Showing 120 of 120on this page. Filters & sort apply to loaded results; URL updates for sharing.120 of 120 on this page

(continuation). Forecast comparison in the sample of the EGARCH (1, 1 ...

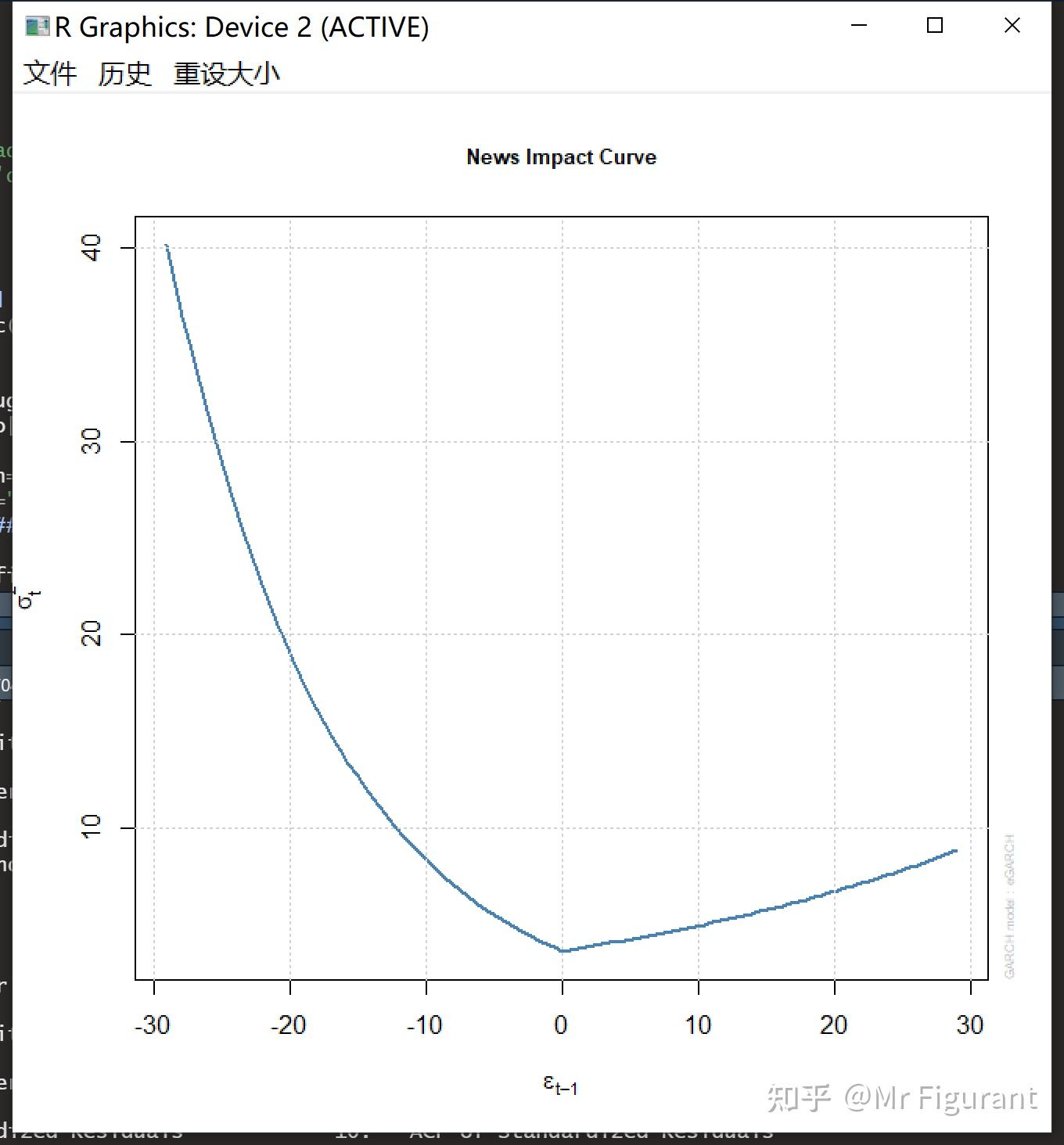

The EGARCH calibrated implied volatility skews are depicted for 30 day ...

EGARCH (1,1) Estimate of Returns | Download Scientific Diagram

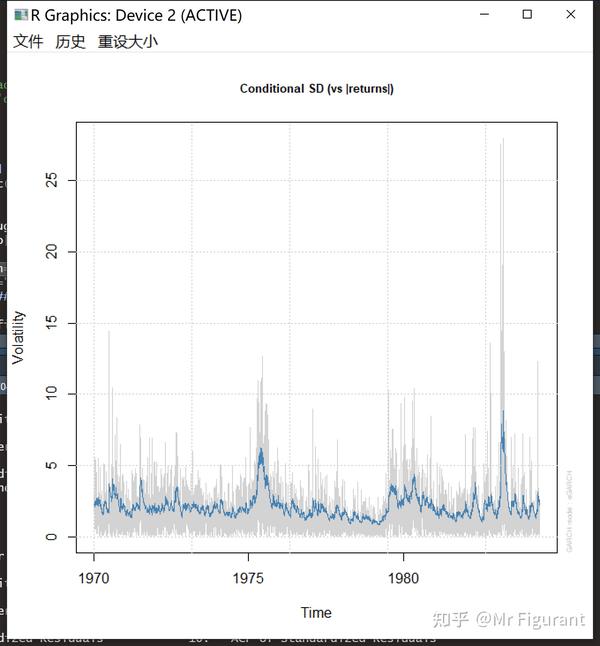

Conditional Standard Deviations of GARCH and EGARCH Models | Download ...

CSR Conditional EGARCH Volatilities | Download Scientific Diagram

Realized, Realized-EGARCH and EGARCH variances | Download High-Quality ...

4GARCH, TGARCH and EGARCH Estimate of Conditional Variance. | Download ...

Estimation results of EGARCH model with normal and student's t ...

Conditional Variance EGARCH Model | Download Scientific Diagram

Statistics for EGARCH and TGARCH Parameters for both Periods | Download ...

Regression results with an EGARCH model of the conditional variance ...

Estimated EGARCH models: Variance equation. | Download Scientific Diagram

Conditional standard deviation of EGARCH (1, 1) model (see online ...

Conditional variance of EGARCH (1, 1) model (see online version for ...

EGARCH model: exponential asymmetric volatility persistence (Excel ...

Inflation volatility graph of EGARCH ( 1,1 ) model. | Download ...

EGARCH Process (sub-period of 22/12/2004 15/05/2006)... | Download ...

Summary of EGARCH estimated results | Download Scientific Diagram

Figure2:The implied volatility of the GJR-GARCH and EGARCH calibrated ...

EGARCH volatility estimates and ETF investment size | Download ...

Volatility and Asymmetry Effects, Estimated Co-efficients of the EGARCH ...

Estimates of the EGARCH Equation Dependent Variable: INF t | Download ...

EGARCH (1,1) Model Results with IT dummy. | Download Scientific Diagram

Statistical property of EGARCH model | Download Scientific Diagram

AIC/SIC result from the initial EGARCH model | Download Scientific Diagram

Estimation of the EGARCH model with different distributions. | Download ...

Estimation Outputs of Multifactor GARCH, TGARCH and EGARCH Models ...

Diagnostic test of the GARCH (1,1), EGARCH (1,1) and TGARCH (1,1) model ...

EGARCH (1,1) model for the FPIM | Download Scientific Diagram

Results of the Estimated EGARCH (1, 1) | Download Scientific Diagram

Results of the EGARCH and GJR-GARCH Models | Download Scientific Diagram

Solved The following is EGARCH model for which of the time | Chegg.com

Maximum Likelihood Estimation of EGARCH Model | Download Scientific Diagram

The Estimation Results of EGARCH Model | Download Scientific Diagram

EGARCH estimation equation on the BOVESPA Daily Returns. | Download ...

7 EGARCH Model Estimates for Economic Indicators of Uncertainty ...

Estimation of The Egarch Model For All-share Index As The Dependent ...

EGARCH Process For Determining The Exchange Rate Volatility | Download ...

Results of the ARCH-LM test for the EGARCH model. | Download Scientific ...

Predicciones del modelo EGARCH estimado. | Download Scientific Diagram

Maximum likelihood estimation of EGARCH model (with mean and time trend ...

Parameter estimates of EGARCH and TGARCH models for three equity ...

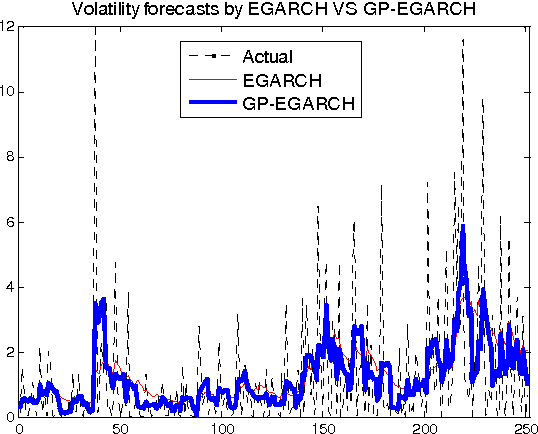

The volatility forecasting using EGARCH with different innovation ...

Egarch Model: The Indian Institute of Planning & Management, AHMEDABAD ...

Modelo EGARCH en Econometría | PDF

Egarch Model | PDF | Null Hypothesis | Normal Distribution

PPT - GARCH Models and Asymmetric GARCH models PowerPoint Presentation ...

(EViews10): How to Estimate Exponential GARCH Models #garchm #tgarch # ...

PPT - Democratic Politics and Financial Markets PowerPoint Presentation ...

PPT - Chapter 8 PowerPoint Presentation, free download - ID:3966639

GitHub - zaniara3/DCC-EGARCH-Simulation: DCC-EGARCH with ARCH in Mean ...

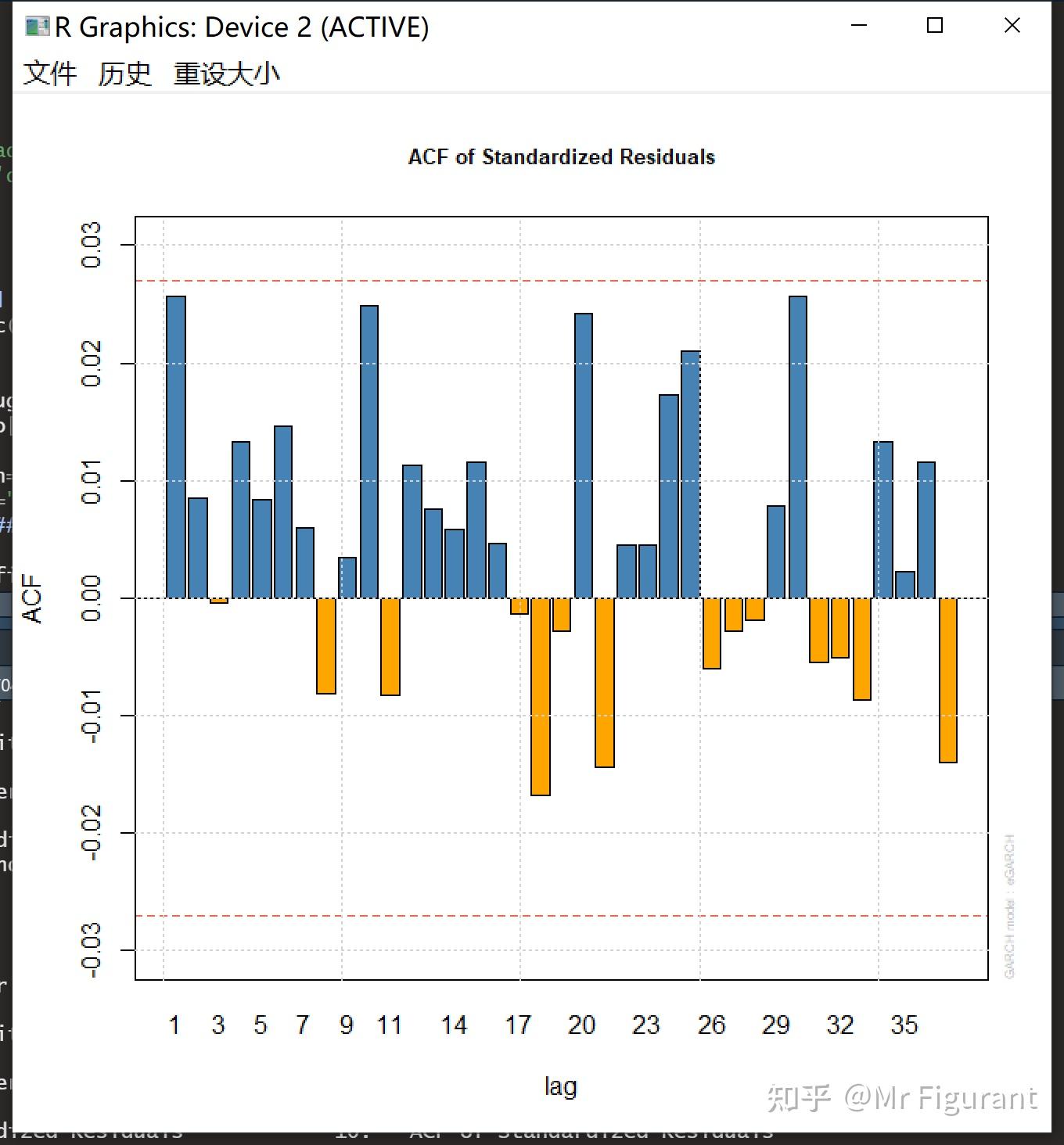

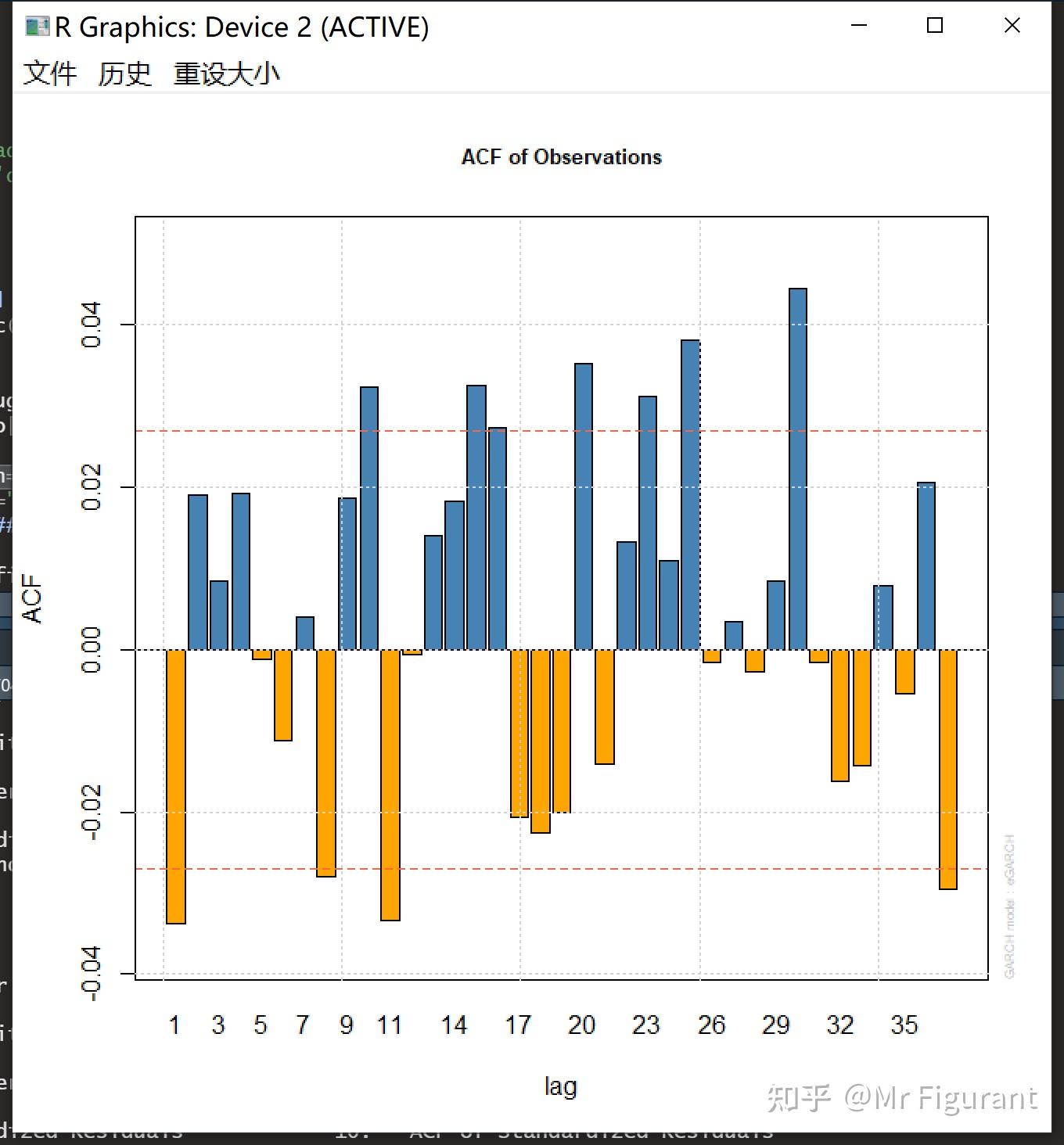

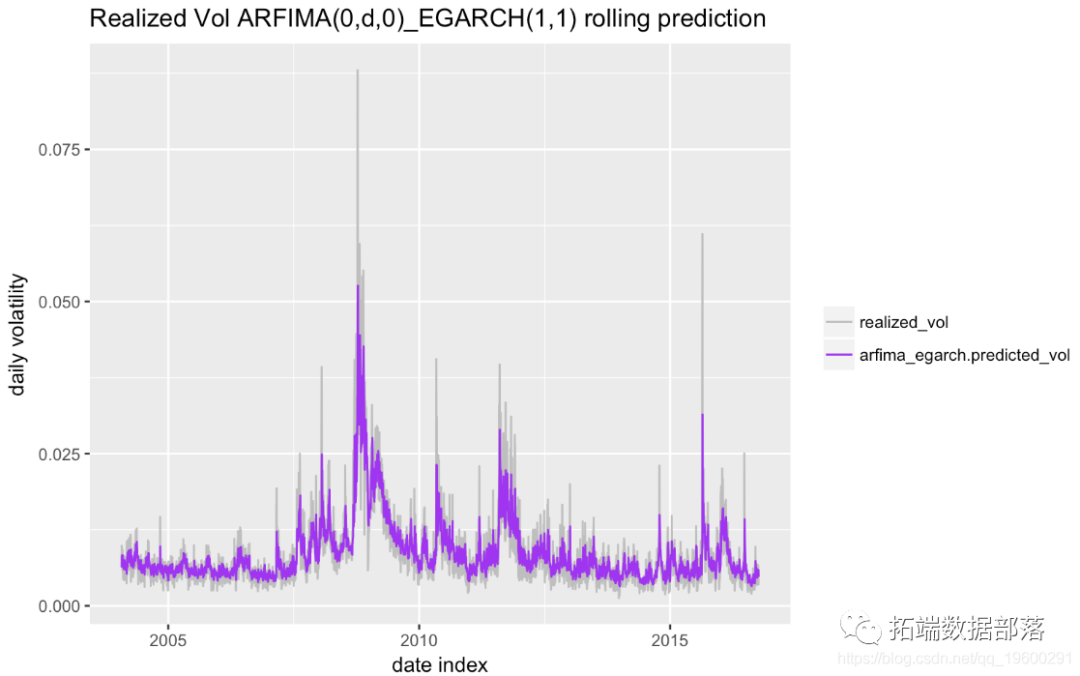

R语言ARMA-EGARCH模型、集成预测算法对SPX实际波动率进行预测_egarch模型r语言_拓端研究室TRL的博客-CSDN博客

ARCH and GARCH. Modeling Volatility Dynamics - online presentation

PPT - Lecture 8: Conditional Heteroscdastic Models PowerPoint ...

R语言学习:如何运行ARMA-EGARCH模型? - 知乎

PPT - Leveraging PowerPoint Presentation, free download - ID:657831

Volatility Modeling (part 1): Journey from ARCH to NN and MCMC

GARCH、GARCH-M、IGARCH、TARCH、EGARCH、PARCH、CGARCH模型-操作视频地址大全财经节析-张华节-计量经济学 ...

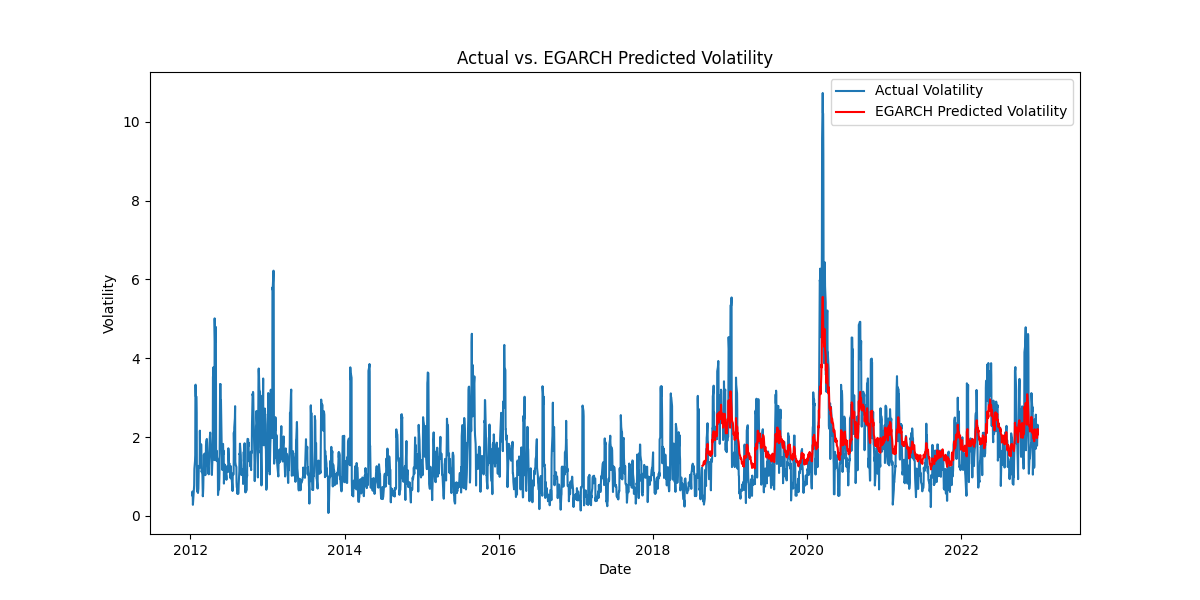

Comparison of realized volatility and conditional volatility (EGARCH ...

How to interpret negative ARCH coeff. and positive leverage effect ...

How to interpret the resulting coefficients in the conditional variance ...

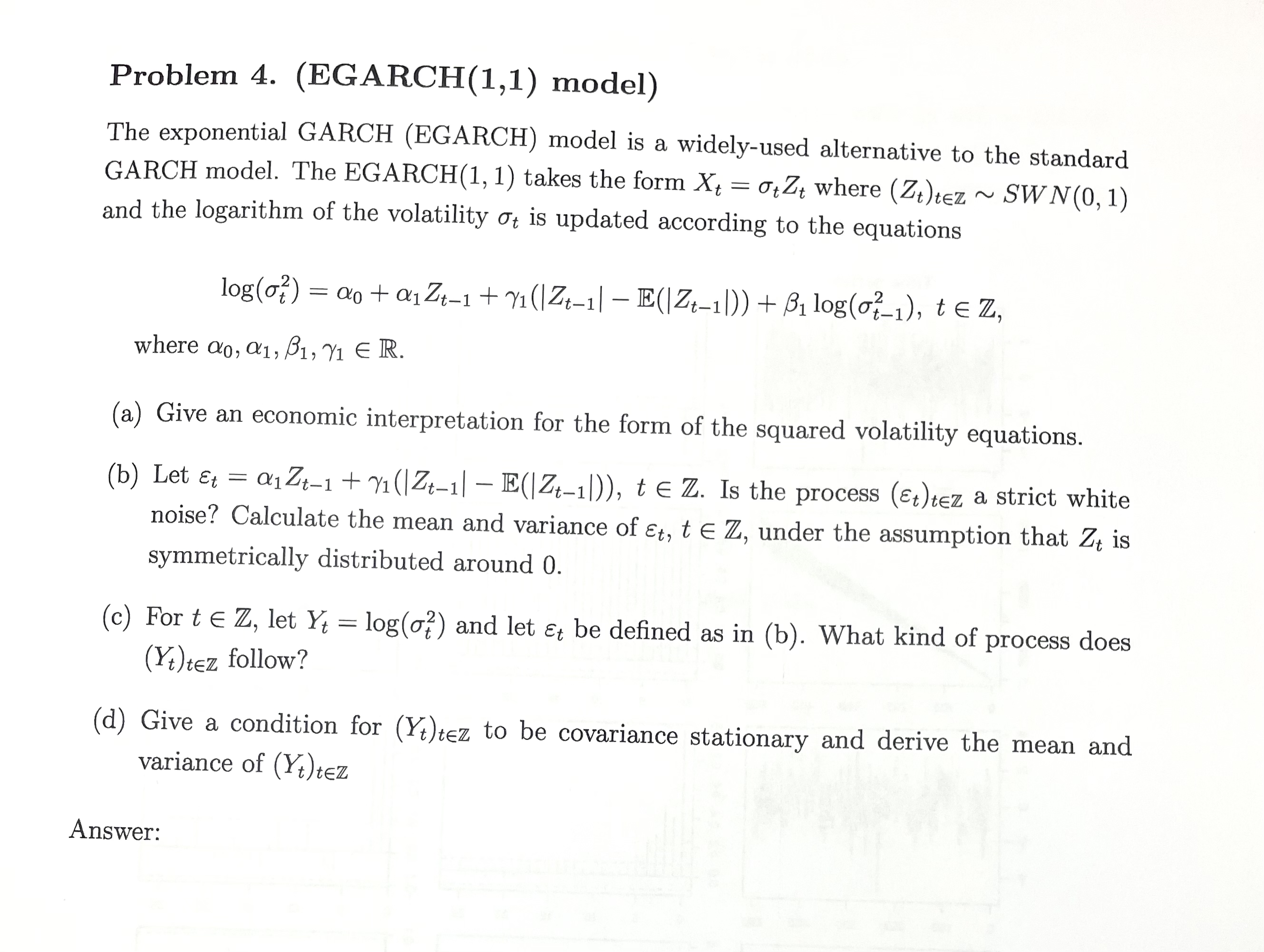

Solved Problem 4. (EGARCH(1,1) model)The exponential GARCH | Chegg.com

Conditional variance from EGARCH(1,1) Model. | Download Scientific Diagram

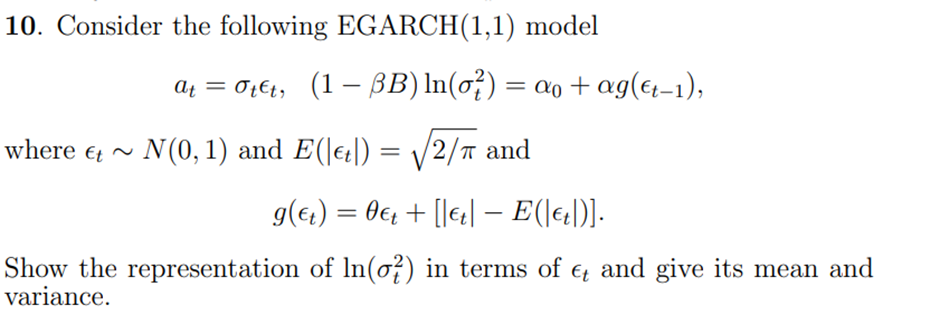

Solved 10. Consider the following EGARCH(1,1) model a_t = | Chegg.com

EGARCH: estimated coefficients of the conditional volatility equation ...

EGARCH(1,1) Model with dummy variables | Download Table

EGARCH(1,1) Model Evaluation depending on Information Criteria and ...

Parameters Estimation EGARCH(1,1) | Download Scientific Diagram

EGARCH, the fitted and forecasted variance, estimated through 2005 for ...

EGARCH(1,1) Variance Estimates | Download Scientific Diagram

8: Adjusted returns by EGARCH(1,1). | Download Scientific Diagram

ARMA-EGARCH模型、集成预测算法对SPX实际波动率进行预测|附代码数据 - 知乎

Figure 1 from Modeling and Forecasting Stock Market Volatility by ...

Summarized results of OLS, GARCH(1,1) and EGARCH(1,1) models | Download ...

Time series of EGARCH(1,1) filtered volatility of the normalized L 2 ...

EGARCH-X (Macro) Result with and without Robust Standard Errors ...

EGARCH(1,1) Model without dummy variables | Download Table

eGARCH(1,1) with normal innovation | Download Scientific Diagram

flattened and filtered probabilities of MS-EGARCH(1,1) model along with ...

Annualized volatility (in % points). (a) Annualized volatility for ...

Estimation Statistics-Distribution Comparison AR(1)-EGARCH Model ...

GitHub - Kapul/EGARCH: E-GARCH estimation of volatilities for Value ...

Relationship between epochs and loss in the hybrid model of GARCH ...

PPT - VOLATILITY MODELS PowerPoint Presentation, free download - ID:6789600

IV-EGARCH(1,1) estimations | Download Table

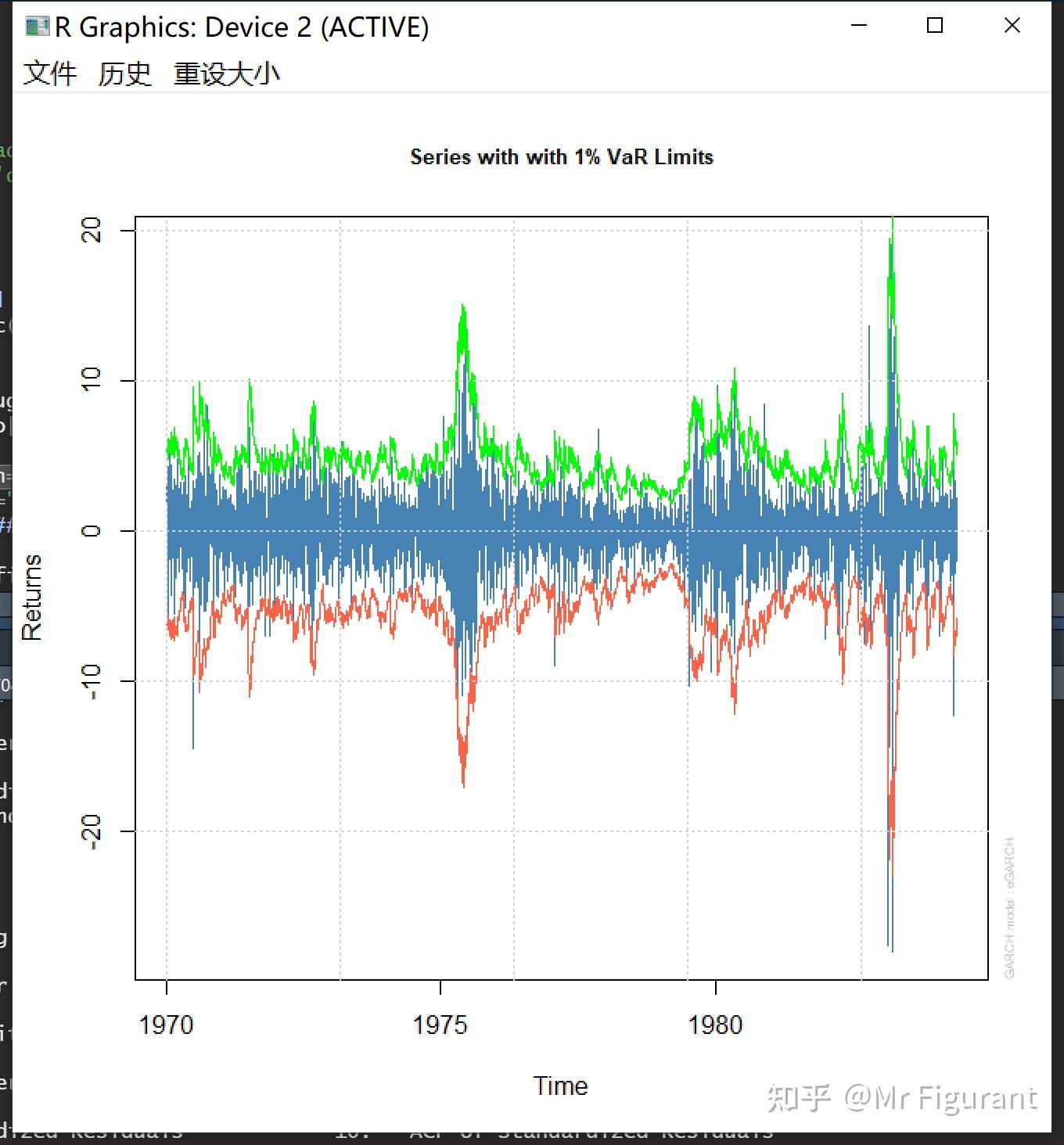

VaR plots for EGARCH. | Download Scientific Diagram

CCC-VAR-EGARCH Model with Spillover and Asymmetry | Download Table

PPT - 國際天然氣市場的訊息傳遞與價格互動 PowerPoint Presentation - ID:5064728

EGARCH-X (Speculation + Macro) Result with and without Robust Standard ...

Variation of dynamic correlation coefficient of DCC-EGARCH model ...

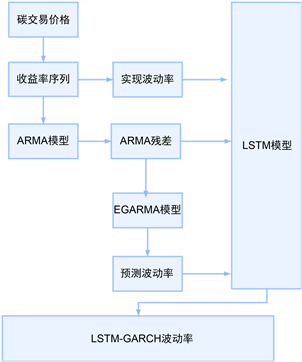

基于LSTM-EGARCH组合模型的VaR碳交易风险度量研究

ARFIMA (1,0,1) +EGARCH (1,1) estimates for equities. | Download ...

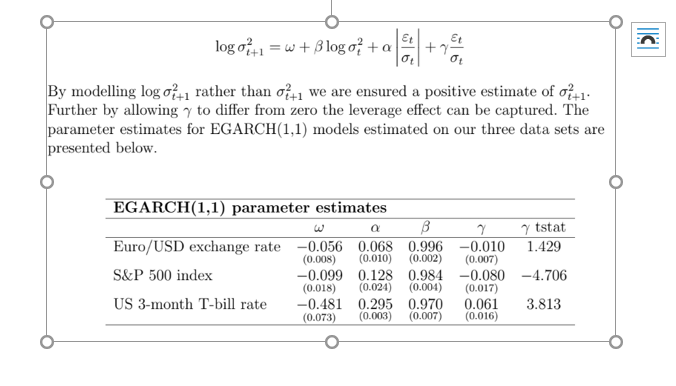

Sample | Volatility Modelling and Forecasting Using GARCH

EGARCH(1,1)model estimation results | Download Scientific Diagram

Estimated conditional volatility by index type and market | Download ...

EGARCH模型结果参数求解 - Stata专版 - 经管之家

Maximum likelihood estimations using asymmetric EGARCH(1,1) model ...

Can anyone help me interpreting the following result of Garch and ...

改进的GARCH模型——EGARCH、GJRGARCH和APARCH模型对杠杆效应的捕捉 - 知乎

深度学习 - R语言GARCH族模型:正态分布、t、GED分布EGARCH、TGARCH的VaR分析股票指数|附代码数据 - 拓端数据 ...