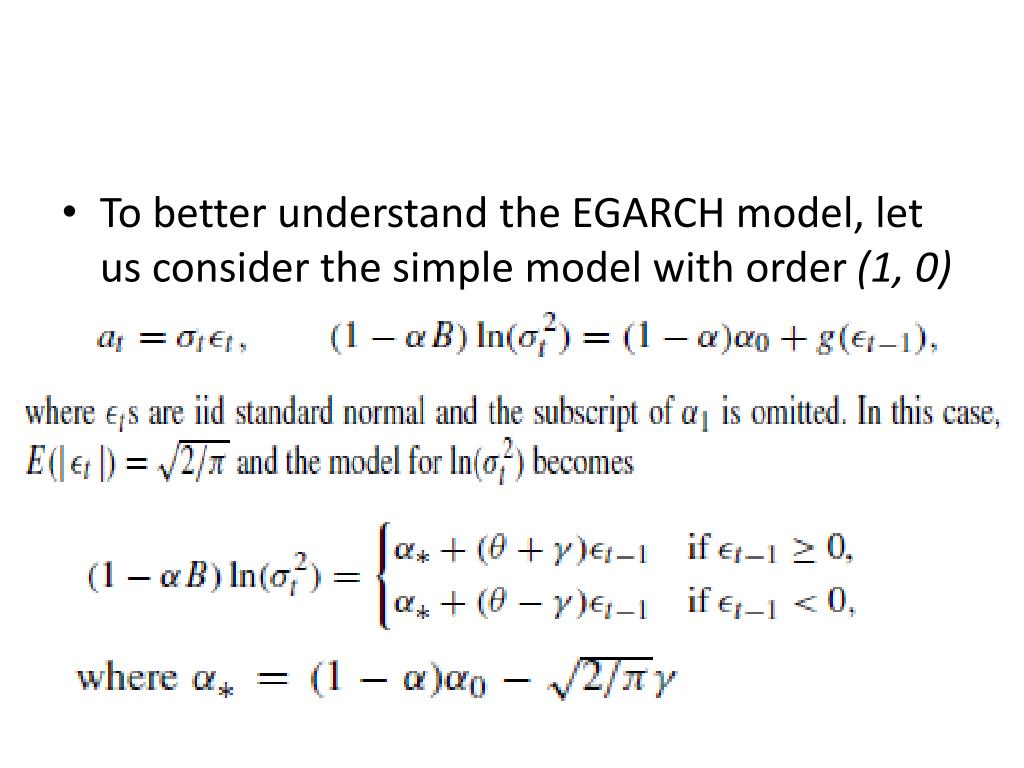

The model and residua 3.6. EGARCH model building I use the ARIMA model ...

Results of the Estimated EGARCH (1, 1) | Download Scientific Diagram

Empirical results of the EGARCH (1, 1) and GARCH models. | Download ...

GARCH (1,1), TGARCH and EGARCH Models for IT Index Returns | Download ...

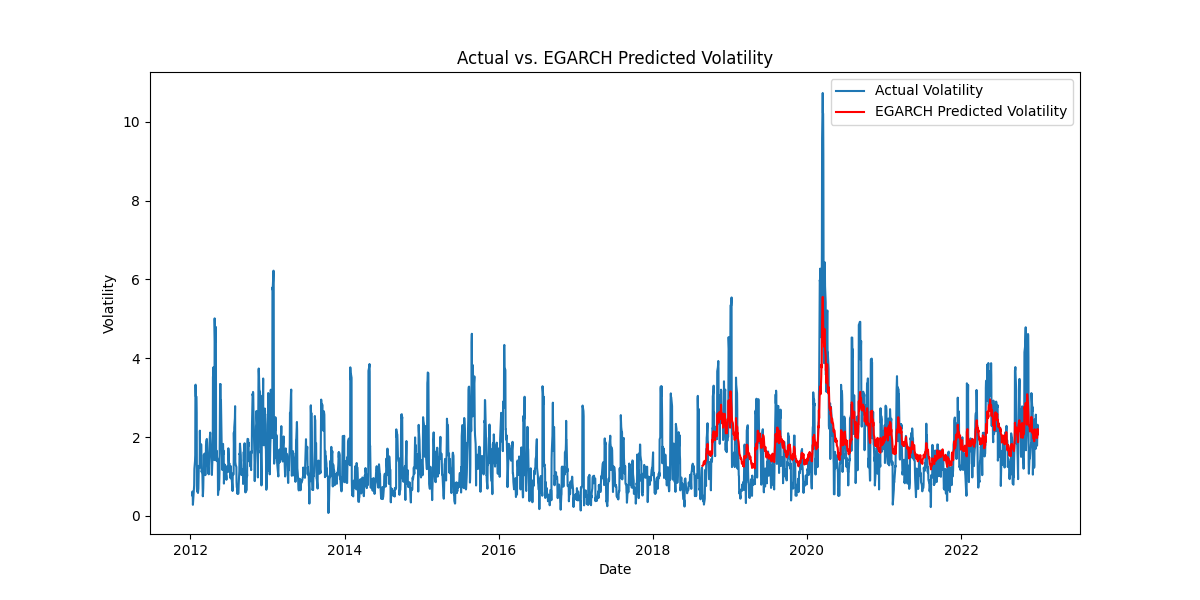

Conditional Standard Deviations of GARCH and EGARCH Models | Download ...

Solved: how to interpret EGARCH output in SAS ? - SAS Support Communities

Results of EGARCH Model for day-of-the-week returns | Download ...

Egarch Model | PDF | Null Hypothesis | Normal Distribution

EGARCH estimation results | Download Table

EGARCH model estimates of crude oil futures price yields in four crude ...

PPT - GARCH Models and Asymmetric GARCH models PowerPoint Presentation ...

(EViews10): How to Estimate Exponential GARCH Models #garchm #tgarch # ...

PPT - Chapter 4 PowerPoint Presentation, free download - ID:5496980

PPT - Week 10: VaR and GARCH model PowerPoint Presentation, free ...

PPT - Chapter 8 PowerPoint Presentation, free download - ID:3966639

ARCH and GARCH. Modeling Volatility Dynamics - online presentation

PPT - Democratic Politics and Financial Markets PowerPoint Presentation ...

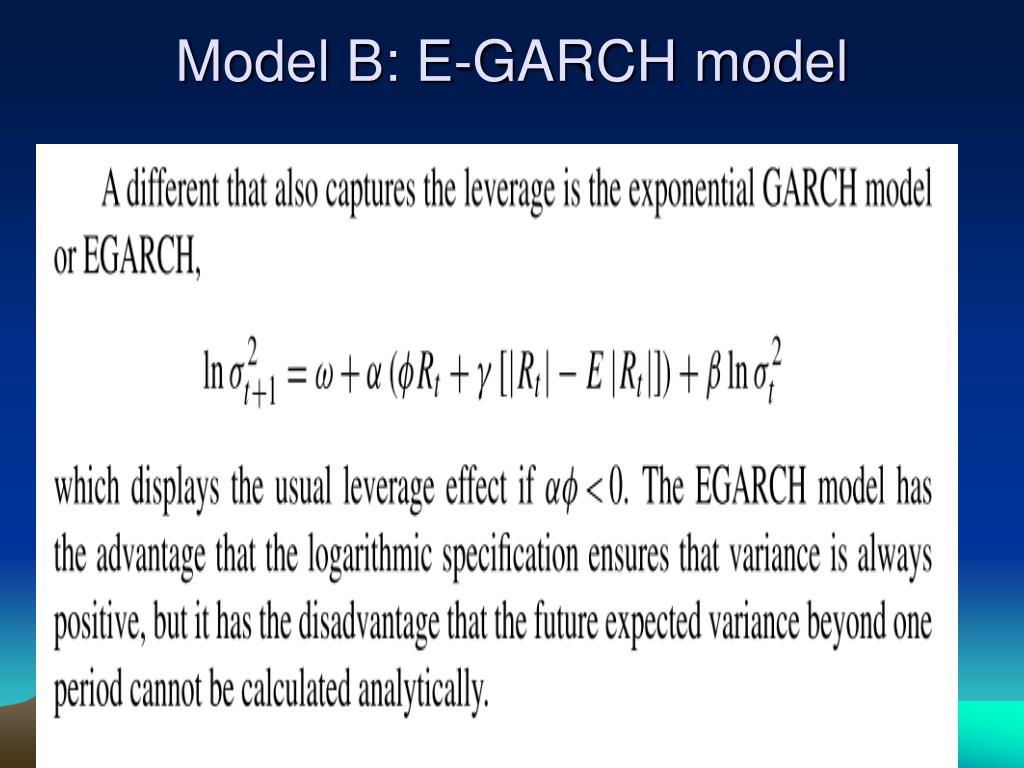

PPT - THE EXPONENTIAL GARCH MODEL PowerPoint Presentation, free ...

PPT - Lecture 8: Conditional Heteroscdastic Models PowerPoint ...

garch - EGARCH(1,1) mean - Quantitative Finance Stack Exchange

PPT - Leveraging PowerPoint Presentation, free download - ID:660088

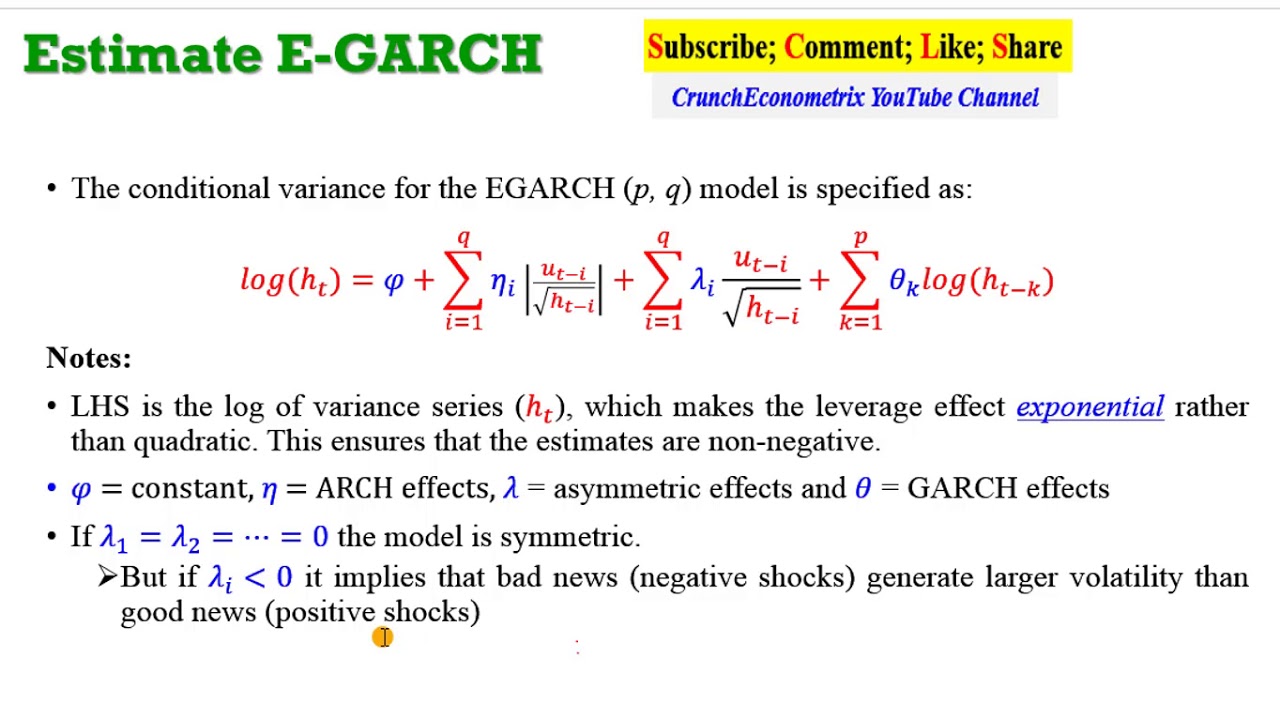

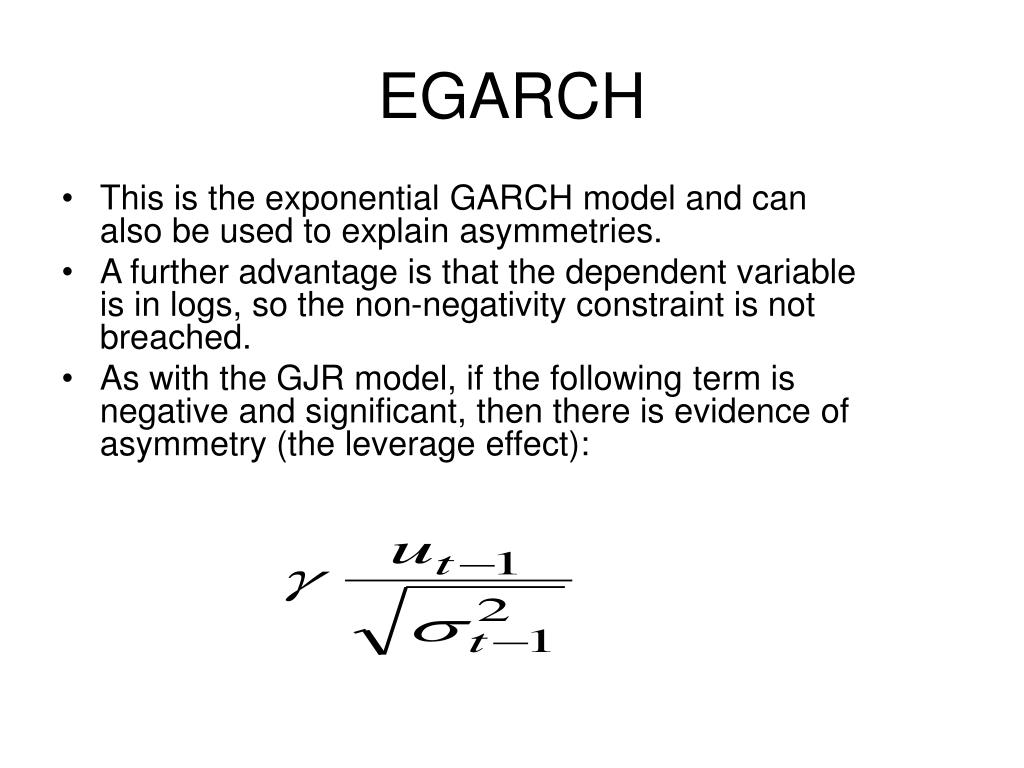

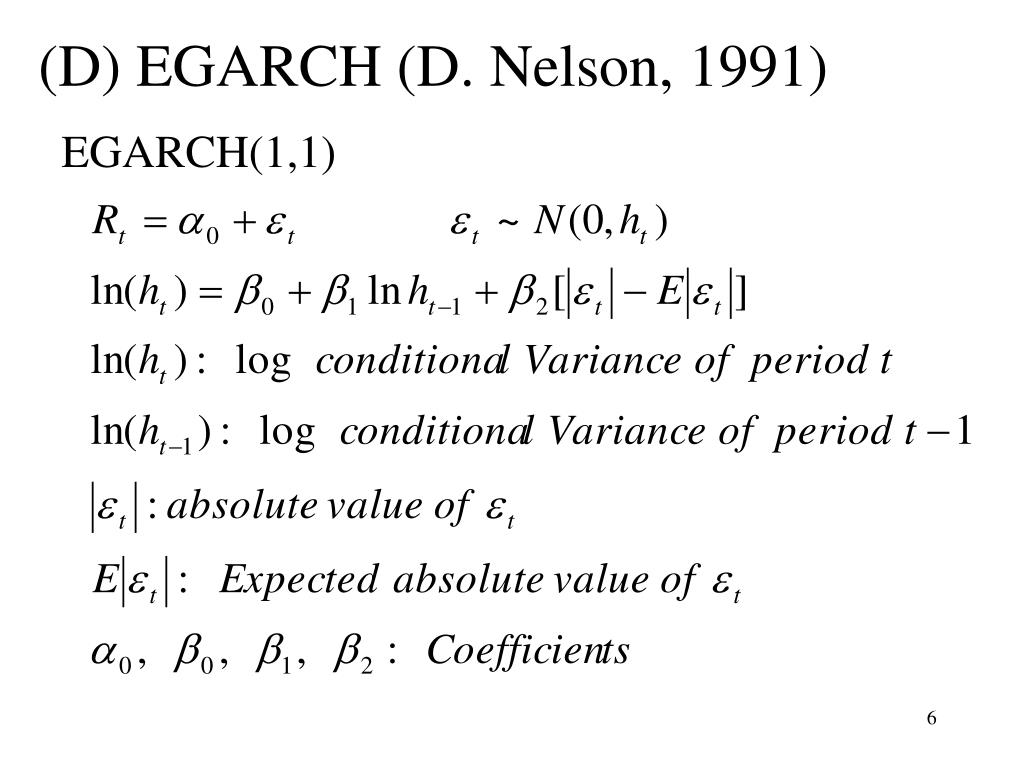

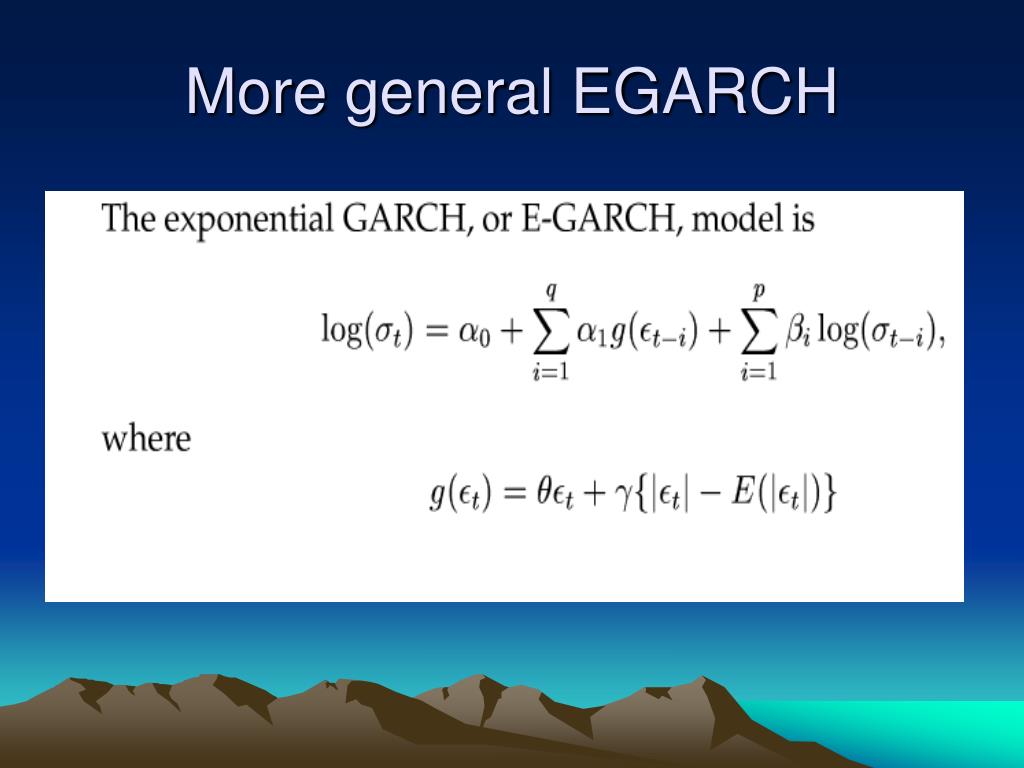

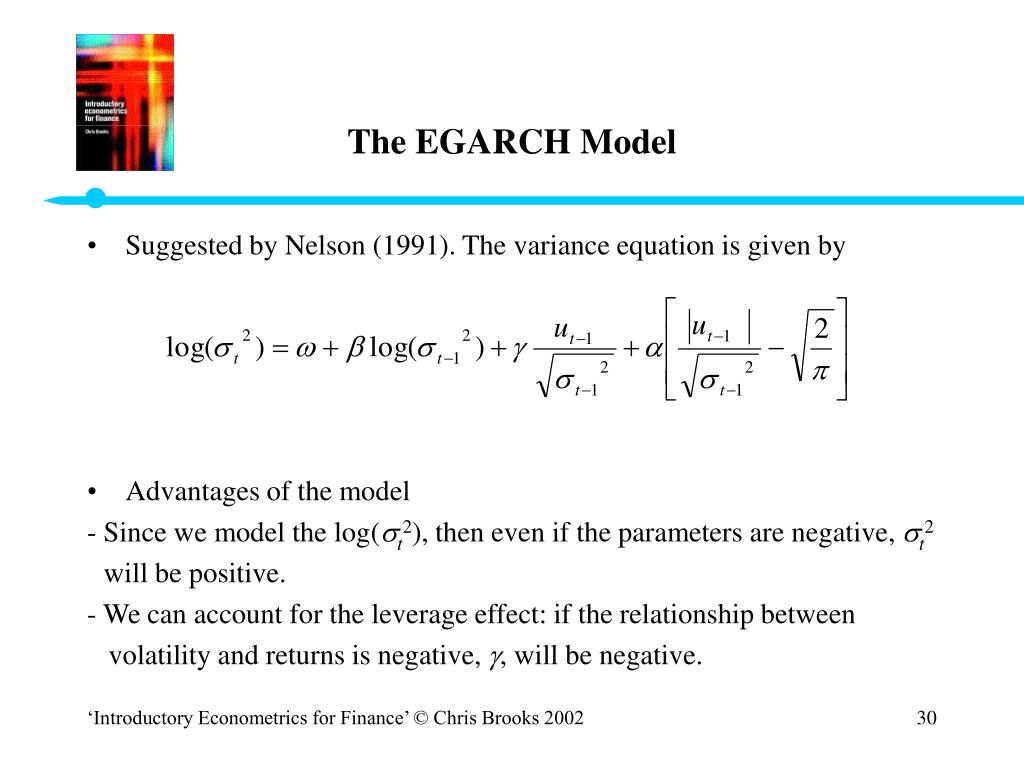

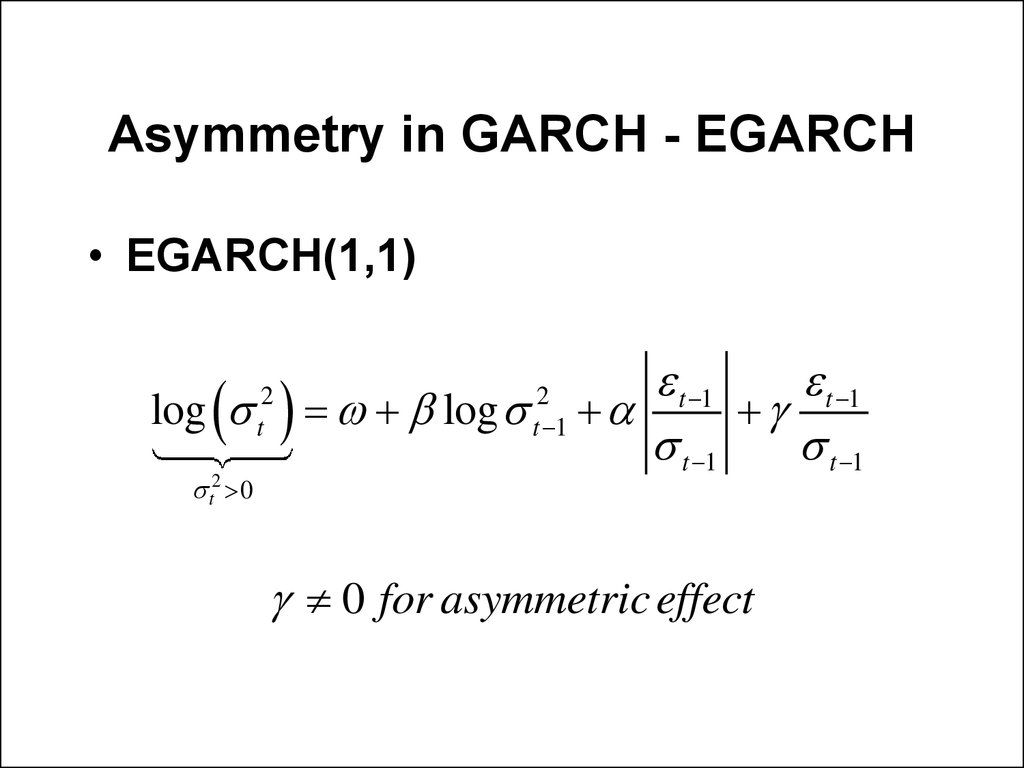

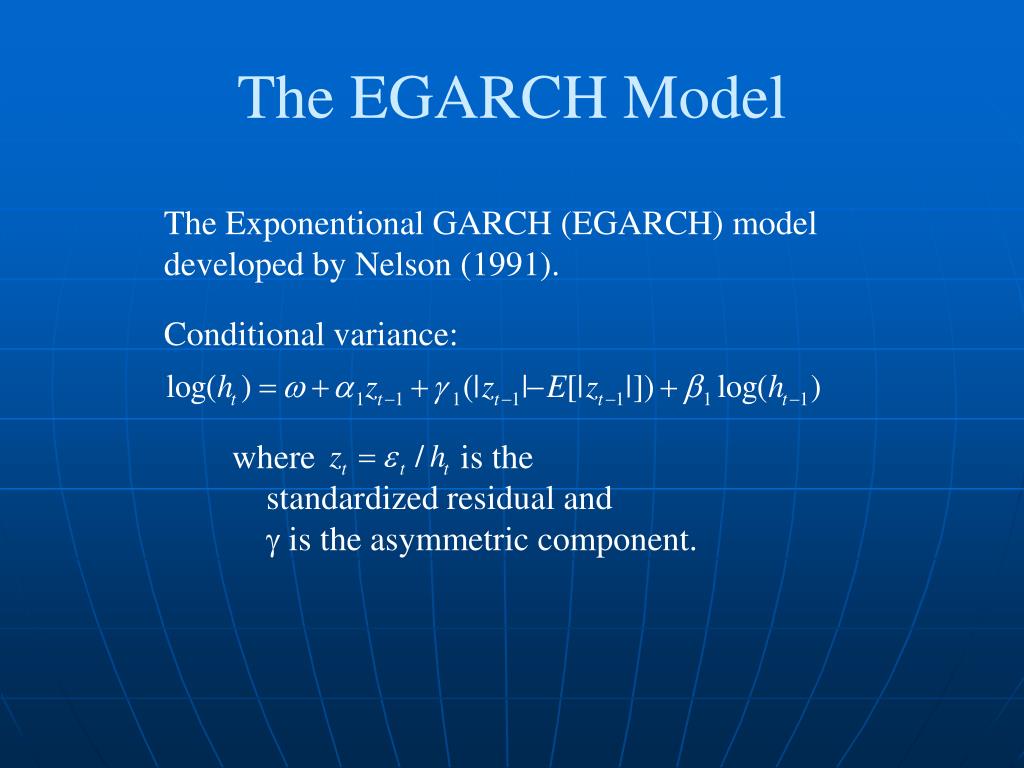

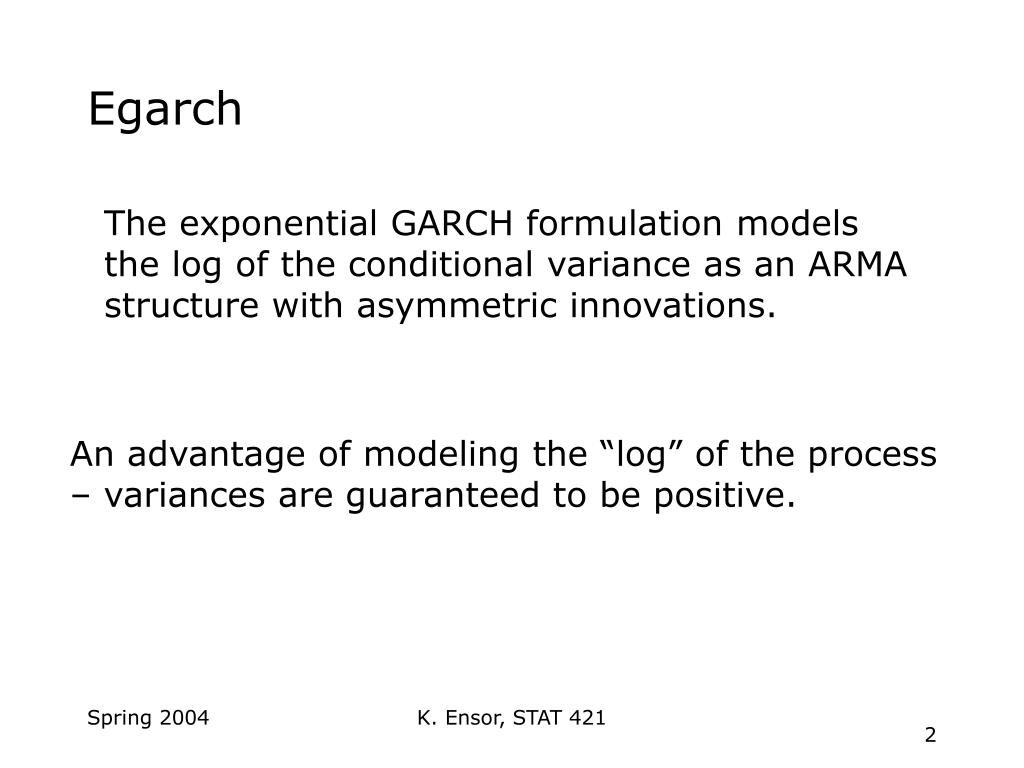

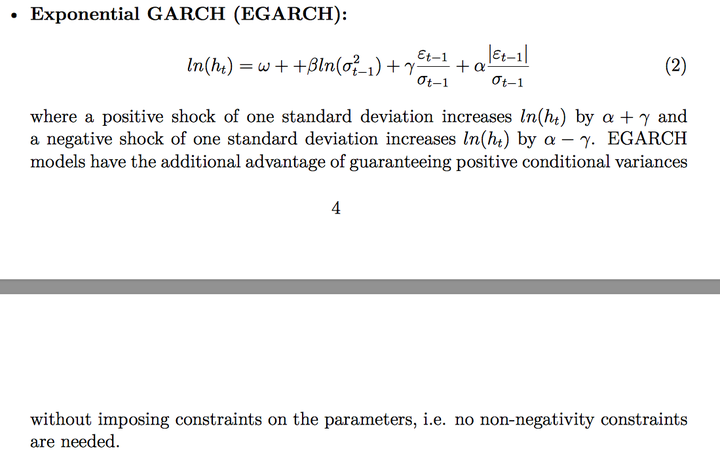

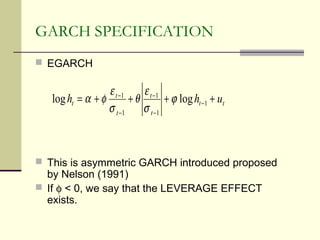

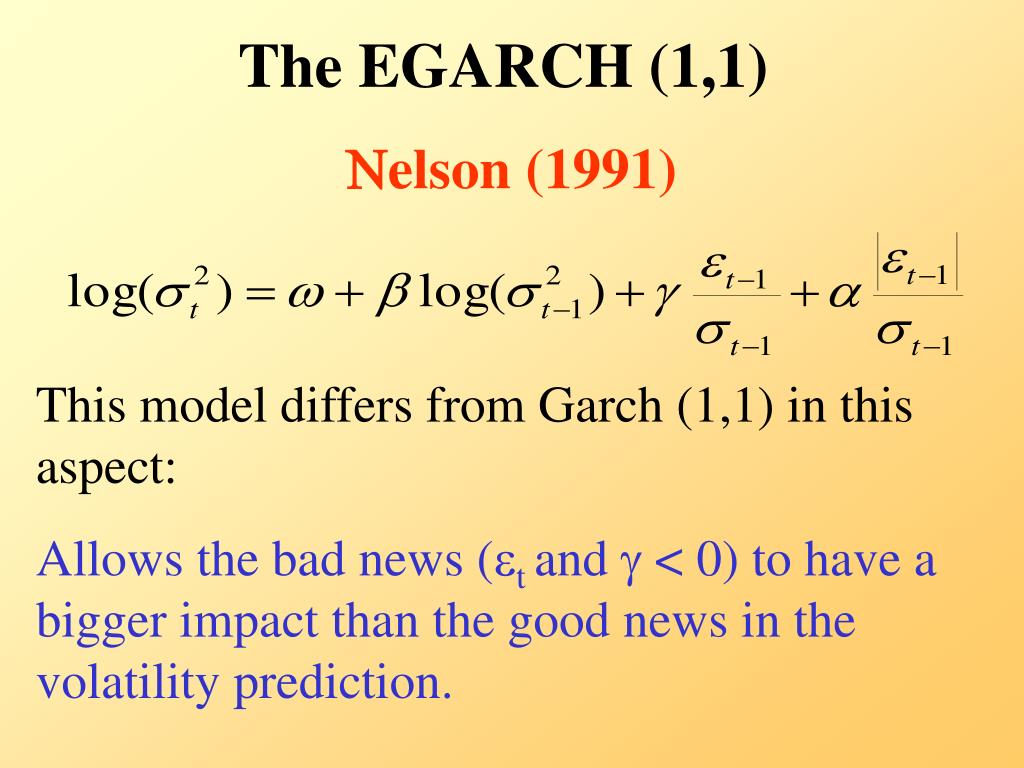

Another popular extended model of the GARCH model proposedby Nelson ...

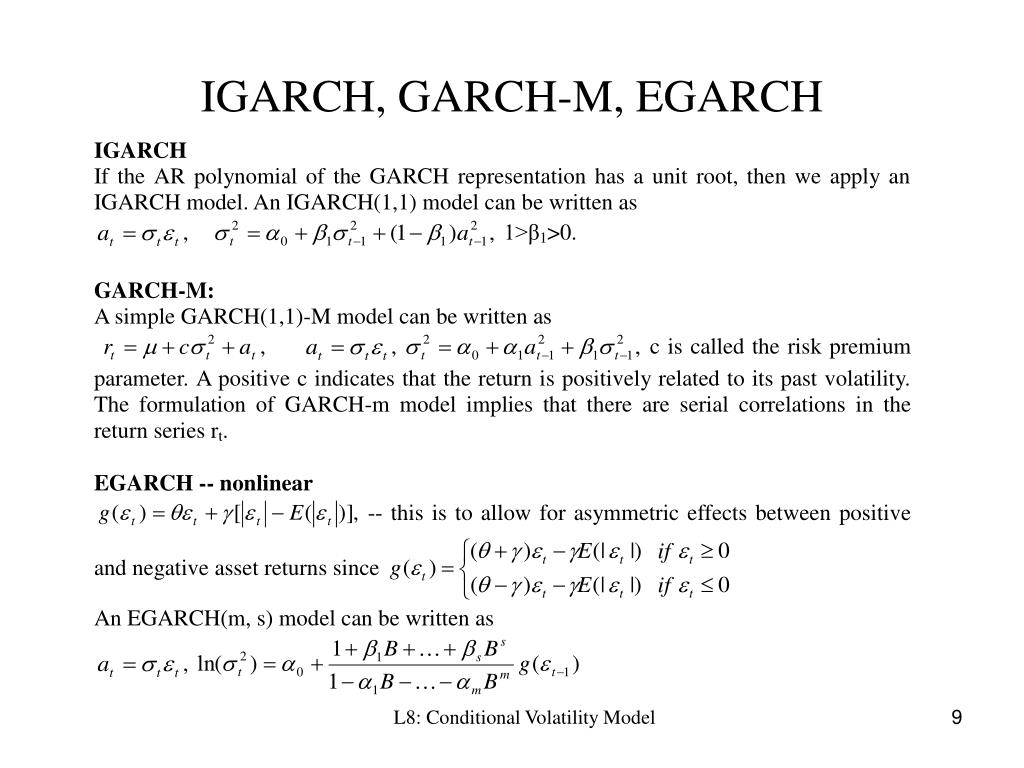

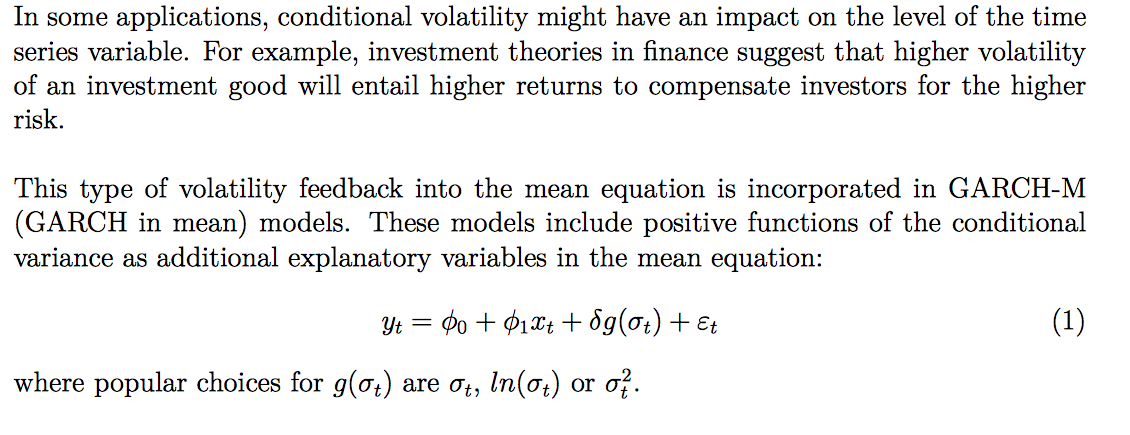

GARCH, IGARCH, EGARCH, and GARCH-M Models

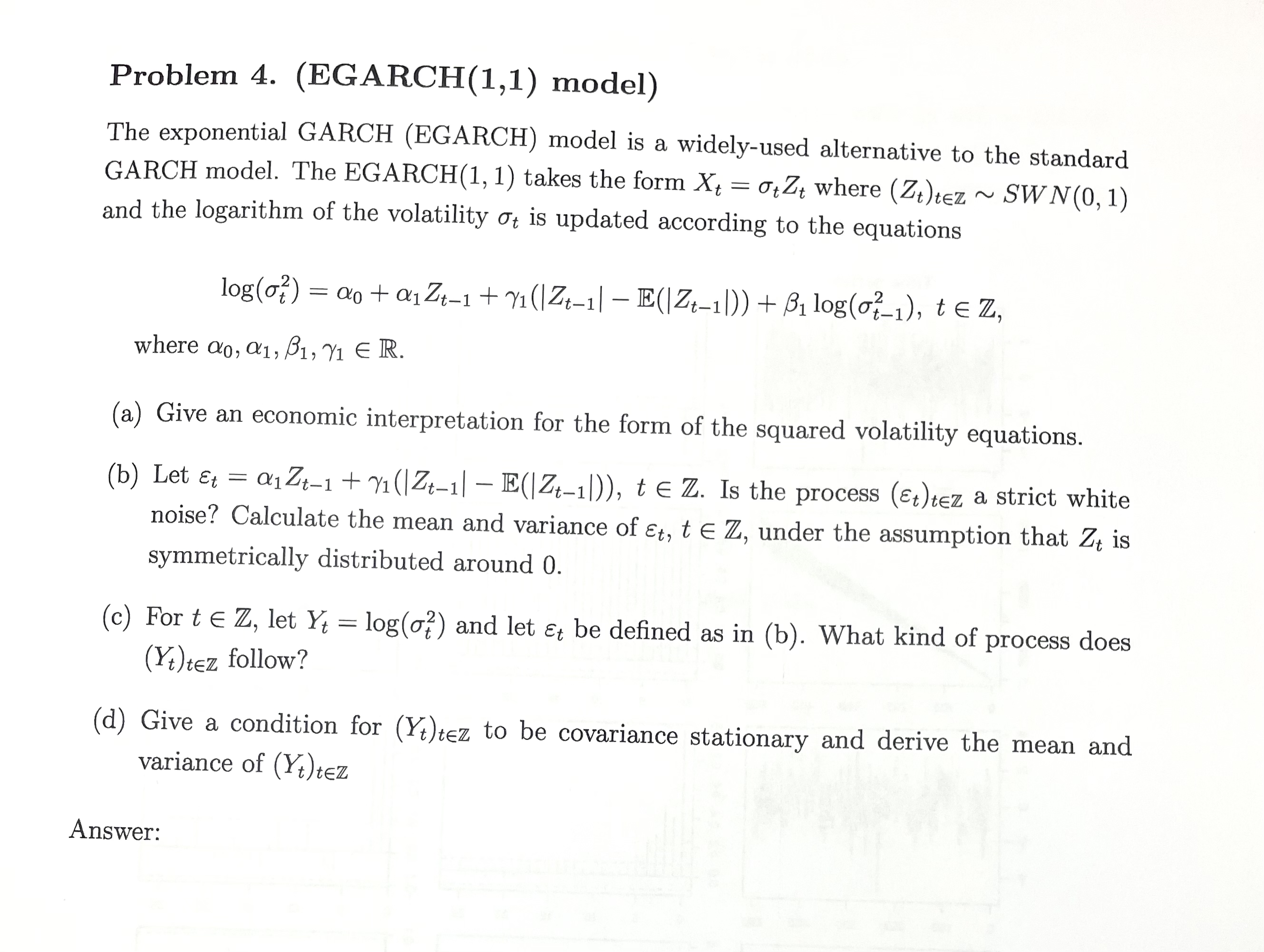

Solved Problem 4. (EGARCH(1,1) model)The exponential GARCH | Chegg.com

GARCH、GARCH-M、IGARCH、TARCH、EGARCH、PARCH、CGARCH模型-操作视频地址大全财经节析-张华节-计量经济学 ...

Arch Model Formula at Nettie Cox blog

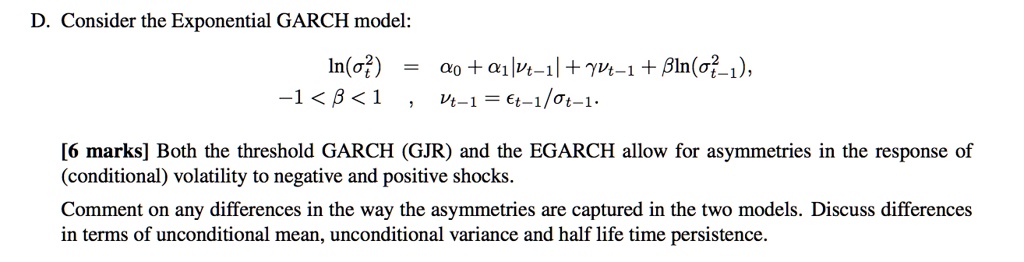

SOLVED: Consider the Exponential GARCH model: -1

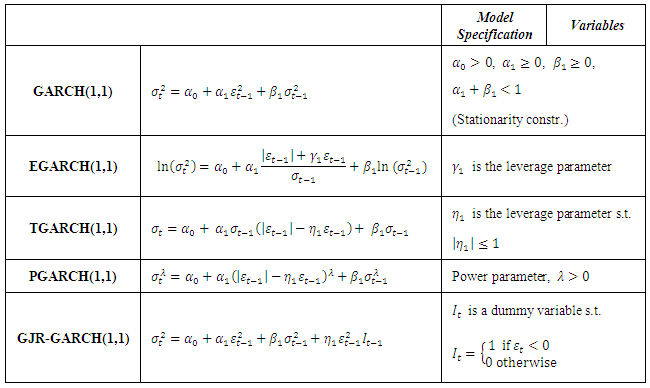

Overview of the GARCH-family models used | Download Table

How to interpret the resulting coefficients in the conditional variance ...

What Is GARCH Model In Python? - AskPython

Forecasting USD/MUR Exchange Rate Dynamics: An Application of ...

Modelling Volatility and the Risk-Return Relationship of some Stocks on ...

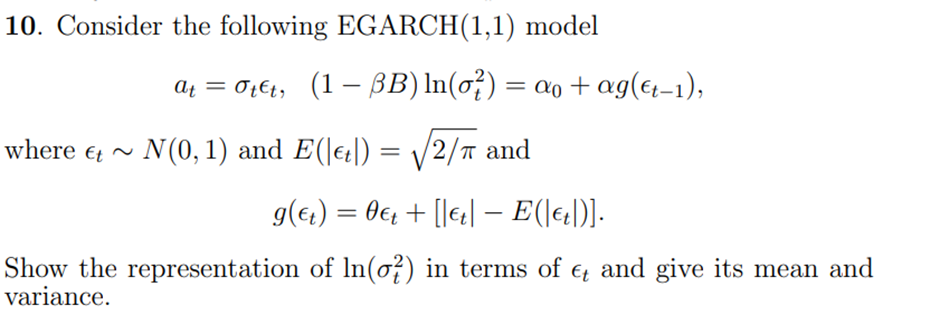

Solved 10. Consider the following EGARCH(1,1) model a_t = | Chegg.com

Financial econometrics xiii garch

PPT - 國際天然氣市場的訊息傳遞與價格互動 PowerPoint Presentation - ID:5064728

Sarveshwar Inani's Blog: GARCH Modelling

Estimation Statistics-Distribution Comparison AR(1)-EGARCH Model ...

The EGARCH(1.1) model estimates of Bank stock index returns | Download ...

GARCH - Tutorial and Excel Spreadsheet

244 questions with answers in FINANCIAL ECONOMETRICS | Science topic

How to interpret negative ARCH coeff. and positive leverage effect ...

Parameters Estimation EGARCH(1,1) | Download Scientific Diagram

Advanced GARCH Models: EGARCH, TGARCH, and PGARCH • Economics.Town

Volatility Modeling (part 1): Journey from ARCH to NN and MCMC

GitHub - zaniara3/DCC-EGARCH-Simulation: DCC-EGARCH with ARCH in Mean ...

GARCH模型的衍生模型(EGARCH IGARCH GARCH-M)的应用背景是什么? - 知乎

Financial econometrics xiii garch | PPT

Parameter Estimates of CC-EGARCH Model | Download Table

MODELOS ARCH, GARCH Y EGARCH: APLICACIONES A SERIES FINANCIERAS

Arch Model In R Example at George Bousquet blog

A.1: Various GARCH-EGARCH models Using Student's t-Distribution Applied ...

PPT - The Garch model and their Applications to the VaR PowerPoint ...

EGARCH(1,1) for daily index returns | Download Scientific Diagram

A.2: Various GARCH-EGARCH models Using Generalized Error Distribution ...

How to interpret bi-Variate EGARCH? | ResearchGate

presents the empirical results of the AR-EGARCH model. As shown in this ...

EGARCH: un modelo asimétrico para estimar la volatilidad de series ...

Results of the estimation of the EGARCH(1,1) model with the slope in ...